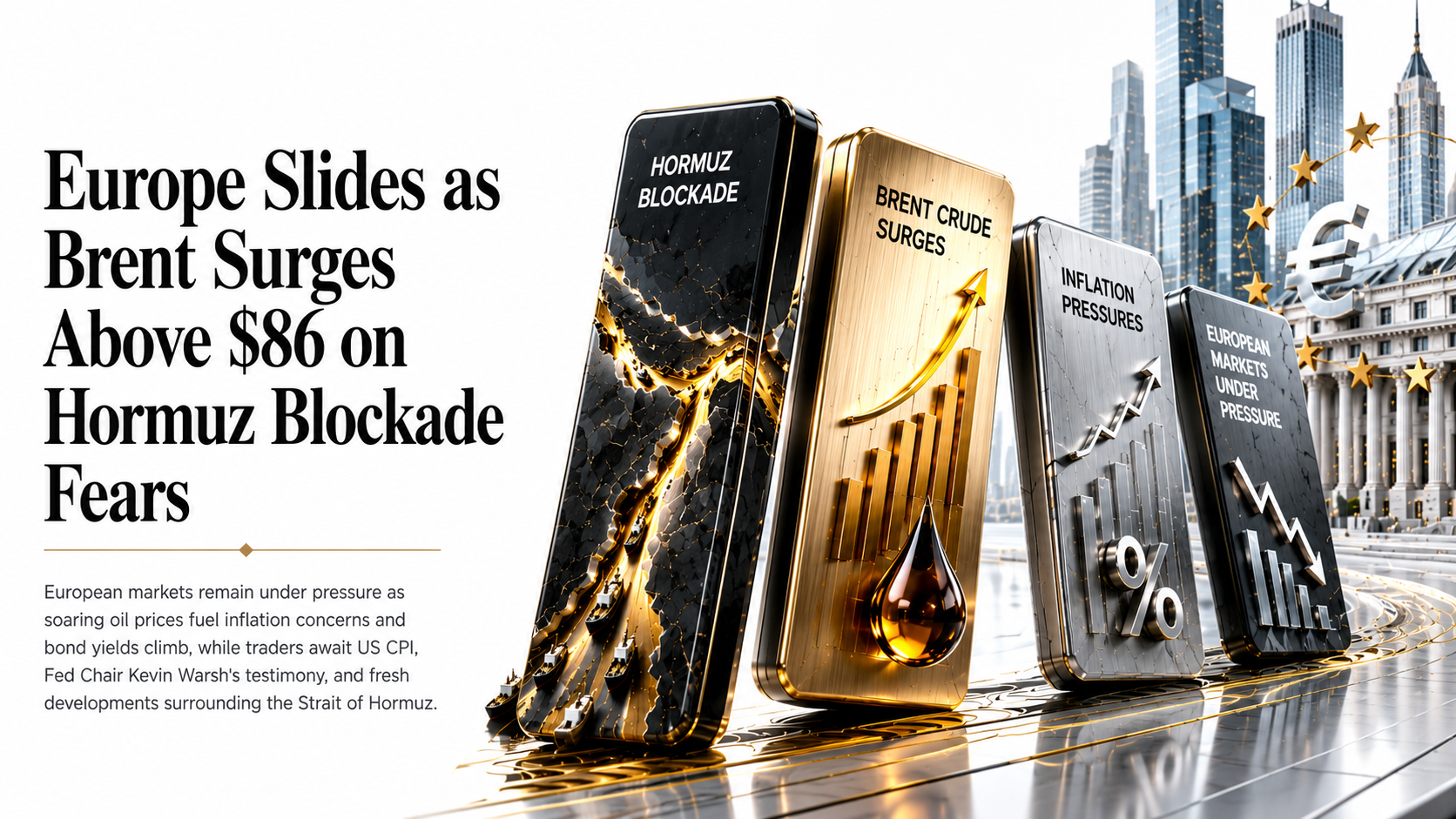

Oil Tops $86 as Trump’s Hormuz Blockade Takes Effect Today; Burnham Confirmed UK PM Steadies Sterling; Euro Bond Yields Surge Ahead of US CPI & Warsh Testimony | European Session Technical Analysis | 14 July 2026

Oil Tops $86 as Trump’s Reinstated Hormuz Blockade Takes Effect This Afternoon; Andy Burnham Confirmed as UK’s Next Prime Minister Steadies Sterling; Euro Area Bond Yields Surge Ahead of US CPI and Fed Chair Warsh’s Testimony

Brent tops $86 as Trump’s Hormuz blockade nears its 4pm ET deadline, European stocks slide and euro bond yields surge on inflation fears, while Burnham’s confirmation as UK PM steadies the Pound ahead of US CPI and Fed Chair Warsh’s testimony.

