Gold: The Eternal Metal — 6,000 Years, One Truth | The Capital Dispatch

Gold: 6,000 Years,

One Unstoppable

Truth.

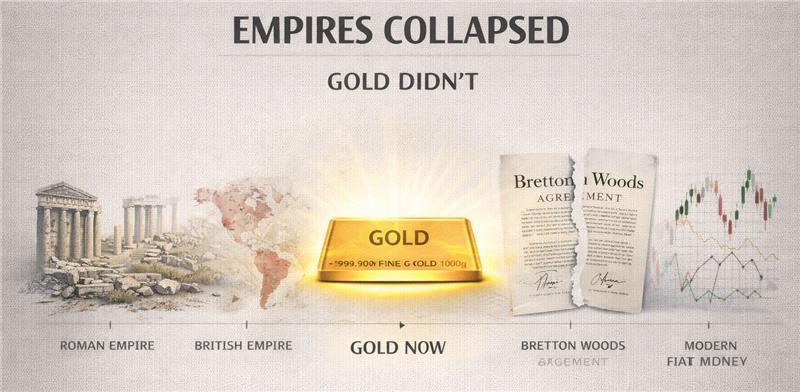

Empires rose and collapsed. Currencies were born and died. Wars rewrote the maps of nations. Through every single convulsion of human history, one substance held its value, inspired dynasties, and backed the world’s most powerful financial systems. From ancient Egyptian mines to $5,589 per ounce in 2026 — the complete story of gold: the one asset no government could ever fully control.

Jan 28, 2026

Mar 2026

Return

Bretton Woods End

Bretton Woods

Oldest Asset

There is a substance on this planet that has been coveted by every civilisation in human history. Every empire fought for it. Every religion revered it. Every government tried to control it. And every time they truly tried — they failed. Gold does not belong to any nation. It belongs to time itself.

The story of gold begins not on a trading floor or in a central bank vault, but in the dust of ancient Mesopotamia around 4,000 BCE. Long before writing was invented, before laws were codified, before empires had names — humans were already using gold. They could not explain why it was valuable. They simply knew that it was. Shimmering, permanent, unchanged by fire or time, heavy with a density that felt like truth in the palm of a hand.

What makes gold remarkable is not just its beauty — it is its chemistry. Gold does not rust. It does not corrode. It does not oxidise. You can bury it for three thousand years and dig it up unchanged. Every other material humans have used as a store of value — grain, cloth, base metals, paper — decays, decomposes, or devalues. Gold simply does not. That single physical property is the foundation of an entire 6,000-year financial history.

Gold (Au, atomic number 79) has unique properties no other element fully replicates: it does not react with oxygen (no rust), does not corrode in water or air, melts at 1,064°C, is infinitely malleable (a gram can be stretched into a wire 2km long), and every atom of gold on Earth was forged in ancient supernovae — making it cosmically rare. These properties were discovered not by economists, but over millennia by humans who noticed that gold simply never changed. That observation became the foundation of money.

Chapter 01 — The Ancient World When Gold Was the Language of Power

By 2600 BCE, Egyptian hieroglyphs were describing gold as “more plentiful than dirt” — not because it actually was, but because Pharaohs had so much of it that it defined their civilisation’s identity. The earliest known map in human history shows the plan of a gold mine. Think about what that says: before we mapped rivers, roads, or cities, we mapped the places where gold could be found.

The funeral mask of Tutankhamun — crafted in 1223 BCE and weighing over 20 pounds of solid gold — captures the core equation that governed every ancient civilisation: gold did not merely represent wealth. Gold was divinity. Egypt’s power over the ancient world was not merely military. It was metallurgical. The discovery of vast gold mines in Nubia gave Egypt a monopoly on value that lasted centuries.

The pivot from ornament to money happened in Lydia (modern-day Turkey) around 600 BCE, when King Alyattes minted the world’s first standardised gold coins from electrum — a natural gold-silver alloy. These were called Croesids after King Croesus, and they changed everything. For the first time, gold had a unit. A portable, verifiable quantity that two strangers could exchange with confidence. The concept of currency was born — and it was made of gold.

