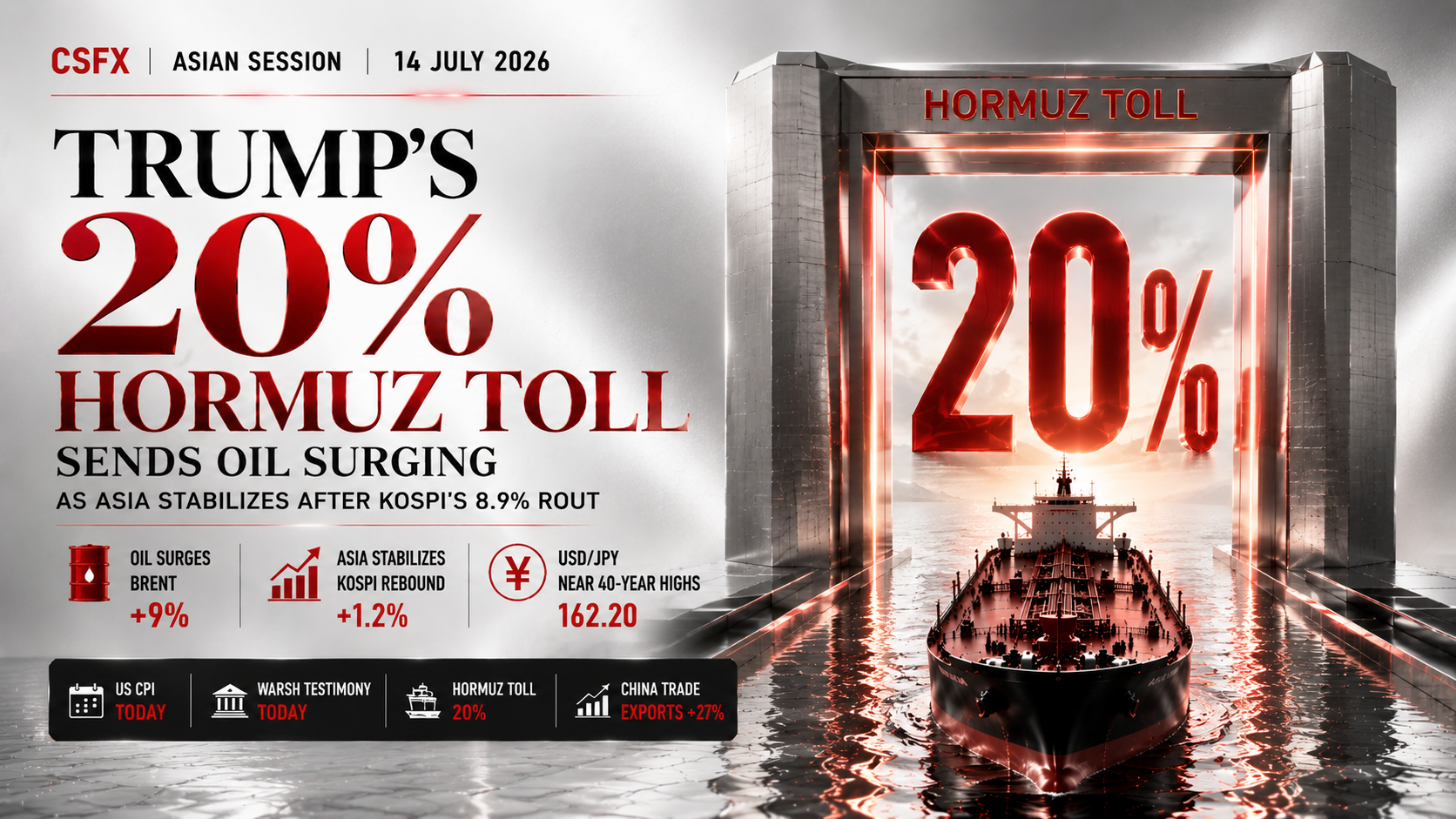

Trump’s 20% Hormuz Toll Sends Oil Surging as Asia Stabilizes After KOSPI’s 8.9% Rout; Yen Holds Near 40-Year Lows Ahead of Warsh Testimony & US CPI | Asian Session Technical Analysis | 14 July 2026

Trump’s 20% Hormuz Toll and Reinstated Iran Blockade Send Oil Surging Anew as Asia Stabilizes After Monday’s KOSPI Rout; Yen Holds Near 40-Year Lows Ahead of Warsh Testimony and US CPI

Asia claws back some stability after Monday’s KOSPI rout as Trump’s new 20% Hormuz toll and reinstated Iran blockade keep oil elevated, while the Yen holds near 40-year lows and traders brace for Fed Chair Warsh’s testimony and today’s US CPI print.