Tuesday’s European session has opened firmly under the shadow of the Gulf, per live Reuters, Bloomberg, Investing.com and FXStreet coverage. Brent crude has pushed above $86 a barrel, its highest level since mid-June and up more than 10% over the past week, as markets brace for President Donald Trump’s reinstated naval blockade of Iranian shipping to take effect at 4pm Eastern Time today, alongside his proposed 20% toll on all other cargo transiting the Strait of Hormuz. The move follows a third consecutive night of US strikes on Iran, with Tehran’s foreign minister rejecting the toll proposal as “too much” and the International Maritime Organization saying there is “no legal basis” for such charges, while Trump has said the Strait will remain open to commercial traffic “with or without Iran.” European equity markets are reflecting the unease: the FTSE 100 has eased to around 10,462.89, down roughly 0.2%-0.4% on the day, while Germany’s DAX and France’s CAC 40 are seeing sharper declines of around 0.4%-0.9%, with energy heavyweights such as BP and Shell providing only a partial offset as crude approaches multi-decade highs.

Fixed income markets are showing a textbook, if counter-intuitive, reaction to the Gulf escalation. Rather than the safe-haven bid that geopolitical shocks typically generate for sovereign debt, Euro Area government bond yields have instead surged as investors revisit inflation expectations tied to sustained higher energy costs. The Euro Area 20-Year yield is trading around 3.543%, up from roughly 3.46% just a week ago and higher by more than 19% over the past year, while Germany’s 10-year Bund yield posted its largest weekly increase in five weeks last week. ECB policymaker Yannis Stournaras warned Friday that the central bank is “back to square one” in its inflation fight, and markets are now pricing two further ECB rate hikes over the next year, with the first widely expected in September, all consistent with the sharp move higher in yields across the curve. Attention today turns to comments expected from ECB Executive Board member Isabel Schnabel and a scheduled German 2-year Schatz auction, both useful reads on how deeply this repricing has taken hold.

Currency markets are torn between the Dollar-supportive Gulf backdrop and idiosyncratic developments closer to home. EUR/USD has rebounded to around 1.1388 as the Dollar corrects lower ahead of today’s US June CPI report, due at 12:30 GMT, though FXStreet’s technical read still frames the pair’s near-term bias as bearish given it remains capped below its 20-period Exponential Moving Average at 1.1438 following Monday’s bearish flag breakdown. GBP/USD, meanwhile, has found genuine support from a domestic political resolution: former Greater Manchester mayor Andy Burnham has secured the backing of the vast majority of Labour MPs to replace Keir Starmer as the UK’s next Prime Minister, calming market concerns about a disorderly transition and helping the Pound hold most of its recent gains near 1.3352, even though broader Dollar demand tied to the Gulf escalation has nudged the pair modestly off its session high. In commodities, Silver has compressed to around $58.03 an ounce inside a tightening symmetrical triangle pattern even as the metal faces a sixth consecutive annual supply deficit of roughly 46.3 million ounces, while Wheat has extended its monthly climb to around 633.97 cents a bushel, up around 7.5% over the past month, as tighter US stocks and reports of Russian export restrictions through the Don-Azov channel add a fresh supply-side risk premium.

In digital assets, the split between Ethereum and XRP has been the standout story of the session. Ethereum is holding a constructive medium-term uptrend structure near $1,779.87, supported by continued institutional accumulation and record-low exchange reserves, while XRP has broken below the $1.07 Fibonacci support level it had defended for 158 consecutive days, now trading around $1.043 amid a broader crypto risk-off tone tied to the Gulf escalation and a stalled CLARITY Act in the US Senate. Looking ahead through the remainder of the European session, the decisive variables are today’s US CPI report, Fed Chair Kevin Warsh’s first congressional testimony before the House Financial Services Committee, any further Hormuz blockade or toll-related headlines as the 4pm ET deadline approaches, and the German Schatz auction and ECB commentary shaping the eurozone rates picture.