The Persians, Greeks, and Romans each adopted and expanded the system. Julius Caesar introduced the gold aureus — 8 grams, pure, bearing the Emperor’s face — around 49 BCE. It underpinned the economic stability of the greatest empire the world had seen. And when Rome began debasing its gold coins — gradually reducing their purity to fund military expansion — it was not merely a monetary crisis. It was a civilisational one. The Roman Empire’s slow disintegration was partly a story of gold: when you debase your currency, you debase your authority.

Chapter 02 — The Gold Standard Era The World Ran on Gold for 200 Years

Britain accidentally adopted a de facto gold standard in 1717 when Isaac Newton — then Master of the Royal Mint — set the exchange rate of silver to gold too low, driving silver coins out of circulation. Newton, the man who discovered gravity, inadvertently changed the global monetary order. By the 1870s, most major nations had formalised what Newton accidentally initiated: a system where every unit of currency was backed by a fixed weight of gold.

The gold standard era — roughly 1870 to 1914 — was a period of extraordinary global economic stability. Inflation was negligible. Trade balances resolved automatically. A pound sterling meant a fixed quantity of gold, and that meant it meant something. When the First World War hit in 1914, every major nation immediately abandoned it. You cannot wage industrial-scale war on a gold budget.

Under a classic gold standard, each unit of currency represented a fixed weight of gold held in reserve. If a country ran a trade deficit, gold flowed out, the money supply contracted, prices fell, exports became cheaper, and the deficit corrected automatically. The system was self-regulating and anti-inflationary — but brutally inflexible. It prevented governments from responding to recessions by expanding credit. When the Great Depression arrived, Roosevelt confiscated US gold at $20.67/oz and repriced it at $35 the following year — an immediate 69% devaluation, executed overnight.

BCE

Chapter 03 — Bretton Woods & The Nixon Shock The Day America Unchained Gold — And Changed Everything

The 1944 Bretton Woods Conference was the most consequential meeting in the history of global finance. Forty-four nations gathered in New Hampshire to build the post-war monetary order from scratch. The agreement was elegant: the US dollar would be the world’s reserve currency, fixed to gold at $35 per ounce. The United States, holding approximately three-quarters of all the world’s official gold reserves, was the anchor of the entire global financial system.

For the first fifteen years, it worked magnificently. But in the 1960s, the cracks appeared. The Vietnam War cost billions. The Great Society domestic programmes cost more. America was spending dollars faster than it was producing goods — and European governments, led by France’s Charles de Gaulle, began noticing.

French President Charles de Gaulle was the first leader to publicly challenge the dollar’s privileged role. He called Bretton Woods “America’s exorbitant privilege” and dispatched a French ship to New York in 1965 to collect $300 million in physical gold from Fort Knox. Between 1958 and 1971, US gold reserves fell from 574 million ounces to approximately 276 million ounces. The arithmetic was simple: America was printing dollars faster than the world trusted they were worth $35 per ounce of gold.

On August 15, 1971, Nixon announced the decision to a stunned world: the United States would immediately end the convertibility of dollars to gold. No more redeeming dollars for gold. No more $35 peg. The world’s currencies — overnight — had no commodity anchor whatsoever.

◆ Sources: Royal Mint, CBS News, Investing News Network, J.P. Morgan Research. Bars proportional to price.

Chapter 04 — Why Gold Is Called “Safe Haven” The Six Reasons Gold Wins When Everything Else Loses

Chapter 05 — The Backbone of Currencies Why Every Currency System Eventually Returns to Gold

Even today, in a world of pure fiat currency, gold’s shadow falls across every major monetary institution. The United States holds approximately 8,133 tonnes of gold reserves — the world’s largest national gold stockpile. Every major economic power maintains substantial gold reserves — not for sentimental reasons, but because every government treasury in the world understands that gold is the ultimate backstop of last resort.

