The Currency That Rules the World Is Changing — A 2,600-Year Story of Monetary Power, Imperial Cycles & Market Impact | Capital Street FX

Capital Street FX Research Desk · Geopolitical & Monetary Intelligence · Q1 2026

The Longest

Battle

in Human

History

For 2,600 Years, Empires Have Fought Over the Right to Issue the World’s Money. Athens, Rome, Byzantium, Spain, Britain — Each Rose. Each Fell. In Q1 2026, the Next Chapter Is Already Being Written.

USD Reserve: 56.3%·

Gold: $5,023·

DXY: –12.5% in 2025·

Yuan FX: 8.5%·

SCO Local Currency: 97%·

Dollar Age: 81 yrs vs 94yr avg

Athens had it. Rome had it. Byzantium kept it for 700 years. Spain seized it with New World silver and bled it dry through imperial war. Britain carried it into two world wars and handed the crown to America in 1944. In Q1 2026, Iran has declared that no vessel will pass the Strait of Hormuz without trading in yuan. Russia has told its partners that dollar transactions are finished. India and China are settling energy, grain, and manufactured goods in their own currencies — quietly, bilaterally, systematically — building the architecture of a world that no longer needs the dollar to function. The battle that has shaped every civilisation for 2,600 years is not approaching. It has arrived.

At the close of the first quarter of 2026, the geopolitical and financial landscape carries a weight that has not been felt since the years immediately following the Second World War — when the world’s monetary order was being recast from scratch at a New Hampshire hotel. Iran has positioned its naval forces at the Strait of Hormuz and declared preferential passage for yuan-paying vessels, applying direct physical leverage to the world’s most critical oil chokepoint. Russia has formally moved away from dollar settlement across its trade corridors, telling partners from Beijing to New Delhi that the era of dollar-denominated transactions is over for those within its economic sphere. India and China — the world’s third and first largest economies by purchasing power — are conducting energy trades, commodity exchanges, and bilateral finance in rupees and yuan, bypassing SWIFT and the dollar-clearing infrastructure that has underpinned global commerce since 1944. Central banks have bought gold at a pace unseen since the 1950s for three consecutive years. The dollar’s share of global reserves has reached its lowest level in three decades. These are not isolated tremors. They are the simultaneous eruption of forces that have been building beneath the surface of the global financial system for the better part of a generation — and together, they constitute the most serious challenge to dollar monetary supremacy in eighty years.

Q2 2025 · 30-yr Low

Worst Yr in 20 Yrs

ATH $5,595 · Jan 2026

Sep 2025 · All-time High

In Local Currencies 2025

Settled in RMB 2025

March 2025

Lifespan · Dollar: 81 yrs

The War That Never Ends: 2,600 Years of Empires Fighting for the Right to Issue the World’s Money

Every great empire in history has grasped, at some level, that military conquest is expensive and impermanent. The deeper, more durable form of power — the kind that extracts wealth from every corner of the world without firing a shot — is monetary. The nation whose currency the world is compelled to use does not need to occupy territories. It occupies balance sheets. It does not need to tax its rivals directly. It taxes them through seigniorage, through the pricing power of the reserve currency, through the quiet right to make its own fiscal excess the rest of the world’s problem. This is the contest that has been fought, in different forms and under different flags, across every major civilisation since Athens first discovered that its silver coins were being accepted from Egypt to Persia without question. It is the longest and least understood war in recorded history.