Sessions this event-heavy reward traders who can react in seconds, not minutes. Capital Street FX clients trade this Hormuz-driven volatility on our Zero Account‘s 0.0 Pips Spreads with 1:10000 Leverage, across 2000+ Instruments spanning FX, indices, commodities, bonds and crypto — backed by 24/7 Live Support for exactly this kind of headline-driven session.

European Session Headlines

The stories driving price action across currencies, bonds, equities, commodities and crypto this session

European Session Economic Calendar — 14 July 2026

Key releases and events shaping price action across today’s European session (CET/GMT and ET as noted)

| Time | Event | Actual / Detail | Impact | Market Read |

|---|---|---|---|---|

| 🇺🇸Monday PM | Trump Reinstates Iran Blockade, Confirms 20% Hormuz Toll | Blockade and toll formally scheduled to take effect at 4pm ET today; Iran’s foreign minister rejects the toll as “too much” | 🔴 CRITICAL | Sets up the session’s key deadline risk this afternoon |

| 🇬🇧Overnight | Andy Burnham Confirmed as UK’s Next Prime Minister | Secures backing of the vast majority of Labour MPs to replace Keir Starmer | 🔴 CRITICAL | Removes a source of domestic political uncertainty, supportive for GBP |

| 🇩🇪10:00 CEST | Germany 2-Year Schatz Auction | First major eurozone debt auction since last week’s sharp rise in Bund yields | 🟢 MEDIUM | Key read on near-term demand for eurozone paper amid the yield surge |

| 🇪🇺Today | ECB’s Isabel Schnabel Commentary | Comments expected on the inflation outlook following Stournaras’ “back to square one” warning | 🟢 MEDIUM | Could reinforce or push back against the market’s hawkish repricing |

| 🇬🇧Today | FTSE 100 / DAX / CAC 40 | FTSE ~10,462.89 (-0.2/-0.4%); DAX and CAC seeing sharper declines of ~0.4-0.9% | 🟢 MEDIUM | Broad European risk-off as oil-driven inflation fears dominate |

| 🇺🇸12:30 GMT / 08:30 ET | US June CPI Report | Consensus looks for headline near 3.8% YoY, down slightly on the month, core steady | 🔴 CRITICAL | Today’s single biggest catalyst for the Dollar, yields and risk appetite |

| 🇺🇸15:00 GMT / 11:00 ET | Fed Chair Kevin Warsh’s First Congressional Testimony | Appearance before the House Financial Services Committee on the semi-annual monetary policy report | 🔴 CRITICAL | Markets watching for confirmation of the hawkish tone set by Governor Waller |

| 🇺🇸16:00 ET | Hormuz Blockade and 20% Toll Formally Take Effect | Naval blockade of Iranian shipping resumes; toll applies to all non-Iranian cargo transiting the strait | 🔴 CRITICAL | Key deadline risk for oil, yields and broad risk sentiment into the US close |

| 🇺🇸Today | US Bank Earnings (JPMorgan, Wells Fargo, Citigroup) | Q2 results kick off the earnings season amid elevated expectations | 🟢 MEDIUM | Could set the tone for global risk appetite into the US afternoon |

| 🇬🇧Thursday | UK Monthly GDP (May) | Consensus looks for a modest 0.1% monthly expansion | 🟢 MEDIUM | Next major UK data point after today’s political and rate-hike focus |

European Session Trade Ideas — 14 July 2026

Eight structured setups — EUR/USD, GBP/USD, Silver, Wheat, FTSE 100, EU 20Y Yield, Ethereum, XRP — with updated prices, levels, and full fundamental and technical analysis

EUR/USD

Fundamental Backdrop

The Euro has clawed back to around 1.1388 as the Dollar corrects lower ahead of today’s US June CPI report, with the Dollar Index easing roughly 0.1% to near 101.17 after Monday’s 0.3% gain. The bounce is being framed by traders as a pre-data adjustment rather than a trend change: the Greenback strengthened Monday after President Trump confirmed the naval blockade on Iranian shipping and reiterated his 20% Hormuz toll claim, and safe-haven Dollar demand could reassert itself quickly if today’s CPI print or Fed Chair Kevin Warsh’s congressional testimony land on the hawkish side. The Euro does have its own hawkish undercurrent: ECB policymaker Yannis Stournaras warned Friday the central bank is “back to square one” in its inflation fight as Gulf-driven fuel costs climb, and markets are now pricing two further ECB hikes over the next year, the first likely in September, which should limit how far the pair can fall on a purely Dollar-driven move.

