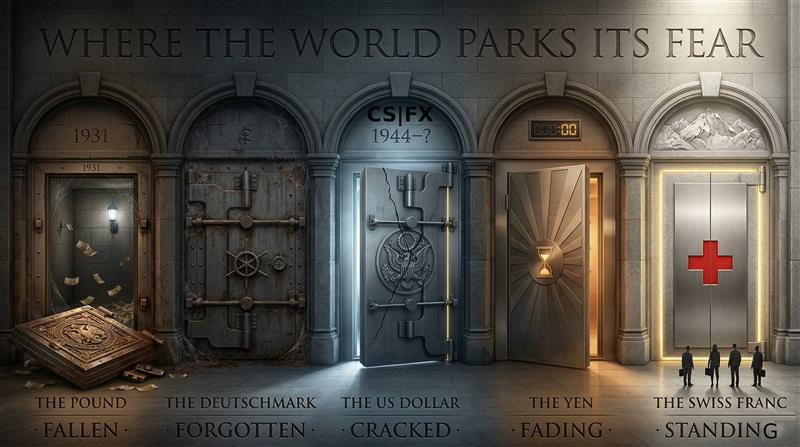

Safe Haven Currencies: The Complete History | The Capital Dispatch

Safe Haven Currencies:

The Complete History

of Where the World

Hides Its Fear

From the pound sterling’s Victorian dominance to Bretton Woods to the yen carry trade to Francogeddon. From the dollar’s post-war supremacy to Liberation Day 2025, when it fell instead of rising. The complete, unflinching story of which currencies the world has trusted with its fear — how they earned that trust, when they lost it, and which ones are about to inherit it.

Mar 2026 · +13% vs USD in 2025

Unwind · 149.30

Worst Since 1973

Global FX Reserves

–1944 · Now At Risk

Reserve Currency

A safe haven currency is not a currency that is safe. It is a currency that people believe will be safe — a distinction that sounds philosophical but has moved trillions of dollars across borders in a matter of hours. The history of safe haven currencies is the history of trust: how it is built over generations, how it is destroyed in moments, and why the world perpetually needs somewhere to park its fear.

When panic strikes global markets — when banks fail, wars break out, inflation erupts, or a government collapses under the weight of its own debt — money moves. Not gradually. Not in an orderly fashion. It moves in torrents, in hours, in a single direction: toward the perceived sanctuary of a currency that will hold its value while everything else does not. The currencies that earn this designation do not announce themselves. They are selected by millions of simultaneous decisions made by central banks, sovereign wealth funds, institutional investors, and terrified individuals across every time zone, all reaching the same conclusion at the same moment: this is the safest place to be.

Since the dawn of modern finance, only a handful of currencies have ever earned that designation. The British pound sterling held it for the better part of two centuries. The US dollar has held it since 1944. The Swiss franc has held it since the First World War. The Japanese yen has held a complicated version of it since the 1990s. And in 2025 and 2026, for the first time in eighty years, the question of who holds it next has become genuinely open.

A safe haven currency is one that appreciates, or at minimum holds its value, during periods of global financial stress, geopolitical crisis, or economic uncertainty, while riskier currencies fall. The academic consensus identifies five necessary conditions: a large, deep, and liquid financial market that can absorb massive capital flows without dislocating; political stability and institutional reliability; a history of low inflation demonstrating the central bank’s commitment to purchasing power preservation; a current account surplus or strong net international investment position providing structural demand for the currency; and a carry trade dynamic whereby the currency is borrowed cheaply in normal times and repurchased during stress, mechanically driving it higher. No currency in history has satisfied all five conditions perfectly. The question has always been: which currency fails the fewest tests?

Chapter 01 — The Age of Sterling When the British Pound Was the World’s Reserve

The British pound sterling’s dominance as the world’s reserve and safe haven currency was not designed. It was earned, incrementally, through the combination of the world’s most powerful navy, the world’s largest empire, the world’s most sophisticated capital markets, and a monetary system — the gold standard — that gave pound-denominated assets a credibility no other currency could match. By the mid-nineteenth century, London was the undisputed centre of global finance. British merchant banks financed trade from Argentina to India. The pound sterling was the settlement currency for the majority of world commerce. Countries held sterling as their reserve asset not because anyone told them to, but because it was the only currency liquid and reliable enough to trust at scale.