Author and economist Jim Rickards has argued that a de facto “shadow gold standard” already exists — not formally declared, but functionally present. When you examine the world’s major central bank balance sheets and the ratio of gold to money supply, the implied gold price needed to restore a full gold standard would be between $10,000 and $50,000 per ounce. That range is not a prediction — it is a measure of how much fiat money has been created since 1971 without a corresponding increase in gold reserves. The gap between printed money and physical gold is the measure of the world’s accumulated monetary risk.

The 2022 episode of Russia’s $300 billion in foreign exchange reserves being frozen by Western sanctions was a watershed moment. For the first time in modern history, a major geopolitical power watched its entire foreign currency reserve vanish overnight by decree. The one asset that could not have been frozen, seized, or sanctioned? Physical gold held on Russian soil. Within months, central bank gold buying globally accelerated sharply.

Chapter 06 — Why Gold Moves Markets Gold as the Barometer of Global Fear

Gold’s price is not really about gold. It is about confidence — specifically, confidence in the entire system of fiat money, government institutions, and global stability. When that confidence is high, gold is less needed. When that confidence cracks — even fractionally — gold reacts with extraordinary sensitivity, often moving before any other asset class.

| Gold’s Price Signal | What It Measures | Implication |

|---|---|---|

| Gold Rising vs Dollar | Dollar Losing Credibility | Markets losing faith in US fiscal position, Fed independence, or reserve currency status |

| Gold Rising with Dollar | Pure Fear / Crisis Flight | Extreme stress — both safe havens bid simultaneously (rare but signals extreme dislocations) |

| Gold Rising vs All Currencies | Global Monetary Debasement | Universal loss of confidence in fiat money — central banks printing simultaneously |

| Gold Rising During War | Geopolitical Tail Risk | Markets pricing physical destruction of assets, supply disruptions, and breakdown of global order |

| Gold Falling on Strong NFP | Strong Economy Signal | Good data → higher rates → stronger dollar → gold less attractive as non-yielding alternative |

| Gold Rising Despite Rate Hikes | Structural Bull Market | Gold ignoring traditional headwinds = structural buyers overriding tactical signals |

Gold in War:

When the World Burns,

Gold Shines.

War is the ultimate test of every asset. Supply chains break. Borders close. Currencies collapse. Governments seize private property. In every war in recorded history, the pattern has been identical: assets that depend on functioning institutions become uncertain. Gold, which depends on nothing and no one, becomes the universal refuge.

The modern financial mechanism is elegant in its simplicity: when war threatens economic stability, investors move out of equities into safe havens. The first safe haven is US Treasuries. The second — and increasingly the first — is gold. The difference: Treasuries require you to trust the US government to pay. Gold requires you to trust nothing but physics.

Chapter 07 — The 2025–2026 Bull Run Why Gold Set 53 Records in One Year

It was not one thing. It was never one thing. The most extraordinary gold bull run in modern history was the product of six forces converging simultaneously — a once-in-a-generation alignment of every variable that has ever driven gold higher.

Force 1: The Tariff Wars and Dollar Erosion

The Trump administration’s blanket tariff agenda — 25% on steel and aluminium, sweeping tariffs on Canada, Mexico, and China — created the kind of policy uncertainty that gold thrives on. Trade uncertainty suppressed global growth expectations, weakened confidence in US assets, and drove the DXY dollar index down over 10% in the first half of 2025. A weaker dollar is almost always mechanically bullish for gold.

Force 2: The Federal Reserve Investigation

On January 9, 2026, the US Department of Justice opened a criminal investigation into Federal Reserve Chairman Jerome Powell. The symbolic impact was immediate: the independence of the world’s most powerful central bank was suddenly in question. Gold, which has no central bank and answers to no government, was the natural beneficiary.

Force 3: Record Central Bank Buying — 3 Consecutive Years

For three consecutive years — 2022, 2023, and 2024 — central banks globally purchased over 1,000 tonnes of gold per year. China’s People’s Bank extended its buying for 15 consecutive months into January 2026. J.P. Morgan projects 755 tonnes of central bank purchases in 2026 alone — still elevated versus the pre-2022 average of 400-500 tonnes per year.