Tuesday’s Asian session has opened in a more tentative, stabilizing tone after Monday delivered one of the sharpest single-day shocks of the entire Gulf conflict, per live Reuters, Bloomberg, Investing.com and FXStreet coverage. President Donald Trump announced late Monday that the Strait of Hormuz “is OPEN, and will remain OPEN, with or without Iran,” while confirming the U.S. Navy is reinstating its blockade of Iranian shipping and that Washington will now charge a 20% toll on all non-Iranian cargo transiting the waterway, framing the U.S. as its new “guardian.” The announcement followed a weekend of renewed hostilities in which the U.S. military struck roughly 140 targets inside Iran after Tehran attacked a container ship in the strait, with Iran responding by firing at U.S. installations in Bahrain, Jordan and Kuwait, all of which reported their air defenses intercepted the incoming fire without casualties. Iran’s top military command has flatly rejected any U.S. role in managing the strait, and the United Nations’ shipping agency said Monday there is no legal basis for mandatory transit tolls, setting up a fresh point of contention even as actual tanker traffic has all but ground to a halt, with Kpler data showing only 12 authorized crossings on Sunday versus more than 100 a day before the war escalated.

Markets reacted forcefully to Monday’s news, and Tuesday’s session is largely about digesting the aftershock. Brent crude surged more than 9% on Monday, its biggest one-day gain since 2020, and remains elevated in the high-$70s a barrel into Tuesday’s Asian trade. Equities bore the brunt of the move: South Korea’s KOSPI cratered 8.9% on Monday — its worst session since SK Hynix’s blockbuster Nasdaq ADR listing — with SK Hynix itself plunging 15.4% and Samsung Electronics down more than 6%, as leveraged AI-memory positioning unwound violently. The S&P 500 fell 0.7% and the Nasdaq Composite dropped 1.4% overnight, with Nvidia down 3.2% and Micron off nearly 5%. Tuesday’s Asian session shows tentative signs of stabilization: Japan’s Nikkei 225 is up around 0.6% near 67,609, a modest bounce after Monday’s near-2% slide to a two-month low, the Topix has added roughly 0.5%, and South Korea’s KOSPI is rebounding close to 1.2% intraday, though still well below levels seen before this week’s chip-sector unwind began. Hong Kong’s Hang Seng is a touch softer, down around 0.5%, while Australia’s S&P/ASX 200 is little changed. A genuine bright spot for regional risk appetite came from China, where June trade data released this morning smashed forecasts: exports jumped 27% year-on-year, the fastest pace since 2021, and imports surged 36%, both powered by surging global demand for AI-related chips and data-center hardware, pushing the monthly trade surplus to $125.6 billion, up from $105.4 billion in May.