The classical gold standard, formalised in the 1870s when most major nations pegged their currencies to gold, cemented sterling’s position. Because Britain had the world’s most developed gold market, the deepest capital markets, and the largest merchant fleet, the pound effectively became the world’s de facto currency — the original global safe haven. Nations under financial stress did not flee to abstract safety. They fled to London. They bought gilts. They held sterling. Until World War I, the pound accounted for over 60% of the world’s debt holdings, and it traded at just under five dollars.

The First World War ended that era irrevocably, though the ending took decades to complete. Britain borrowed massively to finance the war, ran persistent trade deficits, and lost its net creditor status to the United States. The 1925 decision by Winston Churchill — then Chancellor of the Exchequer — to return sterling to the gold standard at its pre-war parity was, in his own later assessment, the biggest mistake of his career. With the pound overvalued by approximately 10% against the dollar, British exports were strangled, unemployment rose, and the currency became an easy target for speculators. In 1931, a speculative attack depleted the Bank of England’s gold reserves so rapidly that Britain was forced to abandon the gold standard entirely. The pound’s reign as the world’s safe haven was over, though its formal demotion would not be formalised until 1944 at Bretton Woods. It had taken 30 years to complete what the guns of 1914 had begun.

Chapter 02 — Bretton Woods and the Dollar’s Coronation How $35 Per Ounce Built the Modern Monetary World

In July 1944, as the Allied armies were fighting across Normandy, 730 delegates from 44 nations gathered at the Mount Washington Hotel in Bretton Woods, New Hampshire, to design the post-war monetary order. The outcome was determined, in practice, by a single fact: the United States held approximately $26 billion in gold reserves — roughly 65% of the world’s total official gold stock. Every other major power was either bankrupt or deeply indebted to Washington. The British economist John Maynard Keynes argued eloquently for an international reserve currency — which he called the “bancor” — that would belong to no single nation. The American Harry Dexter White won. The dollar would be the anchor. Every other currency would be pegged to the dollar. The dollar alone would be convertible to gold at $35 per ounce.

The Bretton Woods system was the most deliberate safe haven designation in monetary history. It did not emerge from market competition or trust accumulated over generations. It was decreed. And for twenty-seven years, it worked. The post-war reconstruction of Europe and Japan powered the longest sustained economic expansion in modern history. The dollar’s gold convertibility gave it a credibility that no fiat currency has since matched. US Treasury bonds became the global risk-free asset — the instrument that every investor in the world would buy when fear overwhelmed greed.

Bretton Woods answered the question “where should money go when the world is frightened?” with a single answer: Washington. For twenty-seven years, that answer was correct.

The system began cracking almost from inception. The fundamental paradox — later called the Triffin Dilemma — was that for the world to have enough dollars to finance international trade, the US had to run persistent balance of payments deficits. But those deficits steadily eroded confidence in the dollar’s gold backing. By 1968, US gold reserves had fallen to $10.7 billion — barely a third of the 1944 level — while foreign dollar claims had ballooned. France, led by Charles de Gaulle, began systematically converting its dollar reserves to gold. Germany and the Netherlands allowed their currencies to float free of the system. On August 15, 1971, President Nixon appeared on American television and, in a decision made over a secret weekend meeting at Camp David, announced the end of dollar-gold convertibility. Bretton Woods was over. The dollar was now a fiat currency — its value backed by nothing except the continued confidence of the world in American institutions.

Nixon’s announcement that the dollar would no longer be convertible to gold at $35 per ounce was the most consequential monetary event since Bretton Woods itself. It did not destroy the dollar’s safe haven status — that would survive for another five decades — but it fundamentally changed the basis for that status. From 1971, the dollar’s value rested not on gold but on the world’s collective confidence in American institutions: the rule of law, the independence of the Federal Reserve, the depth and liquidity of US financial markets, and the military and geopolitical reach of American power. Every one of those foundations is now, in 2026, under meaningful strain for the first time since 1971.