Technical Outlook

EUR/USD is trading around 1.1388, still capped below the 20-period Exponential Moving Average at 1.1438 after Monday’s bearish flag breakdown, per FXStreet’s technical setup. The Relative Strength Index sits near 39.7, below the neutral 50 line, consistent with lingering downside pressure rather than an oversold extreme. Resistance is layered at 1.1411 (the former channel floor), 1.1438 (the 20-EMA, this trade’s sell-rally zone) and 1.1509 (the channel top), while support sits at the psychological 1.1300 figure (this trade’s target) and the deeper 29 May 2025 low of 1.1210 below that. A confirmed close back above 1.1438 would undercut the bearish setup and open a retest of 1.1509, while a break of the June low near 1.1325 would open the door toward 1.1300 and eventually 1.1210.

Session Catalysts

Watch for: (1) today’s US June CPI report at 12:30 GMT, the session’s single biggest catalyst for Dollar direction; (2) Fed Chair Kevin Warsh’s first congressional testimony before the House Financial Services Committee; (3) any comments from ECB officials, including Isabel Schnabel, on the Governing Council’s 23 July decision; (4) further Hormuz blockade or toll-related headlines given the blockade is due to take effect at 4pm ET today; (5) German 2-year Schatz auction results as a read on eurozone rate-hike pricing.

Trade this pair and 60+ FX crosses on our Zero Account‘s 0.0 Pips Spreads — Open an Account at Capital Street FX.

GBP/USD

Fundamental Backdrop

Sterling is trading around 1.3352, a touch softer on the session, even after former Greater Manchester mayor Andy Burnham secured the backing of the vast majority of Labour MPs to replace Keir Starmer, calming markets’ concerns about a disorderly UK political transition, per FXStreet’s coverage of the leadership change. That domestic political clarity is layering on top of bets for at least one further 25-basis-point Bank of England rate hike by the end of 2026, both genuine tailwinds for the Pound. The offsetting headwind is familiar: escalating US-Iran tensions and Monday’s Hormuz blockade and toll announcement continue to underpin safe-haven Dollar demand, which capped Cable’s rebound to 1.3400 on Monday before it eased back toward the 1.3360s. Today’s docket is light for the UK directly, leaving GBP/USD largely at the mercy of the Dollar side of the pair into this afternoon’s US CPI print and Chair Warsh’s testimony.

Technical Outlook

GBP/USD is holding in the upper half of its recent range near 1.3352, having eased back slightly from the session open, with Bollinger Bands (20,2) still widening modestly and the 14-period Relative Strength Index at 56.4, indicating constructive but not overextended upside momentum. Resistance is aligned with the Bollinger upper band at 1.3470 (this trade’s target), while the Bollinger middle band near 1.3300 provides immediate support and the lower band near 1.3130 would contain a deeper pullback. A confirmed close above 1.3470 would expose the recent multi-week high near 1.3450 and beyond, while a break back below 1.3300 would risk a retest of the lower band and cast doubt on the near-term bullish setup.

Session Catalysts

Watch for: (1) today’s US CPI report and Fed Chair Warsh’s testimony, the dominant Dollar-side catalysts; (2) any further detail on Prime Minister-designate Burnham’s cabinet and fiscal stance, given his team’s pledge to respect Chancellor Rachel Reeves’ existing fiscal rules; (3) Bank of England speakers reiterating the case for further tightening; (4) Thursday’s UK monthly GDP data, already on the market’s radar; (5) broad Dollar positioning tied to Hormuz blockade headlines.

Trade this pair and 60+ FX crosses on our Zero Account‘s 0.0 Pips Spreads — Open an Account at Capital Street FX.

Silver

Fundamental Backdrop

Silver is trading around $58.03 an ounce, compressed inside a symmetrical triangle pattern even as the metal faces its sixth consecutive annual supply deficit, with the Silver Institute pegging the 2026 shortfall at roughly 46.3 million ounces, per FX Leaders’ analysis. Because much of the world’s silver supply is a byproduct of copper, lead and zinc mining, new supply is structurally slow to arrive even when prices rise, a genuine medium-term tailwind. The near-term headwind is macro: a firmer Dollar into today’s CPI print and Fed Chair Warsh’s testimony, plus the prospect the Fed holds rates higher for longer, is weighing on the tape even as industrial demand from solar, EVs, electronics and AI-driven data-center buildout continues to grow. A genuine easing of Gulf tensions could also dampen safe-haven demand for the metal, a further risk to the bullish case.