Currency and rates markets remain dominated by the Gulf-driven inflation scare and the looming double catalyst of Fed Chair Kevin Warsh’s first congressional testimony and the U.S. June CPI report, both due later today. USD/JPY has held in the mid-162s, consolidating within striking distance of the four-decade high touched earlier this month, as the roughly 250-275 basis point Fed-BOJ policy gap continues to draw carry-trade flows toward the Dollar even as looming Japanese intervention risk caps the pair’s upside. NZD/USD has recovered to around 0.5795, narrowing the gap to its 200-day moving average near 0.5819 even as it remains below that average for a 25th consecutive session, as a hawkish Reserve Bank of New Zealand backdrop, with swaps traders pricing two further quarter-point hikes, combines with today’s blowout China trade data to help the Kiwi claw back a portion of Monday’s Gulf-driven slide. In commodities, Copper has surged toward $6.39 a pound as intensifying concerns over a worsening sulphuric-acid supply shortage outweigh the earlier Dollar-strength headwind tied to Monday’s Hormuz headlines, while Natural Gas has extended its slide to around $2.88 per MMBtu, largely insulated from Gulf-driven price action given America’s domestic supply position, but pressured by a deepening storage surplus even as above-normal summer temperatures lift power-sector demand. In digital assets, Litecoin has slipped more than 3% to around $42.69, its Relative Strength Index deep in oversold territory, while Solana has fallen toward $73.85, now testing the key 0.786 Fibonacci retracement support near $73 that has repeatedly capped downside on prior pullbacks, both pressured by a broader crypto risk-off tone tied to the weekend’s Gulf escalation. Looking ahead through the remainder of the Asian session, the decisive variables are any further Hormuz-toll or blockade-related headlines, China’s Q2 GDP release due Wednesday, and positioning ahead of today’s CPI print and Chair Warsh’s testimony before Congress.

Sessions this volatile reward traders who can react in seconds, not minutes. Capital Street FX clients trade this Hormuz-driven volatility on 0.0 Pips Spreads with 1:10000 Leverage, across 2000+ Instruments spanning FX, indices, commodities and crypto — backed by 24/7 Live Support for exactly this kind of headline-driven session.

Asian Session Headlines

The stories driving price action across equities, commodities, currencies and crypto this session

Asian Session Economic Calendar — 14 July 2026

Key releases and events shaping price action across today’s Asian session (times local/ET as noted)

| Time | Event | Actual / Detail | Impact | Market Read |

|---|---|---|---|---|

| 🇺🇸Monday PM | Trump Reinstates Iran Blockade, Proposes 20% Hormuz Toll | U.S. declared “guardian” of the strait; Iran’s military command rejects any U.S. role; UN shipping body disputes toll’s legal basis | 🔴 CRITICAL | Reignites the Gulf-driven oil and risk-off shock into Tuesday’s Asian open |

| 🇳🇷Today, 09:00 CST | China June Trade Balance | Exports +27% YoY (vs. +18.5% forecast); imports +36% YoY; surplus $125.6B | 🔴 CRITICAL | A major AI-driven upside surprise that helps offset Gulf-related regional risk-off |

| 🇰🇷Today, Asia Open | Brent & WTI Crude Oil | Brent holding in the high-$70s after Monday’s 9%-plus surge, the biggest since 2020 | 🔴 CRITICAL | Keeps the inflation debate front and center just ahead of today’s US CPI report |

| 🇰🇷Today | South Korea KOSPI | Rebounds roughly 1.2% after Monday’s 8.9% plunge; SK Hynix and Samsung steadying | 🔴 CRITICAL | Tentative sign of stabilization after the sharpest AI-memory unwind of the year |

| 🇯🇵Today | Nikkei 225 / Topix | Nikkei up ~0.6% near 67,609; Topix up ~0.5%, both recovering a sliver of Monday’s losses | 🟢 MEDIUM | Modest stabilization, though the index remains near a two-month low |

| 🇳🇰Today | Hong Kong Hang Seng | Softer by around 0.5%, tracking the region-wide cautious tone | ⚪ LOW | Modest underperformance versus the rebound seen in South Korea and Japan |

| 🇳🇰Wednesday | China Q2 GDP, June Retail Sales & Industrial Output | Due Wednesday; strong trade data raises the bar for a solid growth print | 🟢 MEDIUM | Key confirmation of whether China’s recovery has legs into H2 2026 |

| 🇺🇸Today | US June CPI Report | Goldman Sachs expects core CPI to ease toward 2.8% year-on-year; headline seen near 4.2% before oil’s renewed climb | 🔴 CRITICAL | Today’s single biggest catalyst for Fed-hike pricing, the Dollar and Treasury yields |

| 🇺🇸Today | Fed Chair Kevin Warsh Congressional Testimony | First appearance before Congress since taking office in May 2026 | 🔴 CRITICAL | Markets will parse Warsh’s tone for confirmation of hawkish repricing seen this week |

| 🇳🇳This Week | RBNZ Commentary & Rate-Hike Pricing | Swaps traders fully pricing two further quarter-point RBNZ hikes | 🟢 MEDIUM | Offers the Kiwi some underlying support even as today’s risk-off tone dominates |