Chapter 03 — The Swiss Franc’s Long Ascent Neutrality as Monetary Policy: 200 Years of Refuge

Switzerland has not been involved in a military conflict since 1815. That is not merely a historical curiosity. It is the foundation of the Swiss franc’s monetary identity. While every other major European currency was subjected to the inflationary pressures of wartime finance — money printing to fund armies, debts that degraded purchasing power, gold reserves depleted by military necessity — the Swiss franc remained stable. In 1914, one US dollar cost 5.13 Swiss francs. By March 2026, one Swiss franc costs more than one US dollar. In the 112 years since the First World War began, the franc has appreciated by more than 500% against the dollar in real terms. No other currency in the world has a comparable long-run record of purchasing power preservation.

The franc’s safe haven credentials were established, paradoxically, by the crisis it was not part of. During the 1920s, European currencies collapsed one after another. Germany’s Weimar hyperinflation saw a loaf of bread rise from one mark to 750 billion marks in a single decade. Austria, Hungary, and Poland experienced similar monetary catastrophes. Switzerland, with its political neutrality, fiscal conservatism, and low public debt, maintained its gold standard and kept the franc stable while its neighbours’ currencies were destroyed. Foreign capital poured in. The Swiss banking system — already renowned for discretion — became the preferred depository for European wealth seeking protection from monetary chaos. The 1920s forged an institutional memory in global finance: when currencies fail, park the money in Switzerland.

The modern Swiss franc’s safe haven mechanics are well-understood. Switzerland runs a persistent current account surplus — the economy generates more foreign exchange from exports, tourism, and financial services than it consumes. The Swiss National Bank maintains one of the world’s most conservative monetary policy frameworks, targeting inflation below 2% — a target it has generally met over the past century. Swiss public debt has been kept below 30% of GDP even during the most severe global crises, compared to over 100% in France, Italy, and the United States. And Switzerland’s financial secrecy — while substantially eroded by post-2008 international regulatory pressure — still draws capital from political and economic instability worldwide.

The most dramatic single-day event in the history of safe haven currencies occurred not during a financial crisis but during a period of relative calm. In September 2011, the Swiss National Bank had set a floor of 1.20 francs per euro to protect Swiss exporters from the franc’s relentless appreciation during the Eurozone debt crisis. For over three years, the SNB spent hundreds of billions of francs defending this floor, accumulating foreign reserves equivalent to more than 80% of Swiss GDP. Then, on January 15, 2015, without warning, the SNB abandoned the peg. Within minutes, the franc surged 25-30% against the euro. The Swiss Market Index fell over 10% in a single day. Currency brokers and funds that had been short francs were instantly bankrupt. The lesson was inscribed permanently in the institutional memory of FX traders: safe haven status is a sword as much as a shield. When enough capital piles into a safe haven, the central bank of a small country cannot indefinitely absorb the flows. Something will eventually break — and when it breaks, it breaks violently.

In 2025, the franc delivered its most significant safe haven performance since 2015. Against the US dollar, it gained nearly 13% over the year. Against the euro, it touched an 11-year high. In April 2025 alone, during the worst of the Liberation Day tariff shock, the franc surged approximately 9% against the dollar in a single month — the kind of move that in any other major currency pair would constitute a multi-year event. By March 2026, the franc is trading above parity against the dollar — a level that would have seemed impossible as recently as 2017. The SNB is reportedly watching closely, concerned that franc strength is suppressing exports and threatening deflation. History suggests it will intervene eventually. History also suggests that intervention will not hold indefinitely.

Chapter 04 — The Japanese Yen’s Paradox A Safe Haven Built on Borrowed Money and Unwound Trades

The Japanese yen’s status as a safe haven is the most counter-intuitive designation in all of global finance. Japan has the world’s largest public debt as a percentage of GDP — over 250%. It runs persistent trade deficits. Its population is shrinking and ageing. Its central bank has maintained near-zero or negative interest rates for three decades. By any conventional analysis of safe haven fundamentals, the yen should not qualify. And yet, for the better part of thirty years, it has been one of the most reliable safe haven instruments in the world. Understanding why requires understanding the carry trade — the most important mechanical force in foreign exchange markets that most people have never heard of.