Technical Outlook

Silver has formed a textbook symmetrical triangle on the 2-hour chart, with the pattern closing in toward its apex, per FX Leaders’ latest technical read. The descending trendline at the top of the range sits near $61 (this trade’s target and the breakout level), while rising support underneath comes in near $55.71 (below this trade’s stop). The 14-period Relative Strength Index at 38.51 is showing a positive divergence against price, with long lower wicks on recent red candles suggesting buyers are absorbing the downside pressure. The triangle’s base projects a measured move of roughly $4 to $5 in whichever direction it eventually resolves, and volume is already thinning as the pattern nears its apex, often a precursor to a decisive move.

Session Catalysts

Watch for: (1) today’s US CPI report and Fed Chair Warsh’s testimony, both key for the Dollar and real-rate backdrop that drives precious metals; (2) any easing or escalation in Hormuz-related headlines that shifts safe-haven demand; (3) a confirmed break of either $61 or $55.71 that would resolve the triangle; (4) ongoing Silver Institute deficit commentary and industrial demand data tied to solar and AI infrastructure buildout; (5) gold’s own price action, given the metals often move in tandem.

Access this and 2000+ Instruments across FX, metals, agriculture, indices, bonds and crypto — Open an Account at Capital Street FX.

Wheat

Fundamental Backdrop

Wheat is trading near 633.97 cents a bushel, up around 0.98% on the day and up around 7.5% over the past month, with Trading Economics data showing the contract up more than 18% year-on-year. The rally has been underpinned by genuinely tighter US supply, after the USDA reported lower-than-expected June 1 wheat stocks of 920 million bushels and trimmed its annual acreage forecast, alongside reports that Russia is restricting export flows through the Don-Azov channel, a route responsible for nearly a quarter of Russia’s wheat shipments. Renewed US strikes on Iran and broader Gulf-driven supply anxiety have added a further geopolitical risk premium. The offsetting headwind is a genuinely strong global harvest picture, with China’s wheat crop rising to 138.95 million metric tons and robust Black Sea-region production continuing to point to ample global availability, which could cap further gains if realized.

Technical Outlook

Wheat has climbed from around 627.8 cents to test levels near 634 cents intraday, consolidating within a broader uptrend that has taken the contract from a nearly six-week low to its current levels. Commitment of Traders data shows managed money trimming its net short position in CBOT wheat by 6,705 contracts in the week to 7 July, while Kansas City wheat managed-money net longs grew by 4,845 contracts, both consistent with fading bearish conviction. Resistance sits at 649.60 (this week’s earlier session high) and 665.00 (this trade’s target), while support lies at 614.00 (the recent six-week high turned support) and 605.00 (this trade’s stop). A confirmed close above 649.60 would open a retest of the 665 zone, while a break below 605 would risk a deeper slide back toward the June range.

Session Catalysts

Watch for: (1) Friday’s USDA WASDE report, a pivotal release for global ending-stocks estimates; (2) further updates on Russian Don-Azov export restrictions and broader Black Sea supply flows; (3) weekly US Export Sales and Inspections data measuring competitiveness against Black Sea origins; (4) any further Hormuz-related escalation that adds a geopolitical risk premium across the grain complex; (5) NOAA’s 8-to-14-day outlook for drier conditions across the Northern Plains.

Access this and 2000+ Instruments across FX, metals, agriculture, indices, bonds and crypto — Open an Account at Capital Street FX.

FTSE 100

Fundamental Backdrop

The FTSE 100 is trading around 10,462.89, down roughly 0.2%-0.4% on the day as a third consecutive night of US strikes on Iran and Monday’s Hormuz blockade and toll announcement push Brent crude above $86 a barrel, denting broad risk appetite across Europe, per Investing.com’s live coverage. Heavyweight energy names including BP and Shell are providing a partial offset as crude approaches four-decade extremes, but that support is not enough to lift the wider index given rising UK Gilt yields and broad risk aversion tied to the Gulf escalation. Germany’s DAX and France’s CAC 40 are seeing sharper declines, underscoring that this is a pan-European move rather than anything UK-specific, while confirmation that Andy Burnham will become the UK’s next Prime Minister has at least removed one source of domestic political uncertainty from the equation.