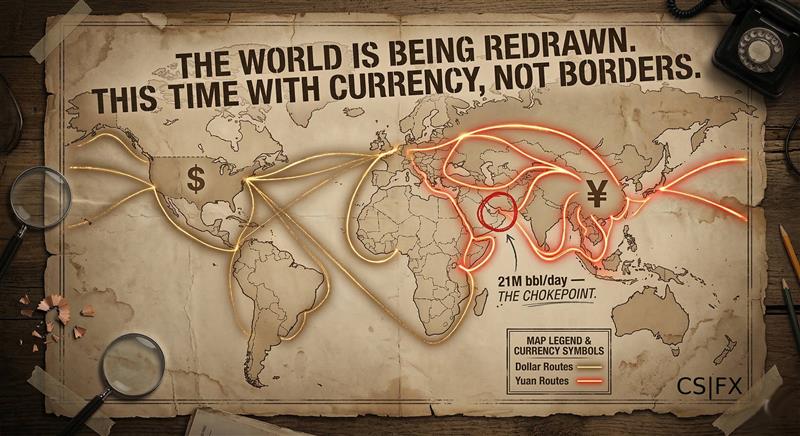

In the first quarter of 2026, that war has entered a new and consequential phase. Iran has positioned its naval forces at the Strait of Hormuz — through which approximately 21 million barrels of oil move daily, representing roughly one-fifth of the world’s entire consumption — and declared that passage will be preferred for vessels trading in yuan rather than dollars. The announcement is not, at its core, a military threat. It is a monetary one. It is the assertion that physical control over the world’s most critical energy corridor can be converted into financial leverage over the currency that has priced that energy for the past half-century. Russia has formally abandoned dollar settlement across its trade corridors, directing partners from Beijing to New Delhi to transact in rubles, yuan, and local currencies. The directive is already largely operational: Russia-China trade, which a decade ago was 90% dollar-denominated, is now 90% non-dollar. India and China — between them the largest and third-largest economies on Earth by purchasing power — are conducting energy purchases, grain trades, and manufactured goods exchanges in rupees and yuan, building bilateral settlement systems that bypass the SWIFT infrastructure entirely. The Shanghai Cooperation Organisation, a bloc of ten nations including Russia, China, India, Pakistan, Iran, and Kazakhstan, conducted 97% of its internal trade in local currencies in the past year. Not 97% with the dollar as a secondary option. Without the dollar at all.

These events are not happening in isolation. They are the visible surface of a structural shift that has been building across two decades of quiet, deliberate construction. China has spent twenty years erecting a parallel monetary architecture — its own cross-border payment system that now connects 1,467 institutions across 119 countries, its own yuan-denominated oil futures exchange in Shanghai, bilateral currency swap agreements with over thirty central banks, a digital yuan tested in cross-border pilots with the UAE and Hong Kong. Russia, after the freezing of $300 billion in its central bank reserves by the West in February 2022 — an act that demonstrated with brutal clarity that dollar reserves are not assets but permissions — has redesigned its entire financial operating system around the assumption that dollar access is a weapon that can be turned against any nation at any time. And the lesson of 2022 was not lost on the others. Gold purchases by central banks have exceeded 1,000 tonnes annually for three consecutive years — the highest sustained pace since the 1950s. Gold cannot be frozen. Gold cannot be sanctioned. Gold holds no counterparty risk. The global rush toward bullion is not a bet on inflation. It is a vote of no-confidence in the paper reserve system that the United States has managed since 1944.

The United States dollar’s share of global foreign exchange reserves now stands at 56.3% — its lowest level in thirty years, down from 71.5% at the turn of the century. The dollar index fell 12.5% across 2025 — its worst annual performance in more than two decades. Gold reached its all-time high of $5,595 per ounce in January 2026. These are not market fluctuations. They are the measurable, data-confirmed signals of a system in transition. And the system in question — the dollar-centred global monetary order codified at Bretton Woods in 1944 — sits today where every preceding reserve currency system has eventually sat: under challenge from a rising coalition of nations who have concluded that the costs of the incumbent’s privilege outweigh the benefits of its stability.