Asian Session Trade Ideas — 14 July 2026

Seven structured setups — USD/JPY, NZD/USD, Copper, Natural Gas, Nikkei 225, Litecoin, Solana — with updated prices, levels, and full fundamental and technical analysis

USD/JPY

Fundamental Backdrop

USD/JPY is consolidating near 162.29 in the mid-162s, holding within striking distance of the four-decade high touched earlier this month, as the Dollar draws renewed safe-haven demand following Monday’s dramatic Hormuz toll and blockade announcement. Persistent Yen weakness continues to reflect a wide 250-275bps rate gap between the Fed’s 3.50-3.75% target and the BOJ’s 1.0% policy rate, which keeps carry-trade flows firmly in the Dollar’s favour. Traders remain reluctant to place large fresh directional bets ahead of today’s dual catalysts — the US June CPI report and Fed Chair Kevin Warsh’s first congressional testimony — both of which carry outsized importance for the pace of further Fed tightening. Looming Japanese intervention risk, given the currency’s proximity to 40-year lows, continues to cap enthusiasm for aggressive upside bets even as the broader trend remains firmly Dollar-supportive.

Technical Outlook

USD/JPY has held a tight consolidation range in the mid-162s after Monday’s close near 161.70, with the pair’s structure still pointed higher within its multi-month uptrend toward fresh 40-year highs. Resistance sits at 162.85 (the 52-week high) and 163.80 (this trade’s target, the next psychological level above the multi-decade peak). Support lies at 161.50 (this trade’s buy-dip level, near Monday’s range) and 161.00 (this trade’s stop, the next Fibonacci confluence). A confirmed close above 162.85 would expose fresh multi-decade highs, while a break below 161.00 would risk a deeper pullback toward 159.50, particularly if verbal or actual intervention chatter intensifies out of Tokyo.

Session Catalysts

Watch for: (1) today’s US CPI report and its implications for Fed-hike pricing and the Dollar side of the pair; (2) Fed Chair Kevin Warsh’s first congressional testimony and whether his tone confirms the hawkish repricing seen this week; (3) any official verbal or actual intervention signals from Japanese authorities given the currency’s proximity to 40-year lows; (4) further Hormuz-related headlines that could shift safe-haven Dollar demand; (5) intervention data due later this month that could confirm or deny recent suspected official action.

Trade USD/JPY and 60+ FX pairs on 0.0 Pips Spreads at Capital Street FX.

NZD/USD

Fundamental Backdrop

NZD/USD has rebounded to around 0.5795 in early Asian trade, narrowing the gap to its 200-day Simple Moving Average near 0.5819 even as it remains below that average for a 25th consecutive session. The pair had slid 0.12% during Monday’s North American session as the Greenback posted broad gains amid rising geopolitical tensions and hawkish comments from a Fed Governor, but has clawed back the bulk of that move during Asian hours as today’s much stronger-than-expected China trade data, with exports up 27% year-on-year, offers a genuine tailwind for the Kiwi given New Zealand’s reliance on Chinese demand. That is being reinforced by the Reserve Bank of New Zealand’s hawkish stance, with swaps traders now fully pricing two additional quarter-point hikes; RBNZ Chief Economist Paul Conway warned inflation may not ease as quickly as the central bank expects. The lingering Gulf-driven risk-off tone remains a headwind that could cap further upside if broad safe-haven Dollar demand reasserts itself later in the session.

Technical Outlook

NZD/USD has cleared Monday’s daily high of 0.5789 to trade around 0.5795, now pressing directly into the 0.5800 psychological level just below its 200-day moving average near 0.5819. Momentum, as measured by the Relative Strength Index, has turned firmer intraday, though the pair remains within its broader downward-biased structure until it can reclaim the 200-day average on a closing basis. Resistance sits at 0.5800 (this trade’s sell-rally level, the immediate barrier) and 0.5840 (this trade’s stop, just above the 200-day average). Support lies at the psychological 0.5700 figure, and below that the 8 July low of 0.5672 (this trade’s target zone), followed by 0.5650. A confirmed close above 0.5840 would open a bullish continuation toward the 200-day average and beyond, while rejection at 0.5800-0.5819 would favor a fade back toward these lower support levels.