Technical Outlook

The FTSE 100 has pulled back from Friday’s close near 10,497 to trade around 10,462.89, holding within its recent 10,397-10,747 range over the past month. The index remains inside its broader 52-week uptrend, up over 17% year-on-year, but today’s session shows clear signs of short-term exhaustion as oil-driven inflation concerns weigh on rate-sensitive sectors alongside miners and financials. Resistance sits at 10,540 (this trade’s sell-rally zone, just above today’s early session high) and 10,600 (this trade’s stop, near last week’s highs), while support lies at the psychological 10,400 level and 10,300 (this trade’s target, near the past month’s low). A confirmed close below 10,400 would open a deeper retest of 10,300, while a reclaim of 10,600 would favor a fade back toward the recent range highs.

Session Catalysts

Watch for: (1) today’s US CPI report and Fed Chair Warsh’s testimony, both key drivers of the global rate backdrop that feeds through to UK equities; (2) further Brent crude price action tied to the Hormuz blockade taking effect at 4pm ET; (3) UK Gilt yield moves, which have been surging on rate-hike bets; (4) any fresh detail on Prime Minister-designate Burnham’s policy agenda; (5) US bank earnings from JPMorgan, Wells Fargo and Citigroup, which could set the tone for global risk appetite.

Access this and 2000+ Instruments across FX, metals, agriculture, indices, bonds and crypto — Open an Account at Capital Street FX.

EU 20Y Yield

Fundamental Backdrop

The Euro Area 20-Year government bond yield has climbed to around 3.543%, up sharply from 3.46% just a week ago, as Monday’s 4.4% surge in Brent crude prompted investors to revisit inflation expectations rather than simply seek the defensive qualities of sovereign debt, per Yahoo Finance’s coverage of the move. Normally, geopolitical shocks drive demand for government bonds and push yields lower, but the prospect of sustained higher energy costs is instead keeping yields elevated. Germany’s 10-year Bund yield posted its largest weekly increase in five weeks last week as traders raised bets that the ECB could pause any further policy easing, or even resume tightening, if energy-driven inflation persists — consistent with ECB policymaker Yannis Stournaras’ warning that the central bank is “back to square one” in its inflation fight. Markets are now pricing two further ECB hikes over the coming year, with the first widely expected in September.

Technical Outlook

The 20-Year Euro Area yield has pushed from around 3.46% to 3.543% over the past week, extending a steady climb that has taken the yield up more than 19% over the past year. The move higher has been persistent rather than a single-day spike, consistent with a genuine repricing of the ECB’s rate path rather than a transient risk-off spasm. Resistance for the yield sits at 3.60% (a round-number psychological level) and 3.78% (this trade’s target, near the multi-year highs), while support lies at 3.50% (this trade’s buy-dip zone) and 3.44% (this trade’s stop, near last week’s starting point). A sustained push above 3.60% would confirm the market is pricing a genuine hawkish pivot, while a reversal back below 3.44% would suggest today’s inflation scare is proving transient.

Session Catalysts

Watch for: (1) comments today from ECB Executive Board member Isabel Schnabel on the inflation outlook; (2) today’s Germany 2-year Schatz auction results as a read on near-term demand for eurozone paper; (3) the ECB’s 23 July policy decision, where markets currently lean toward a pause but watch for hawkish repricing; (4) further Brent crude price action tied to the Hormuz blockade; (5) today’s US CPI report and Fed Chair Warsh’s testimony, which set the tone for global yields more broadly.

Access this and 2000+ Instruments across FX, metals, agriculture, indices, bonds and crypto — Open an Account at Capital Street FX.

Ethereum

Fundamental Backdrop

Ethereum is trading around $1,779.87, up modestly on the session and holding up better than several other major tokens against today’s broader Gulf-driven risk-off tone, per Bybit’s live market data. The network continues to benefit from a genuine institutional-adoption tailwind: corporate treasuries including BitMine Immersion now hold over 5.6 million ETH, roughly 4.66% of global supply, while a newly launched independent nonprofit, Ethereum Institutional, is aiming to serve as a neutral point of contact for institutions evaluating ETH-based infrastructure. Exchange reserves have also fallen to record lows as more supply moves into staking and corporate treasuries, a structural tailwind for scarcity. The offsetting headwind is the same one hitting risk assets broadly: a hawkish Fed repricing into today’s CPI report and Chair Warsh’s testimony, plus Gulf-driven macro uncertainty, could pressure crypto risk appetite broadly if the data surprises hawkish.