The historical record of these transitions is unambiguous in its patterns, even when it is ambiguous about its timings. Athens rose to monetary dominance through the purity of its silver and the reach of its navy. Rome built a monetary system of extraordinary sophistication and then destroyed it through a century of fiscal debasement — the silver content of its denarius falling from 95% to 2%, triggering an inflation crisis that contemporary accounts describe as 1,000% price rises within three decades. The Byzantine Empire maintained gold monetary discipline with a rigour that no subsequent system has matched — and held reserve currency status for 700 consecutive years as a direct result. Spain flooded the world with New World silver and triggered the first global inflation crisis — the sixteenth-century Price Revolution that drove European prices up 500% over 150 years and ultimately dissolved the monetary hegemony that the silver had built. Britain financed the global industrial revolution on sterling’s reserve status, ran up debts in two world wars it could not afford, and watched its currency fall from $4.86 to $1.03 over the following eight decades. The pattern in every case is the same: power enables privilege, privilege enables excess, excess erodes credibility, and eroded credibility creates the conditions for the next challenger to step forward.

The United States is 82 years into a reserve currency era whose historical average has lasted 94 years. It carries a national debt of $36.2 trillion. Its fiscal deficit runs above 6% of GDP. Its current account has been in deficit for four decades. It has weaponised dollar access through sanctions to the point where the sanction tool has become, paradoxically, the greatest accelerant of the movement to render it obsolete. Iran’s Hormuz announcement, Russia’s dollar rejection, India’s rupee settlement network, China’s yuan infrastructure — these are not spontaneous developments. They are the coordinated, if not always coordinated between themselves, responses of nations that have drawn a shared conclusion: in a world where the reserve currency can be deployed as a weapon against any of them at any moment, the reserve currency is a liability as much as it is a convenience. The architecture being built to replace it — imperfect, incomplete, fragmented — is not a single challenger. It is a system of alternatives designed to reduce the points of failure. And it is further advanced, in Q1 2026, than almost any mainstream financial analysis has yet acknowledged.

Iran · The Hormuz Lever: Naval forces positioned at the 39-kilometre strait carrying 21 million barrels per day. Yuan-denominated vessels declared preferred. The first time in history a physical energy chokepoint has been used as monetary leverage. UBS models $150/bbl oil under sustained disruption.

Russia · The Dollar Rejection: Formal directive to abandon dollar settlement across all major trade corridors. Russia-China trade: 90%+ non-dollar. Russia-Iran: 95%+ rubles and rials. Russia-India: rupee-ruble with UAE dirham as bridge. The operational dollar exodus is a fact, not a policy aspiration.

China · The Parallel Architecture: CIPS payment system operating in 119 countries. Shanghai INE pricing crude in yuan. e-CNY tested across borders. 54% of China’s own cross-border transactions in RMB — up from zero in 2010. The infrastructure for a yuan-based trade system is built, tested, and in daily use.

India · The Bilateral Settlement Network: Rupee Vostro accounts in 26 countries. Local Currency Settlement Agreements with UAE, Malaysia, Maldives, Indonesia, and others. First crude oil purchase in rupees completed with ADNOC in August 2023. The world’s most populous nation is systematically reducing its dollar dependency through bilateral treaties rather than confrontation.

BRICS+ · The Coalition: Eleven full members representing 37% of world GDP by purchasing power. Saudi Arabia formally joined in 2025. Indonesia joined in January 2025. Over 40 nations have applied for membership. 97% of SCO intra-bloc trade in local currencies. The coalition is no longer an aspiration. It is an operating economic bloc.

Central Banks · The Gold Signal: 1,000+ tonnes purchased annually for three consecutive years. Gold’s share of global reserves more than doubled since 2015, from below 10% to over 23%. The Bank of Poland, the People’s Bank of China, the Reserve Bank of India, the central banks of Turkey and Kazakhstan — all systematically accumulating. The signal is not ambiguous.

The EV Transition · The Structural Threat: One in four cars sold globally in 2026 is electric. By 2030, analysts project one in three. Global oil demand is expected to peak and begin declining within this decade. The petrodollar system — the mechanism that replaced gold convertibility in 1974 and has sustained dollar structural demand for 51 years — depends on the world buying oil in dollars. As oil’s primacy fades, so does that mechanism’s grip.