The carry trade is simple in principle. An investor borrows in a currency with low interest rates — say, the Japanese yen at near zero percent — and invests the proceeds in a higher-yielding currency or asset. As long as the exchange rate stays stable or moves in the right direction, the investor pockets the interest rate differential as profit. Beginning in the mid-1990s, as the Bank of Japan cut rates to near zero to combat deflation following the collapse of Japan’s asset price bubble, the yen became the world’s preferred funding currency. Trillions of dollars of yen were borrowed by investors worldwide to buy Australian dollars, US Treasuries, emerging market bonds, and virtually any higher-yielding asset on the planet. This structural short position on the yen — the aggregate of all these borrowings — is what creates the yen’s safe haven mechanics.

When a crisis hits and risk appetite evaporates, carry trade positions are unwound simultaneously. Investors sell their higher-yielding assets and buy back yen to repay their borrowings. This mechanical repurchase of yen — regardless of Japan’s domestic economic conditions — drives the currency sharply higher during crises. The yen is not a safe haven because Japan is a safe country for investment. It is a safe haven because the world is heavily short it in normal times, and when fear arrives, the short must be covered. The 2008 financial crisis produced a yen appreciation of over 20% in effective terms within months of the Lehman collapse. The 2010-2011 Eurozone debt crisis produced similar dynamics. The Brexit shock in 2016 drove the yen to its strongest level in three years within hours of the referendum result.

Every Crisis Writes the Rules Differently

Chapter 05 — The Dollar Under Question Can the World’s Safe Haven Lose Its Status?

The dollar’s safe haven status rests on four pillars that have, until recently, been unshakeable: the depth and liquidity of US financial markets; the institutional independence and credibility of the Federal Reserve; the rule of law and predictability of US policy; and the absence of any credible alternative large enough to absorb a reallocation of global reserves. In 2025, all four pillars were subjected to the most serious stress test since Bretton Woods.

The dollar index (DXY) fell 10.8% in the first half of 2025 — its worst six-month performance since 1973, the year the Bretton Woods system formally ended. During the April Liberation Day tariff shock, the dollar fell when previous market history said it should have risen. Trump’s attacks on Federal Reserve Chairman Jerome Powell — threatening his removal, publicly demanding rate cuts, questioning the Fed’s independence — damaged one of the core pillars of dollar safe haven status: the belief that the currency is managed by an institution free from political interference. The “One Big Beautiful Bill” Act’s projection of trillions in additional US debt over the coming decade raised questions about the long-term sustainability of US government finances that investors had previously been willing to overlook.

And yet, the dollar has not fallen from its reserve throne. The dollar’s share of global FX reserves has declined from approximately 71% in 2000 to approximately 58% by 2024 — a meaningful decline, but one that has occurred over 24 years, not 24 months. In July 2025, AI sector investment flows helped stabilise the currency. By late 2025, the dollar had largely recovered from its Liberation Day lows. A Federal Reserve official, speaking at the 2026 US Monetary Policy Forum in March 2026, reminded the audience that even after the US suffered its first credit downgrade from AAA in August 2011, Treasury bond prices rallied — investors bought Treasuries as a safe haven after they were downgraded. The dollar’s structural position — the deepest, most liquid financial market in the world, the currency in which global commodities are priced, the denomination of approximately 50% of all international debt — does not dissolve in a single year of erratic policy.

Gold surpassed the euro as the second-largest reserve asset globally by value in 2025, driven by central bank buying and rising prices. Dollar share has fallen from 71% in 2000 to ~58% in 2024 — significant erosion, but structurally still dominant.