Force 4: ETF Inflows Return

After two years of ETF outflows (2022-2023, as rising rates made gold less competitive), the gold ETF market swung to significant inflows in 2024 and accelerated dramatically in 2025. J.P. Morgan projects 250 tonnes of ETF inflows in 2026 alone. The return of institutional ETF demand alongside continued central bank buying created a two-sided structural bid that absorbed every tactical selloff.

In Q3 2025, 950 tonnes of combined investor and central bank demand translated to approximately $109 billion of quarterly gold purchases — roughly 90% higher than the preceding four-quarter average. J.P. Morgan’s framework holds that 350+ tonnes of quarterly net demand implies positive price pressure. At 950 tonnes, the price was going only one direction: up. That demand level persisted, with J.P. Morgan projecting 585 tonnes/quarter averaged through 2026.

Force 5: De-Dollarisation — The Structural Shift

The share of global foreign exchange reserves held in US dollars fell from 71% in 1999 to approximately 56.3% by end-2025. BRICS nations accelerated settlement systems denominated outside the dollar. Saudi Arabia began accepting yuan for oil. Every dollar that exits the global reserve system needs to go somewhere. An increasing proportion of that somewhere is gold — and this is a structural decoupling building for 25 years, not reversible by any single event.

Force 6: The Iran War and the $5,000 Threshold

Gold’s push past $5,000 for the first time in history — on the way to its January 28th all-time record of $5,589.38 — coincided with escalating US-Iran tensions that culminated in Operation Epic Fury on February 28th. When the petrodollar system itself is under physical threat via the Strait of Hormuz, gold’s role as the alternative reserve asset becomes acute.

Chapter 08 — Why Gold Gets Pricier Every Decade The Structural Reasons the Floor Keeps Rising

Gold’s long-term price trajectory is not random. It is the intersection of structural forces that only move in one direction over multi-decade timeframes. Understanding them is the key to understanding why gold at $5,000 is not the same kind of “expensive” that $1,900 was in 2011.

| Structural Driver | Direction | Long-Term Implication |

|---|---|---|

| Global Debt Accumulation | ▲ Always rising | Total global debt exceeds $300 trillion. More debt = more potential for monetary debasement = higher structural gold floor. US debt alone crossed $36T in 2026. |

| Mine Supply Constraints | → Flat to declining | Gold mine production grows ~1.5%/year. Major new gold discoveries are increasingly rare. Supply cannot chase demand. |

| Central Bank Diversification | ▲ Multi-year trend | Post-Russia sanctions, every EM central bank is diversifying toward gold. This is a decade-long structural shift. |

| Fiat Currency Proliferation | ▲ Irreversible | Since 1971, global money supply has expanded exponentially. Every dollar, euro, yuan, and pound created without a gold anchor is another unit of fiat chasing the same fixed quantity of gold. |

| Generational Wealth Transfer | ▲ Accelerating | An estimated $84 trillion in assets will transfer from Baby Boomers to Millennials and Gen Z through 2045. Even 1-2% allocation toward gold = trillions in new demand. |

| Geopolitical Fragmentation | ▲ Rising | Multipolar world = more conflicts, more sanctions weaponisation, more trade fragmentation = more demand for an asset no government controls. This trend accelerated sharply in 2022–2026. |

January 28, 2026

Return

In 2025 Alone

Central Banks/Year

Key Gold Driver

2027 Target

Where Does Gold Go From Here?

Mountains or Rollercoaster?

Gold just set an all-time high of $5,589 per ounce on January 28, 2026 — and is currently trading near $5,050, nearly 10% below that peak. Is this a breather before the next assault on $6,000? Or is 2026 the year gold’s rollercoaster finally tips downward?