The events of Q1 2026 are not unprecedented. They are, in structural terms, nearly identical to the period between 1920 and 1944 — when the British pound was losing reserve status and the US dollar was building the institutional depth to replace it. The British pound’s decline was gradual: devalued in 1949, again in 1967, bailed out by the IMF in 1976, near-parity in 1985, all-time low in 2022. The entire transition from formal reserve currency supremacy to ordinary floating status took thirty years. The lesson is not that reserve currency transitions happen quickly. It is that, by the time they are undeniable, they are already well advanced. Gold in sterling terms rose 22,000% across the period of British reserve decline. That is the template. The question for every market participant in 2026 is not whether the transition is happening. It is where, in that arc, the current moment falls.

What You Get When Your Currency Rules the World — and What You Lose When It Stops

Reserve currency status is not simply a financial designation. It is the most powerful economic privilege in recorded human history — conferring rights and advantages that no military conquest, trade agreement, or diplomatic treaty can match. French Finance Minister Valéry Giscard d’Estaing called it exorbitant privilege in 1965, and he was right.

When a country’s currency becomes the world’s reserve currency, it gains something extraordinary: the right to print the very medium of exchange through which the entire planet conducts its most important business. When a Brazilian company buys Saudi oil, the transaction clears in dollars — regardless of whether a single American is involved. When Indonesia issues international bonds, they are denominated in dollars. When the IMF bails out Argentina, it lends in dollars. The reserve currency nation did not build that system through superior virtue. It built it through superior power — and maintains it through superior institutional depth, liquidity, and the shadow of financial sanctions.

interest rates · permanently

without currency crisis

in your own currency

free from the world

nation’s wealth overnight

world funds your deficits

without firing a single shot

every global financial market

The seigniorage benefit alone is staggering in scale. Because foreign central banks, corporations, and individuals need to hold dollars, the United States effectively receives an interest-free loan from the entire world of approximately $6.5 trillion. The annual seigniorage benefit — the difference between what the US pays to issue currency and what it earns from foreign holdings — ranges from $40 billion to $100 billion per year. Over 81 years since Bretton Woods, this accumulates to a figure measured in multiple trillions of dollars.

The geopolitical weapon is even more consequential. In February 2022, when Russia invaded Ukraine, the West froze $300 billion in Russian central bank reserves with a phone call. Not a single missile was fired. The money simply ceased to be accessible. This single demonstration — that the United States can effectively confiscate any nation’s dollar-denominated wealth — has driven more de-dollarisation in three years than the previous three decades combined. Every central bank in the world that is not fully aligned with Washington now asks the same question: are our dollar reserves safe?

Russia held approximately $630 billion in foreign exchange reserves before the invasion. The West froze approximately $300 billion — nearly half — within days. The lesson was heard in Beijing, Riyadh, New Delhi, Ankara, and Jakarta simultaneously. Dollar reserves are not safe if Washington decides they are a geopolitical target. Foreign ownership of US Treasuries has fallen from above 50% during the GFC to approximately 30% in early 2025 — the lowest in decades.

US President Trump explicitly warned that any attempt by BRICS to bypass the dollar would result in 100% tariffs on BRICS exports to the US. This threat of economic retaliation deters rapid de-dollarisation — but paradoxically, the use of the dollar as a coercive tool accelerates the search for alternatives among nations fearing future targeting.

From Athenian Silver to the Petrodollar: Every Reserve Currency, Every Collapse, Every Pattern

No reserve currency has lasted forever. The average reign across 2,600 years of monetary history is approximately 94 years in the modern era. The US dollar has held reserve status for 81 years. Every predecessor was once considered unassailable. Every one fell.