Chapter 06 — The Current Safe Havens Who the World Trusts in March 2026

The hierarchy of safe haven currencies in March 2026 is undergoing its most significant reshuffling since the Nixon Shock of 1971. The Swiss franc has emerged as the single strongest performer in the post-Liberation Day world. The Japanese yen retains its mechanical carry-trade safe haven properties, though the Bank of Japan’s tentative moves toward policy normalisation — the first interest rate rises in decades — are beginning to change the structural dynamics that created those properties. The US dollar remains the dominant reserve currency but has partially lost its pure risk-off safe haven characteristics during crises that originate in US policy. And a third tier of currencies — the euro, the Singapore dollar, and increasingly the Chinese renminbi in specific contexts — is beginning to attract serious discussion as potential safe haven candidates.

The franc’s safe haven dominance in 2025–2026 reflects a structural advantage that no policy can manufacture quickly: it has been doing this for over a hundred years. Switzerland’s neutrality, its fiscal conservatism, its current account surplus, its institutional credibility, and the SNB’s track record of maintaining purchasing power — all of these compound over decades into an irreplaceable trust. The franc gained approximately 13% against the dollar in 2025, hit an 11-year high against both the dollar and the euro, and continues to be the first destination for capital fleeing political risk in 2026. The SNB’s challenge — that a too-strong franc damages exporters and risks deflation — is real, but it is the challenge of success, not failure.

The yen’s position in 2026 is more complicated than at any point since it acquired safe haven status. Japan’s Bank of Japan raised rates for the first time in seventeen years in 2024 and has signalled further normalisation in 2025 and 2026. As Japanese interest rates rise, the yen-funded carry trade gradually loses its structural rationale — borrowing yen becomes more expensive, reducing the aggregate short position that creates the mechanical safe haven demand in crises. In August 2024, a single BOJ policy signal caused the yen to surge and the Nikkei to fall 12% in a single day as carry trades unwound catastrophically. As the BOJ continues to normalise, the yen’s safe haven status may paradoxically weaken even as Japan’s economic fundamentals improve — because the carry trade mechanics that drove it are the same ones that are now being dismantled. The USD/JPY rate at 149.30 in March 2026 reflects a market that is still uncertain about the pace and extent of Japanese monetary normalisation.

Chapter 07 — The Forward View Which Currencies Will the World Trust Next?

Projecting safe haven currency status over a five to ten year horizon requires accepting a fundamental limitation: safe haven status has historically taken decades to build and sometimes only a single crisis to permanently damage. The British pound lost its reserve status in a slow-motion collapse between 1914 and 1944. The dollar’s post-Bretton Woods dominance was predicted to be brief in 1971 and has persisted for fifty-five years. The Swiss franc’s safe haven reputation was built between 1914 and 1939 and has never seriously been threatened. With that caveat, the analytical framework for the coming years is reasonably clear.

The Swiss franc’s safe haven status appears the most structurally secure. Switzerland has no meaningful political risk, no fiscal imbalance, no central bank credibility problem, and no military entanglement. Its only vulnerability is the size problem: Switzerland’s financial markets are not large enough to absorb a wholesale global reallocation of reserves away from the dollar. In a scenario where the world is looking for a dollar alternative at sovereign scale, the franc cannot fill the gap — it would simply surge to levels that would destroy the export economy and force SNB intervention. The franc remains the world’s best individual portfolio safe haven, not a systemic reserve alternative.

The yen’s trajectory over the next five years is the most uncertain of the three traditional safe havens. If the BOJ successfully normalises Japanese monetary policy — raising rates toward 1-2% and dismantling the yield curve control framework — the carry trade that mechanically creates yen safe haven demand will shrink. A yen that no longer appreciates in crises due to carry unwind would need to attract safe haven flows on fundamental grounds: and Japan’s demographics, debt burden, and persistent deflationary tendencies do not readily make that case. The yen’s next decade is likely to see it transition from mechanical safe haven to conventional currency — one that moves primarily in response to interest rate differentials and trade flows rather than global risk sentiment.