Session Catalysts

Watch for: (1) any further Hormuz-related escalation or de-escalation headlines that drive broad risk sentiment; (2) China’s Q2 GDP data due Wednesday, given New Zealand’s reliance on Chinese demand; (3) further RBNZ commentary on the inflationary outlook and additional hike signalling; (4) today’s US CPI report and its implications for Fed policy and the Dollar; (5) broad Dollar positioning ahead of Chair Warsh’s congressional testimony.

Amplify high-conviction setups like this with 1:10000 Leverage at Capital Street FX.

Copper

Fundamental Backdrop

Copper has surged to around $6.39 a pound, rallying more than 3.5% intraday as easing Dollar momentum during Asian trade and intensifying supply-side concerns overwhelm the metal’s earlier Hormuz-driven Dollar-strength headwind. LME three-month copper has jumped in sympathy overnight, with the rally increasingly framed around a worsening shortage of sulphuric acid used in refining, a structural constraint on global smelter output that is now dominating price action across the base-metals complex, including aluminium, zinc, lead, nickel and tin. Copper, often viewed as a barometer of global economic health, is also drawing support from today’s blowout China trade data, which underscored resilient demand for industrial and AI-related hardware from the world’s largest metals consumer. Markets continue to price at least one further Fed rate hike this year, a dynamic that would ordinarily strengthen the Dollar and weigh on metals, but today’s supply-driven repricing is proving the dominant force in the session.

Technical Outlook

Copper has broken sharply higher from Monday’s close near $6.17 to trade around $6.39, decisively clearing the prior range-top resistance near $6.22 and $6.30 and reversing what had been a roughly 4.85% corrective move over the past month; the metal is now about 15% higher than a year ago. Resistance sits at $6.50 (a near-term psychological level) and $6.65 (this trade’s target, the next measured-move objective above the breakout). Support lies at $6.28 (this trade’s buy-dip level, the former resistance-turned-support zone) and $6.15 (this trade’s stop, back inside the prior range). A confirmed close above $6.50 would open a path toward $6.80, while a failure to hold $6.15 would risk a false-breakout retest of $6.00.

Session Catalysts

Watch for: (1) broad Dollar direction as Hormuz-toll headlines and today’s CPI print evolve through the session; (2) China’s stronger-than-expected trade data and Wednesday’s GDP release, given China’s outsized share of global copper demand; (3) any fresh supply-side disruption news, including sulphuric acid availability tied to Middle East refining capacity; (4) Fed Chair Warsh’s testimony and its read-through for Fed policy and industrial financing costs; (5) broader risk sentiment across base metals as regional equities attempt to stabilize.

Copper is one of 2000+ Instruments available to trade at Capital Street FX.

Natural Gas

Fundamental Backdrop

Natural Gas has extended its slide to around $2.88 per MMBtu, down roughly 6% from Monday’s close, largely insulated from the Gulf turmoil given the U.S.’s domestic supply position but pressured by a larger-than-expected storage build that has pushed working inventories further above the five-year average toward the upper end of recent estimates. Above-normal temperatures across the central and eastern U.S. have pushed electric-power demand for gas-fired generation up more than 15% week-on-week according to Rystad Energy data, yet Henry Hub futures have broken decisively below the $3.15-$3.34 range that had defined trading since mid-June, as strong supply fundamentals, including record Lower 48 production led by growth in the Permian region, continue to outweigh demand-side support. The EIA’s latest Short-Term Energy Outlook projects Henry Hub spot prices averaging $3.57/MMBtu in the fourth quarter, still below year-ago levels, underscoring how comfortably supply is keeping pace with rising demand even during peak summer cooling season.