| Currency | Era | Duration | Backing | Peak Reach | How It Ended | Forex Impact at Collapse | Commodity Impact |

|---|---|---|---|---|---|---|---|

| Athenian Drachma | ~600–300 BC | ~200 yrs | Laurion silver | Mediterranean + Near East | Macedonian military conquest | Regional trade disruption, prices +30–40% | Silver repriced across Aegean |

| Roman Denarius | 211 BC–301 AD | ~400 yrs | Silver: 95%→2% debased | Europe, N.Africa, Near East, India | Hyperinflationary collapse | 1,000% inflation 268–301 AD | Grain prices collapsed system-wide |

| Byzantine Solidus ★ | 301–1453 AD | ~700 yrs · LONGEST | 24-carat gold (strict) | Global medieval trade | Military defeats + debasement post-1071 | Ottoman conquest reset global gold price | Gold repriced across Europe-Asia |

| Islamic Dinar | 700–1258 AD | ~500 yrs | Pure gold | Islamic world + Africa + India | Mongol sack of Baghdad 1258 | Trade routes collapsed; silk road repriced | Gold and spice markets disrupted |

| Florentine Florin | 1252–1533 | ~280 yrs | 24k gold · never debased | ~50% European trade finance | Black Death; Italian city wars | Italian banking collapse; 1340s credit freeze | Wool and spice prices volatile |

| Spanish Real (Piece of 8) | 1535–1820s | ~280 yrs | New World silver | First truly global currency | Imperial overextension; debasement | European Price Revolution: +500% over 150 yrs | Silver flood → global inflation |

| Dutch Guilder | ~1600–1720 | ~100 yrs | Amsterdam Bank gold | ~50% European trade | Anglo-Dutch Wars; VOC decline | GBP strengthened; Amsterdam Bank failed 1819 | Spice and grain markets repriced |

| British Pound Sterling | 1815–1944 | ~130 yrs | Gold standard | 60% of global trade invoiced | Two World Wars; US gold dominance | GBP: $4.86→$1.03 (–79%) over 80 yrs | Gold in GBP +22,400%; commodity repricing |

| US Dollar | 1944–now | 81 yrs · ongoing | Gold (1944–71) → Petrodollar → Debt | 56.3% of global reserves (Q2 2025) | Approaching average; first serious challenge | DXY –12.5% in 2025 · Gold ATH | Gold $5,023; Brent $82; all commodities elevated |

The Pattern That Killed Every Reserve Currency — And Why the Dollar Is Showing the Same Signs

How a 1974 Deal With Saudi Arabia Kept the Dollar King After Nixon Ended Gold — And Why It’s Cracking Now

On August 15, 1971, President Nixon announced on national television that the US would no longer exchange dollars for gold. The Bretton Woods system collapsed. The dollar should have lost its reserve status. Instead, Henry Kissinger flew to Riyadh and created the most consequential monetary architecture since Bretton Woods: the petrodollar.

The petrodollar agreement — formalised in 1974 between the US and Saudi Arabia — was brutally elegant. Saudi Arabia would price all oil exports in US dollars. OPEC would follow. In exchange, the US would provide Saudi Arabia with military protection, weapons systems, and political guarantees. Saudi petrodollar surpluses would be “recycled” into US Treasury bonds, funding American deficits at artificially low rates. The result: every oil-importing nation on Earth needed dollars to buy energy. The structural demand for dollars was guaranteed not by gold, but by the physical necessity of petroleum.

This system worked with extraordinary stability for 48 years. It allowed the US to run persistent current account deficits — the world needed to accumulate dollars to buy oil, so dollars flowed back to America in exchange for goods and services. It funded US military supremacy. It kept US Treasury yields suppressed. It gave the United States a financial weapon of enormous precision: deny dollar access, and you deny the ability to buy energy.

One in four cars sold globally in 2025 will be electric. By 2030, the ratio is expected to reach two in five. Global oil demand is projected to stagnate after 2026 and potentially decline by 2030 as EV adoption accelerates. China sold 11 million EVs in 2024 alone and produces over 70% of global EV manufacturing capacity. As transportation electrifies, the structural demand for oil — and therefore for dollars — diminishes. This is the long-term structural threat to the petrodollar that no army can defend against. Unlike geopolitical challenges, the EV transition is irreversible.

30+ Nations Are Abandoning the Dollar in 2025 — The Complete Country-by-Country Record

This is not a theoretical future scenario. The de-dollarisation is happening now, in dozens of countries simultaneously, at a pace that has never been seen before. Here is the complete data.