Technical Outlook

Ethereum is holding a medium-term upward structure, per Bybit’s technical read, with the 14-day RSI near 52.80 signaling neutral-to-constructive momentum. The 20-day EMA sits at $1,718, the 50-day EMA at $1,801 and the 100-day EMA at $1,960, meaning ETH needs to reclaim the 50-day average to strengthen bullish momentum meaningfully. Support lies at $1,740-$1,750 (this trade’s buy-dip zone); a loss of this zone would risk a deeper pullback toward $1,700. Resistance sits at $1,846 (this trade’s target) and the 100-day EMA near $1,960 above that. A confirmed reclaim of the 50-day EMA at $1,801 on a closing basis would open a retest of $1,846 and beyond.

Session Catalysts

Watch for: (1) today’s US CPI report and Fed Chair Warsh’s testimony, key drivers of broad risk appetite across crypto; (2) continued spot Ethereum ETF flow data, which showed a modest net outflow from Fidelity’s FETH in the most recent session; (3) further corporate treasury accumulation announcements; (4) progress on the Glamsterdam upgrade, now targeted for testing on public testnets; (5) broader Bitcoin price action, which continues to set the tone for the wider crypto complex.

Access this and 2000+ Instruments across FX, metals, agriculture, indices, bonds and crypto — Open an Account at Capital Street FX.

XRP

Fundamental Backdrop

XRP has broken below the critical $1.07 Fibonacci support level it had held for 158 consecutive days, trading around $1.043 and down sharply over the past 24 hours, per CryptoNews’ coverage of the move. The decline is being driven by the same broad market downturn hitting risk assets generally: renewed Iran-US hostilities and Monday’s 8-9% surge in oil prices have revived macro inflation fears just as Fed Governor Christopher Waller warned another hot core CPI reading could force policymakers to consider a near-term hike. Long liquidations over the past 24 hours totaled $6.67 million, according to CoinGlass, adding further selling pressure. Compounding matters for XRP specifically, the CLARITY Act’s Senate floor vote has been pushed to late July or early August at the earliest after talks broke down over an ethics provision, removing a potential near-term catalyst.

Technical Outlook

XRP has broken the $1.07 Fibonacci support it held for 158 consecutive days, with that level now acting as overhead resistance and the next support zones at the $1.00 psychological floor and the 18.75% Fibonacci retracement near $0.998. Notably, the weekly Relative Strength Index has entered oversold territory for only the second time in the token’s 12-year history, a rare technical signal that some analysts argue preceded a substantial rally the last time it occurred, though replicating that move today would likely require far greater institutional demand given XRP’s much larger current market capitalization. Resistance sits at $1.09 (this trade’s sell-rally zone, near the broken former support) and $1.13 (this trade’s stop, near last week’s range highs), while a break below $1.00 would open the $0.998 zone (this trade’s target).

Session Catalysts

Watch for: (1) today’s US CPI report and Fed Chair Warsh’s testimony, key for the broad risk backdrop weighing on crypto; (2) any fresh news on the CLARITY Act’s stalled Senate timeline; (3) further whale activity and wallet-creation data, which have shown periodic surges even amid the broader downtrend; (4) whether the $1.00 psychological level holds as a final line of defense; (5) broader Bitcoin and Ethereum price action, given XRP’s high correlation to overall crypto risk sentiment.

Access this and 2000+ Instruments across FX, metals, agriculture, indices, bonds and crypto — Open an Account at Capital Street FX.

European Session FAQ — 14 July 2026

Answers to the questions traders are asking most this session

European Session Summary — Tuesday, 14 July 2026 (Updated Mid-Session)