The dollar’s trajectory depends almost entirely on US political institutions. The structural foundations of dollar dominance — the deepest capital markets, the most liquid government bond market, the currency of global trade invoicing — remain intact. There is no alternative at comparable scale. The renminbi’s capital controls, the euro’s fiscal fragmentation, and gold’s lack of a digital settlement mechanism all mean that a sudden shift away from the dollar is logistically impossible in the near term. What is possible — and what 2025 demonstrated is already occurring — is a gradual diversification: central banks holding slightly less in dollars and slightly more in euros, yen, gold, and non-traditional currencies. This slow-motion de-dollarisation does not end dollar dominance. It erodes it, percentage point by percentage point, over decades.

| Currency | Safe Haven Since | Primary Mechanism | 2026 Status | 2030 Outlook | Key Risk |

|---|---|---|---|---|---|

| CHF | 1914 (WWI) | Neutrality, fiscal discipline, SNB credibility | Strongest active SH | Durable | SNB intervention at extreme levels |

| JPY | Mid-1990s (carry trade) | Carry trade unwind mechanics | Mechanical / fading | Diminishing | BOJ normalisation removes the carry dynamic |

| USD | 1944 (Bretton Woods) | Reserve dominance, market depth, funding currency | Contested | Contested | Policy unpredictability, institutional erosion |

| EUR | Partial, crisis-dependent | Large market, current account surplus | Partial beneficiary | Gradual gain | Fiscal fragmentation across member states |

| XAU (Gold) | Pre-history | Non-sovereign store of value | Surging | Structural bull | Illiquid for large-scale settlement |

| CNY | Not yet | Trade settlement, Belt and Road | Challenger | Emerging | Capital controls, trust deficit, governance |

The most analytically interesting projection for the next five years is not which single currency will dominate — it is whether the world is moving toward a multipolar safe haven system for the first time since the nineteenth century, when the pound was the unambiguous anchor. If de-dollarisation continues at the pace of the past decade, if the BOJ’s normalisation reduces the yen’s crisis-appreciation mechanics, and if Swiss franc appreciation prompts SNB interventions that limit its accessibility, the world may find itself in a situation unprecedented in modern finance: no single currency commands unambiguous safe haven consensus. In that scenario, gold — the one asset that answers to no central bank and no government — stands to be the primary beneficiary. The record central bank gold buying of 2022, 2023, 2024, and 2025 suggests that central bank reserve managers have already drawn this conclusion, even if they have not publicly stated it.

The Safe Haven Bull and Bear Cases — 2026 to 2031

What the structural data actually says · Not forecasts · The analytical framework for where trust flows

- Dollar’s Liberation Day failure to rally confirms what structural analysis has suggested: the dollar is a safe haven only in crises of external origin, not crises of US policy origin. More US policy volatility means more exceptions to the rule.

- Franc strengthens further as US political uncertainty persists. CHF at 0.85 or even 0.80 per dollar by 2028 is analytically plausible if dollar erosion continues at 2025 pace. SNB may intervene but cannot indefinitely resist structural flows.

- Gold at $6,000–$8,000 by 2030 is consistent with the trajectory of central bank buying, de-dollarisation, and a world where no single currency commands universal safe haven consensus.

- Euro gradually absorbs safe haven flows as it benefits from dollar uncertainty without being the crisis epicentre. EUR/USD at 1.15–1.20 by 2028 consistent with modest structural improvement in euro’s reserve role.

- BOJ normalisation causes yen carry trade to shrink, reducing crisis volatility but not eliminating yen as a factor in cross-asset risk events.

- A multipolar safe haven system — CHF for individual portfolios, dollar for systemic crises, gold for sovereign reserves — emerges as the dominant structure by 2028–2030.

- No alternative to the dollar exists at systemic scale. The renminbi has capital controls. The euro has fiscal fragmentation. The franc is too small. Gold cannot be digitally settled. When a true global crisis hits, the world defaults to the dollar by necessity, not preference.

- US 2026 midterm elections bring policy moderation. Tariff war de-escalates. Fed independence reaffirmed. Dollar recovers lost ground as political risk premium unwinds.

- US financial markets remain the deepest, most liquid on earth — by a margin no other market comes close to matching. Depth is the non-negotiable prerequisite for reserve currency status. It cannot be built quickly.

- The dollar’s 2025 weakness was cyclical not structural — driven by specific policy choices that can be reversed, not by irreversible structural deterioration of the US economy or institutions.