◆ Sources: IMF COFER Q2 2025 (Oct 2025), Federal Reserve International Role of the USD 2025 Edition (Jul 2025), BestBrokers Nov 2025. Note: Dollar’s measured decline in 2025 partly reflects DXY weakness (–12.5%) inflating non-USD reserve values. Exchange-rate-adjusted active selling is smaller but still structurally significant per IMF analysis.

The Country-by-Country De-Dollarisation Map

The scale of countries reducing dollar dependency in 2025 is unprecedented. This is not confined to adversaries of the United States. It is a global movement driven by economic logic — reducing transaction costs, avoiding sanctions exposure, and building monetary sovereignty.

In 2025, more than 54% of China’s cross-border transactions were settled in RMB — up from approximately 15% in January 2017, and from close to zero in 2010. China is the world’s largest trading nation. Achieving majority-RMB settlement for its own trade is equivalent to creating a parallel global monetary system through the back door. The CIPS payment network had 1,467 indirect participants across 119 countries by early 2025, processing ¥9.6 trillion in daily average volume — a 65%+ year-over-year growth rate from 2022.

Iran’s Strait of Hormuz Announcement: 21 Million Barrels a Day as a Financial Weapon

When Iran announced that vessels conducting oil trade in yuan would receive preferential Hormuz passage treatment, it did something that no previous de-dollarisation effort had achieved: it connected a physical commodity chokepoint to a financial incentive to abandon the dollar. The implications for oil, gold, and forex markets are structural.

through Hormuz

at stake

transiting

if disrupted

via Hormuz

already in yuan

What Reserve Currency Erosion Does to Every Asset Class — Historical Evidence & Live Projections

The reserve currency story is not abstract geopolitics — it is the most important macro driver in global markets right now. In 2025, every major asset class is already reflecting the early stages of this transition. Here is what history and current data say about where each asset goes next.

Gold — The Primary Beneficiary: Bank Forecasts 2026–2030

Gold is the unambiguous winner of reserve currency fragmentation. The mechanism: as the dollar loses share as the global reserve asset, central banks need an alternative that carries zero geopolitical counterparty risk. You cannot freeze physical gold held in your own vaults. Gold’s share of reserve assets has more than doubled from below 10% in 2015 to over 23% in 2025. Central banks bought over 1,000 tonnes annually for three consecutive years — the highest sustained pace since the 1950s. 95% of central banks surveyed by the World Gold Council intend to increase gold reserves in 2026.

◆ Sources: JPMorgan raised gold target to $6,300 by end-2026 on Feb 2, 2026; Wells Fargo lifted to $6,100–$6,300; Goldman Sachs: $5,000 for 2026/2027; RBC Capital Markets: $4,600 avg 2026, $5,100 in 2027; InvestingHaven structural bull case: $5,750 (2026), $6,500 (2027), $8,150 (2030). Current price: $5,023 (March 17, 2026).

DXY Dollar Index — Structural Weakening Ahead

The DXY has already delivered its worst annual performance in over two decades in 2025 (–12.5%). The structural case for further dollar weakness rests on four pillars: (1) declining global reserve demand reducing the captive buyer base for dollar assets; (2) Fed rate cuts narrowing the interest rate differential advantage; (3) EV transition gradually dismantling the petrodollar’s oil-demand mechanism; and (4) the $36.2 trillion US national debt eventually forcing a fiscal reckoning. Against this, the dollar’s bull case rests on its unmatched liquidity, institutional depth, and the absence of a ready replacement.

◆ Source: Forex.com Year-End 2025 Review (Dec 24, 2025). Gold data: LiteFinance Dec 2025. Yuan data: Atlas Institute Sep 2025.

Bull Case, Base Case, Bear Case: What the World Looks Like in Each

The next decade will determine whether the dollar’s reserve status erosion is gradual and manageable, or sudden and destabilising. Three scenarios cover the realistic range of outcomes — each with distinct asset price implications.