Technical Outlook

Natural Gas has broken down sharply from Monday’s close near $3.10 to trade around $2.88, decisively clearing what had been the lower end of the summer consolidation range and opening a fresh leg lower. Resistance sits at $2.98 (this trade’s sell-rally level, the former range-low-turned-resistance) and $3.08 (this trade’s stop, back inside the broken range). Support lies at $2.80 (a near-term pivot) and $2.72 (this trade’s target, the next Fibonacci extension below the range). A confirmed close below $2.72 would expose a deeper move toward $2.60, while a reclaim of $3.08 would shift the near-term bias back toward the middle of the prior summer range.

Session Catalysts

Watch for: (1) updated weather forecasts and whether above-normal temperatures persist through the back half of July, sustaining power-sector demand; (2) this week’s EIA storage injection data and how it compares with the five-year average; (3) any LNG feedgas disruptions, including planned Freeport LNG maintenance; (4) broader Dollar and rates direction following today’s CPI print, which can influence energy-sector positioning; (5) Lower-48 production trends, which have recently eased slightly from December’s record highs.

New to commodities trading? Claim a deposit bonus when you open an account at Capital Street FX.

Nikkei 225

Fundamental Backdrop

The Nikkei 225 is up modestly around 0.6% near 67,609, clawing back a small part of Monday’s near-2% decline to a two-month low, a session that erased 1,361 points as Taiyo Yuden, Yaskawa Electric and Murata Manufacturing led the retreat amid broad Gulf-driven risk aversion. Today’s stabilization is helped by China’s blowout June trade data, with exports up 27% year-on-year on booming AI-hardware demand, a tailwind for Japan’s export-heavy, semiconductor-supply-chain-linked market. Even so, rising energy costs tied to oil’s Hormuz-driven surge remain a genuine headwind, particularly given Japan’s near-total reliance on imported energy, and June producer prices already running at a multi-year high pace of 7.1% year-on-year. The Yen’s continued weakness near 40-year lows offers exporters some offsetting earnings support, a dynamic that has repeatedly cushioned the index during past bouts of Gulf-related volatility.

Technical Outlook

The Nikkei 225 has stabilized from Monday’s close near 67,197 to trade around 67,609, though the index remains firmly below the 52-week high near 72,832 set in June and closer to its recent two-month low. Resistance sits at 67,900 (this trade’s sell-rally level, near Monday’s earlier session high) and 68,400 (this trade’s stop, the next supply zone). Support lies at 66,800 (a near-term pivot) and 66,200 (this trade’s target, near last week’s low). A confirmed close below 66,200 would risk a deeper retest of the 65,000 area, while a reclaim of 68,400 would shift the near-term bias back toward last week’s higher levels.

Session Catalysts

Watch for: (1) any further Hormuz-toll or blockade-related headlines that could reignite regional risk-off flows; (2) China’s Q2 GDP, retail sales and industrial output data due Wednesday, key for regional sentiment; (3) continued read-through from South Korea’s chip-sector unwind and whether it stabilizes further; (4) today’s US CPI report and Fed Chair Warsh’s testimony, both influential for global risk appetite; (5) any fresh BOJ policy signals or intervention chatter given the Yen’s proximity to 40-year lows.

Questions on index positioning during fast-moving sessions like this? Reach 24/7 Live Support at Capital Street FX.

Litecoin

Fundamental Backdrop

Litecoin has slipped over 4% to around $42.69, with a 24-hour range between $42.50 and $44.62, as the weekend’s Hormuz escalation drives a broad risk-off move across digital assets. LTC’s market capitalization has fallen to roughly $3.30 billion, and the token’s daily Relative Strength Index sits deep in oversold territory near 20, a level technically associated with stretched downside but which has, in prior sessions, coincided with a further grind lower rather than an immediate reversal. Broader market sentiment for Litecoin remains bearish, consistent with a wider pullback across older, lower-beta altcoins as traders rotate into cash or Bitcoin during acute risk-off episodes. The token continues to trade well below the psychologically significant $50 level that capped several rebound attempts earlier this year, and is now approaching the $42.30 pivot support that anchors this trade’s outlook.