- J.P. Morgan has a $5,000 base case for Q4 2026 and cites $6,000 as a realistic longer-term possibility with continued 585 tonnes/quarter of demand

- The Iran war is not resolved. Every week of continued Hormuz disruption is a week of rising inflation pressure that eventually forces the Fed back toward easing — structurally bullish gold

- The dollar is 10.7% weaker YTD — its worst first half in 50 years. A dollar in structural decline is gold’s most reliable tailwind

- The shadow gold standard argument: the implied “true” gold price of $10,000–$50,000 per ounce at historical monetary ratios. The gap has never been wider

- The $84 trillion wealth transfer — as Boomers pass assets to younger generations more comfortable with gold ETFs, structural allocation demand will grow for decades

- If the Iran war resolves rapidly with a ceasefire, the geopolitical premium — estimated at $300–$500/oz — could unwind violently within days

- If February NFP surprises to the upside and the Fed holds rates higher for longer, real yields rise, the dollar strengthens, and gold loses its anti-dollar premium

- Profit-taking at all-time high levels. The March 3rd intraday crash of –5.16% to $5,050 showed the speed at which crowded longs can unwind

- A Bitcoin or crypto narrative takeover — if digital assets increasingly absorb the inflation-hedge allocation, demand may structurally soften among younger investors

- Recall 1980: gold surged from $35 to $850 in nine years — then crashed to $265 over the next 20 years. Post-peak corrections in gold are not short. They are brutal and decade-long.

“Gold at $5,000 is not the same story as gold at $1,900 in 2011. In 2011, the bull market was driven by fear and speculation. In 2026, it is being driven by central banks — the very institutions that were gold’s traditional opponents. When the money-makers become the gold-buyers, the game has fundamentally changed.”

But here is the question nobody can answer: at what price does gold’s truth stop being a hedge and start being a warning? If gold reaches $8,000, $10,000 — what is it telling us? Is it the safe haven winning, or the system losing? Gold at truly transformative prices is not a success story for investors. It is a story of a world that has lost faith in the institutions that hold it together.

The mountains may still be ahead. The rollercoaster is always one geopolitical surprise away. Gold does not tell you which. Gold only tells you: it is not over. It is never over.

Frequently Asked Questions

■ Gold — Everything You’ve Wondered, Answered

Conclusion: The Metal That Outlived Every Empire — and Every Crisis

Six thousand years. Every civilisation. Every monetary system. Every war. Every financial crisis. Every attempt by governments to print their way to prosperity. And through all of it, one thread runs unbroken: gold held its value. Not every day, not every year — but across every generation that has ever lived, the metal that ancient Egyptians dug from Nubian mines and the metal that JPMorgan analysts are pricing at $5,000+ per ounce in 2026 is the same substance, performing the same function it always has.

The 2025–2026 bull run is not a speculative mania. It is the culmination of structural forces building for decades: a dollar losing reserve share, governments running deficits that can only be financed by monetary expansion, geopolitical fragmentation that makes foreign reserves vulnerable to seizure, and central banks that understand — better than any retail investor — that gold is the backstop when everything else fails.

Gold at $5,589 per ounce on January 28, 2026 is not a number that existed anywhere in human consciousness five years ago. And yet here we are. The question no analyst can honestly answer is whether $5,589 is gold’s mountaintop for this generation, or its base camp for the next ascent.

History offers one clue. Every time in recorded history that governments expanded their money supply beyond what the economy justified, gold eventually caught up. Not immediately. Not smoothly. But inevitably. The shadow gold standard implied price of $10,000–$50,000 per ounce remains a mathematical possibility the market is slowly, year by year, rediscovering.

Gold does not rise because people become irrational. Gold rises because money becomes unreliable. And the answer to where gold goes next is simply: wherever money goes wrong first.

Published March 6, 2026 by The Capital Dispatch at Capital Street FX (capitalstreetfx.com). For informational and educational purposes only. Not financial advice. Sources: World Gold Council, J.P. Morgan Global Research, CBS News, Investing News Network, Royal Mint, Federal Reserve History, USA Gold, Wikipedia (Nixon Shock, Gold Standard, Bretton Woods), Hard Money History, SimTrade.