Six Market Positions for the Reserve Currency Transition Era — Full Entry, Stop, Target, Thesis

The reserve currency transition is already a live market driver. The trades below are structured around the multi-year directional thesis, with levels based on current March 2025/2026 prices. Not financial advice — educational trade framework only.

Frequently Asked Questions on Reserve Currencies & Markets

The Dollar at 81: Not Dying — But Sharing

The US dollar is not dying. The dominance of the US dollar in global foreign exchange reserves remains clear — 56.32% is still a dominant share. The dollar accounts for 50% of international payments on SWIFT, 88% of all FX transactions by volume, 70% of international foreign currency debt issuance, and 48% of cross-border liabilities. These are not the numbers of a currency in crisis. They are the numbers of the world’s most deeply embedded monetary institution, with network effects accumulated over 81 years of structural integration.

But the direction is unambiguous. The 26-year decline from 71.5% (1999) to 56.3% (2025) is not a measurement error. The SCO conducting 97% of trade in local currencies is not a rounding error. China settling 54% of cross-border transactions in yuan — up from zero in 2010 — is not a coincidence. Central banks buying over 1,000 tonnes of gold per year for three consecutive years is not a temporary aberration. Iran’s Hormuz announcement is not a geopolitical bluff. These are the early, measurable signals of a structural transition that every previous reserve currency in history has undergone.

The CSFX investment conclusion is clear: gold is the structural trade of this decade. JPMorgan raised its 2026 target to $6,300/oz. Wells Fargo sees $6,100–$6,300. The structural bull case reaches $8,150 by 2030 under InvestingHaven’s model. Every central bank that is nervous about dollar reserves — Western or non-Western — is buying gold, because physical gold in your own vaults cannot be frozen. The DXY is in a structural weakening trend that may have years to run. The EUR/USD recovery from post-2022 lows has the fundamental support of reserve diversification behind it.

The transition, when it comes fully, will be measured in decades — not years. The British pound took 30 years to transition from reserve currency dominance to ordinary floating status, and another 46 years to reach its all-time low. The US dollar will not collapse overnight. But every investor and every trader operating in currency markets for the next decade will be operating in the shadow of this transition — and the price signals are already, clearly, pointing in one direction.

“The reserve currency does not change overnight. It changes the way tides change — imperceptibly at first, then with a force that rearranges everything. The tide turned in 2022. The smart money knows which direction to face.”

— Capital Street FX Research Desk · March 17, 2025 · capitalstreetfx.com · For educational purposes only · Not financial advice

⚠ RISK DISCLAIMER: Trading foreign exchange, commodities, and derivative instruments involves substantial risk of loss and is not suitable for all investors. Leverage can work against you as well as for you. Past performance is not indicative of future results. The information contained in this article is for educational and informational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instrument. Capital Street FX (capitalstreetfx.com) does not provide personalised investment advice. All trade setups, forecasts, and projections are illustrative examples for educational purposes only. You should seek independent financial advice before making any investment decisions. CFD trading is restricted in certain jurisdictions. Please ensure you fully understand the risks involved.

Sources used in this article: IMF COFER Q2 2025 (October 2025); Federal Reserve International Role of the US Dollar 2025 Edition (July 18, 2025); JPMorgan Global Research Gold Forecasts (February 2026); Goldman Sachs Commodity Research; Wells Fargo Investment Institute; RBC Capital Markets; Atlas Institute for International Affairs (September 2025); Chicago Policy Review (October 2025); EBC Financial Group De-Dollarisation Report (October 2025); BestBrokers Reserve Currency 2025 (November 2025); Wikipedia De-dollarisation (March 2026); Diplomatist BRICS Analysis (May 2025); LiteFinance Gold Price Analysis; InvestingHaven Gold Forecast (February 2026); Forex.com Year-End 2025 Review; Investing.com DXY Analysis; Scottsdale Bullion & Coin Bank Forecasts; Carnegie Endowment for International Peace (December 2025).

© 2025 Capital Street FX · All Rights Reserved · capitalstreetfx.com · Regulated by FSC Mauritius C112010690 and FSA Saint Vincent 22064-IBC-2014