Technical Outlook

Litecoin has extended its slide from a 24-hour high near $44.62 to trade around $42.69, continuing a short-term downtrend that has taken the token roughly 4% lower over the past day and kept it consolidating well below its 50-day moving average. Resistance sits at $45.50 (this trade’s sell-rally level, near the 50-day EMA) and $46.80 (this trade’s stop, the next supply zone). Support lies at $42.30 (the classical pivot point’s strongest support, now just below current price) and $40.00 (this trade’s target, a key psychological level). A confirmed close below $40.00 would expose a deeper move toward the low-$30s, while a reclaim of $46.80 would shift the near-term bias back toward the recent range highs.

Session Catalysts

Watch for: (1) Bitcoin’s own directional cues, given the historically tight correlation between BTC and legacy altcoins like LTC during risk-off events; (2) any further Hormuz-related headlines that could deepen the broader crypto selloff; (3) whether the deeply oversold RSI reading triggers a near-term technical bounce; (4) broader altcoin performance, including Solana, as a read on whether today’s weakness is idiosyncratic or market-wide; (5) today’s US CPI print and its implications for risk appetite across speculative assets.

Trade Litecoin and other majors on 0.0 Pips Spreads across 2000+ Instruments at Capital Street FX.

Solana

Fundamental Backdrop

Solana has fallen to around $73.85, sitting directly on the long-term 0.786 Fibonacci retracement near $73 that has capped the token’s downside on prior pullbacks, as Monday’s Hormuz escalation drives a broad risk-off move across digital assets. SOL remains well below its all-time high and has round-tripped much of its early-July recovery, with the broader structural picture still fragile even as tokenized real-world-asset value on the network has grown to roughly $3.5-3.6 billion, up more than 36% over the past 30 days, and spot volumes for tokenized assets hit a Q2 2026 high of $5.77 billion. Institutional flows have been notably resilient on the ETF side, with Morgan Stanley amending its proposed Solana ETF filing to a 0.14% fee, the lowest among U.S. crypto ETFs, underscoring how forcefully macro and geopolitical risk-off sentiment is currently dominating token-specific fundamentals despite continued structural progress.

Technical Outlook

Solana’s decline from Monday’s close near $78.40 has taken price down to $73.85, now sitting right on the critical 0.786 Fibonacci support near $73 that marks the last major floor before deeper downside would open up. Resistance sits at $76.00 (near-term pivot, former support) and $79.00 (this trade’s sell-rally level, near Monday’s close), with $82.00 as this trade’s stop (the 50-day/100-day moving average confluence). Support lies at $73.00 (the critical Fibonacci zone the token is now testing) and $70.00 (this trade’s target, just below that zone). A confirmed close below $73 would risk an extension toward $65-$68, while a bounce off this support and reclaim of $76 would shift the near-term bias back toward the 50-day and 100-day moving averages.

Session Catalysts

Watch for: (1) Bitcoin’s own directional cues, given the historically tight correlation between BTC and SOL during risk-off events; (2) any further Hormuz-related developments that could deepen the broader crypto selloff; (3) continued ETF and institutional fund-flow data for Solana-linked products, including the low-fee Morgan Stanley filing; (4) progress on infrastructure catalysts including the Firedancer validator rollout; (5) broader altcoin performance, including Litecoin, as a read on whether today’s weakness is idiosyncratic or market-wide.

Trade Solana and 40+ digital assets with 1:10000 Leverage and a welcome deposit bonus at Capital Street FX.

Asian Session FAQ

Common questions about today’s key market movers, answered

Asian Session Summary — Tuesday, 14 July 2026 (Updated Mid-Session)