- AI investment flows into US technology assets continue to generate dollar demand that partially offsets reserve diversification trends.

- The DXY has recovered from previous 10%+ drawdowns — in 2008, 2011, and 2020 — each time returning to structural dominance within 18 months of the initial sell-off.

The most honest characterisation of the safe haven currency landscape in March 2026 is that the world is between systems. The dollar-dominant order that Bretton Woods established in 1944 is not collapsing — but it is, for the first time since 1971, visibly eroding. The 2025 Liberation Day episode was historically significant not because the dollar fell — it has fallen before — but because it fell during a risk-off episode when it had always previously risen. The rule that “in a crisis, the dollar rises” was broken. Rules that were broken once are never quite unbreakable again.

The Swiss franc has never been more clearly the world’s cleanest individual safe haven. Its 2025 performance against the dollar and euro, combined with its 110-year track record, places it in a category that no other currency can currently claim with equal authority. The franc’s limitation — market size — is real, but for individual portfolio protection rather than sovereign reserve reallocation, it remains the single most reliable refuge available.

The yen’s safe haven future is in transition. The BOJ’s gradual normalisation is dismantling the carry trade mechanics that created yen safe haven demand. This does not mean the yen will stop being a safe haven. It means the mechanism by which it performs that function will change — and the transition is likely to be volatile, with episodes like August 2024 becoming more rather than less frequent in the short term as the aggregate carry position is unwound.

The most important structural trend for the next five years is not any individual currency’s performance. It is the multi-decade, slow-motion fragmentation of reserve currency concentration away from the dollar — and the corresponding rise of gold as the only truly neutral reserve asset that every central bank can hold without creating a geopolitical statement. The message being sent by central bank gold buying is not that the dollar is dead. It is that the dollar is no longer unquestionable. And in a world where the dollar is no longer unquestionable, the architecture of safe haven currencies must, eventually, look different from the one that has existed since 1944.

Frequently Asked Questions on Safe Haven Currencies

Every question the market is asking · answered analytically

Conclusion: The Geography of Fear Is Changing

Eighty years. That’s how long the dollar held a single rule without a single exception: when the world panics, the dollar rises. It rose after the oil shock. It rose in 2008, even though 2008 was America’s own crisis. It rose when the US credit rating was downgraded. For eight decades, every investor on earth had the same reflex, the same muscle memory: sell the risky stuff, buy dollars, buy Treasuries, breathe again.

Then April 2, 2025 happened. The reflex failed. Stocks fell. Treasuries fell. And the dollar fell. All three at once — which was supposed to be structurally impossible, because the whole architecture of global safe haven demand was built on the assumption that at least one of those three would hold. None of them held. And when the eighty-year rule breaks, it doesn’t unbreak. Ever.

The franc is now the world’s clearest safe haven. 110 years without a serious failure. The deficit: it’s too small to be the world’s reserve currency. The advantage: that doesn’t matter for portfolio protection. The yen is transitioning — slowly, violently in episodes, toward a more ordinary currency. The dollar is contested — still dominant, still irreplaceable in systemic crises, but no longer unquestionable when the US itself is the source of the fear. The euro is still waiting for fiscal union. The renminbi is still trapped behind capital controls. Gold is rising — past $5,200 an ounce — because central banks are buying it in record amounts and they wouldn’t be doing that if they believed the current system was fine.

The geography of fear is changing. Slowly. Percentage point by percentage point, crisis by crisis, reserve reallocation by reserve reallocation. Not a revolution. A slow-motion rerouting of the world’s trust. The dollar will remain the anchor for years, probably decades — but dominant the way the pound was dominant between 1931 and 1944: by inertia and the absence of a ready replacement, not by unquestioned confidence. There is a difference. The market in 2026 is beginning to understand it.

A safe haven currency isn’t where your money is safe. It’s where your money feels safe. The difference between those two things — that gap between the feeling and the fact — is where every great monetary transition in history has hidden, waiting to be discovered.

Published March 26, 2026 by The Capital Dispatch at Capital Street FX (capitalstreetfx.com). For informational and educational purposes only. Not financial advice. Not investment guidance.