Tuesday’s European session is defined by the countdown to the 4pm ET deadline for President Trump’s reinstated Hormuz blockade and 20% cargo toll, with Brent crude pushing above $86 a barrel, its highest level since mid-June and up more than 10% on the week, per live Reuters, Bloomberg, Investing.com and FXStreet coverage. European equities are reflecting the unease, with the FTSE 100 easing to around 10,462.89 and Germany’s DAX and France’s CAC 40 posting sharper declines, even as energy heavyweights including BP and Shell offer a partial offset from higher crude prices. Fixed income markets are showing a textbook inflation-driven reaction to the Gulf shock rather than a traditional safe-haven bid, with the Euro Area 20-Year bond yield surging to around 3.543%, up from 3.46% a week ago, as ECB policymaker Yannis Stournaras’ warning that the central bank is “back to square one” on inflation gains further traction and markets price two further ECB hikes over the coming year. In currencies, EUR/USD has rebounded to around 1.1388 as the Dollar corrects lower ahead of today’s US CPI report, though the pair remains technically capped below its 20-period moving average, while GBP/USD has found genuine support near 1.3352 after Andy Burnham’s confirmation as the UK’s next Prime Minister calmed concerns about a disorderly political transition. In commodities, Silver has compressed to around $58.03 an ounce inside a tightening symmetrical triangle even as the metal faces a sixth consecutive annual supply deficit, while Wheat has extended its monthly climb to around 633.97 cents a bushel on tighter US stocks and reports of Russian export restrictions through the Don-Azov channel. In digital assets, Ethereum is holding a constructive uptrend near $1,779.87 while XRP has broken below the $1.07 Fibonacci support it defended for 158 consecutive days, now trading around $1.043 amid a rare weekly-oversold RSI reading. Highest-conviction session idea: fade EUR/USD’s pre-CPI bounce by selling rallies toward 1.1440, targeting 1.1300 — the pair’s technical structure remains bearish below its 20-EMA, and a hawkish surprise from either today’s CPI print or Fed Chair Warsh’s testimony could quickly restore the safe-haven Dollar bid that dominated Monday’s session, though a genuinely soft CPI print or dovish Warsh tone remains a real risk that could instead extend the pair’s current corrective bounce.

For the individual instruments: EUR/USD sell rallies toward 1.1440, stop 1.1485, target 1.1300 — the pair’s bearish flag structure below the 20-EMA and hawkish ECB repricing are offsetting factors, though a genuine near-term catalyst is today’s CPI print and Warsh testimony, both of which could quickly restore broad Dollar demand. GBP/USD buy dips toward 1.3320, stop 1.3270, target 1.3470 — Burnham’s confirmation as PM and BoE rate-hike bets are genuine tailwinds, though broad Gulf-driven Dollar demand remains a real headwind to sustained Sterling strength. Silver buy dips toward $56.20, stop $54.90, target $61.00 — a genuine sixth consecutive annual supply deficit is a structural tailwind, though a firmer Dollar into today’s data is a real near-term headwind that could resolve the triangle to the downside instead. Wheat buy dips toward 620.00¢, stop 605.00¢, target 665.00¢ — tighter US stocks and Russian export restrictions are genuine tailwinds, though a strong global harvest picture, including China’s, is a real headwind to further gains. FTSE 100 sell rallies toward 10,540, stop 10,600, target 10,300 — broad oil-driven risk-off and rising Gilt yields are genuine tailwinds to further downside, though strength in energy heavyweights like BP and Shell is a real headwind to a sustained move lower. EU 20Y Yield buy dips toward 3.52%, stop 3.44%, target 3.78% — oil-driven inflation repricing and hawkish ECB commentary are genuine tailwinds to further yield increases, though a swift Hormuz de-escalation is a real risk that could quickly reverse the move. Ethereum buy dips toward $1,750, stop $1,715, target $1,846 — continued institutional accumulation and record-low exchange reserves are genuine tailwinds, though a broad risk-off reaction to today’s CPI or Warsh testimony is a real risk to further upside. XRP sell rallies toward $1.09, stop $1.13, target $1.00 — the break of a 158-day Fibonacci support and a stalled CLARITY Act are genuine tailwinds to further downside, though a rare weekly-oversold RSI reading is a real risk of a near-term technical bounce. The decisive variables for the remainder of the session are today’s US CPI report, Fed Chair Warsh’s testimony, the 4pm ET Hormuz blockade deadline, and the German Schatz auction and any further ECB commentary. Size positions accordingly, and note that the geopolitical backdrop remains exceptionally fluid and carries genuine event risk that could reshape sentiment sharply intraday.

Ready to act on today’s setups? Open an Account with Capital Street FX and trade every instrument covered in this report on our Zero Account‘s 0.0 Pips Spreads and 1:10000 Leverage, across 2000+ Instruments, with a welcome deposit bonus and 24/7 Live Support on hand for every session.

Not sure which account fits your style? Compare our Account Types side by side with our Account Comparison tool, browse current Promotions / Bonus offers, and trade from our Trading Platform suite. Funding is simple via our Deposit & Withdrawal options. For ongoing coverage, explore our Forex Analysis Pages, Commodity Analysis Pages and Crypto Analysis Pages, plus our Daily Market Analysis and Weekly Market Analysis reports and the full Economic Calendar. New to trading? Visit our Trading Education / Blog, or reach our Contact Us / Live Support team any time.

Access Live European Markets →