Tuesday’s Asian session is defined by a tentative stabilization following one of the sharpest single-day shocks of the four-month-plus Gulf war, per live Reuters, Bloomberg, Investing.com and FXStreet coverage. President Trump’s Monday announcement that the U.S. is reinstating its naval blockade of Iranian shipping and imposing a 20% toll on all non-Iranian cargo transiting the Strait of Hormuz sent Brent crude surging more than 9%, its biggest one-day gain since 2020, and triggered an 8.9% plunge in South Korea’s KOSPI as SK Hynix cratered 15.4% and Samsung Electronics fell over 6% in a violent unwind of leveraged AI-memory positioning. Today’s session shows early signs of stabilization rather than a fresh leg lower: Japan’s Nikkei 225 is up around 0.6% near 67,609, South Korea’s KOSPI is rebounding roughly 1.2%, and Hong Kong’s Hang Seng is only modestly softer, while a genuine bright spot came from China’s June trade data, which smashed forecasts with exports up 27% year-on-year on booming AI-hardware demand, pushing the trade surplus to $125.6 billion. Oil holds a large share of Monday’s gains, keeping the inflation debate front and center just ahead of today’s US CPI report and Fed Chair Kevin Warsh’s first congressional testimony, both landing later today. USD/JPY has held in the mid-162s, just off a four-decade high, as the wide Fed-BOJ rate gap continues to draw carry flows even as Japanese intervention risk caps further upside, while NZD/USD has rebounded toward 0.5795, narrowing the gap to its 200-day moving average, as a hawkish RBNZ backdrop and today’s blowout China trade data help the Kiwi claw back Monday’s Gulf-driven slide. In commodities, Copper has surged toward $6.39 a pound on intensifying supply-side concerns, while Natural Gas has slid to around $2.88 per MMBtu on a deepening storage surplus that continues to outweigh above-normal summer demand. In digital assets, Litecoin has fallen over 4% to around $42.69 and Solana has eased toward $73.85, testing key Fibonacci support near $73, both pressured by the broader crypto risk-off tone. Highest-conviction session idea: fade the Yen’s safe-haven bid by buying USD/JPY dips toward 161.50, targeting 163.80 — the combination of a still-widening Fed-BOJ rate gap, fresh Hormuz-driven safe-haven Dollar demand, and today’s CPI/Warsh testimony catalysts together form a genuine near-term directional case, though escalating Japanese intervention risk near 40-year lows remains a real and growing headwind that could sharply reverse this move on short notice.

For the individual instruments: USD/JPY buy dips toward 161.50, stop 161.00, target 163.80 — the wide Fed-BOJ rate differential and renewed safe-haven Dollar demand are genuine tailwinds, though the pair’s proximity to 40-year lows keeps intervention risk from Japanese authorities a real and growing headwind. NZD/USD sell rallies toward 0.5800, stop 0.5840, target 0.5680 — broad Gulf-driven risk aversion is a genuine tailwind for this trade, though a hawkish RBNZ backdrop and today’s strong China trade data are real headwinds to a sustained move lower. Copper buy dips toward $6.28, stop $6.15, target $6.65 — intensifying sulphuric-acid supply concerns and today’s strong China trade data are genuine tailwinds to further upside, though a resumption of broad Dollar strength is a real risk to this trade. Natural Gas sell rallies toward $2.98, stop $3.08, target $2.72 — a deepening storage surplus is a genuine tailwind, though above-normal summer temperatures supporting power-sector demand are a real headwind to further downside. Nikkei 225 sell rallies toward 67,900, stop 68,400, target 66,200 — oil-driven energy-cost concerns and lingering regional risk-off are genuine tailwinds, though today’s stabilization and China’s blowout trade data are real headwinds to a sustained move lower. Litecoin sell rallies toward $45.50, stop $46.80, target $40.00 — broad crypto risk-off and a bearish technical structure are genuine tailwinds, though a deeply oversold RSI reading is a real risk of a near-term technical bounce. Solana sell rallies toward $79.00, stop $82.00, target $70.00 — the token’s approach toward key Fibonacci support and broad crypto risk-off are genuine tailwinds, though resilient ETF and institutional flow data are a real risk to further downside. The decisive variables for the remainder of the session are any further Hormuz-toll or blockade-related headlines, China’s Q2 GDP data due Wednesday, and today’s US CPI release and Chair Warsh’s testimony. Size positions accordingly, and note that the geopolitical backdrop remains exceptionally fluid and carries genuine event risk that could reshape sentiment sharply intraday.

Ready to act on today’s setups? Open an account with Capital Street FX and trade every instrument covered in this report on 0.0 Pips Spreads and 1:10000 Leverage, across 2000+ Instruments, with a welcome deposit bonus and 24/7 Live Support on hand for every session.

Access Live Asian Markets →