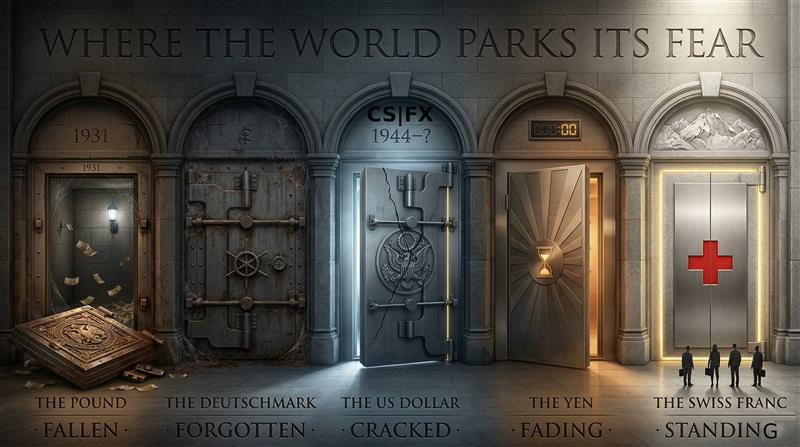

Safe Haven Currencies: The Complete History | The Capital Dispatch

Safe Haven Currencies:

5,000 Years of History,

the Present Crisis,

and the Next Five Years

For five thousand years, every civilisation that ever rose asked the same question: when the armies arrive, when the harvest fails, when the empire starts to crack — what do you hold that will still be worth something tomorrow? The Mesopotamian merchant answered with silver. The Byzantine emperor answered with a gold coin so trusted it circulated unchanged for seven centuries. The Florentine banker answered with the florin. The Spanish crown answered with a mountain of Bolivian silver. The British Empire answered with sterling. Each answer worked. Each was eventually replaced — not by conquest alone, but because the trust that made it work had quietly worn through. This is the story of all twelve answers, the pattern that connects them across five millennia, and what that pattern tells us about the one playing out right now.

Before there were banks, before there were coins, before there was even a word for money, there was fear. A farmer in the Tigris valley in 3000 BCE understood something about the world that no school could teach him: what he held today might be worthless tomorrow. The harvest could fail. The river could flood. A king could march through and take everything. And so humanity began its oldest and most restless search — not for wealth, but for a form of wealth that survived. Something a stranger would accept without knowing your name. Something that could be carried across a border, buried under a floor, sewn into a cloak. Something that held its value when everything around it was collapsing. The search for that thing is the oldest continuous project in civilisation. It has never stopped. It is still underway today.

Silver answered first. You could weigh it. You could divide it. It did not rot, did not die, did not answer to any king’s decree. When the Lydians struck the first true coins around 700 BCE, they turned that ancient instinct into architecture — and the world has been building on that architecture ever since. The Byzantine solidus carried the same 4.5 grams of pure gold for seven hundred years, financing trade from the Baltic to the Indian Ocean because every merchant from a Norse chieftain to an Arab silk trader knew, without testing it, that the coin would not lie. The Florentine florin filled the void when Constantinople’s emperors finally got greedy and debased what seven centuries had built. Spain’s Piece of Eight became the first currency accepted on every continent, not because Madrid commanded it, but because the silver content could be verified anywhere on earth with a simple scale — a promise written in metal rather than in a government’s word. The Dutch guilder proved that paper, backed by a sufficiently disciplined institution, could carry the same trust as gold. Sterling underwrote a century of world commerce on the credibility of the Bank of England and the reach of the Royal Navy. Each answer worked, for a time. Each was eventually replaced. Not by conquest alone, but because the trust that made it work had quietly worn through.

The pattern, once you see it, is impossible to unsee. Safe haven status is never declared — it is earned, grain by grain, crisis by crisis, over decades or centuries of never breaking the promise. And it is never lost in a single catastrophe. It drains away through compounding moments of weakness: a coin shaved a little thinner, a peg held at the wrong rate out of pride, a deficit allowed to grow because the consequences feel distant, a power wielded once too often until the world learns it can be wielded against them. The solidus lasted 700 years, then fell in a generation. The florin lasted 280. The Piece of Eight lasted 300 — long after the Spanish empire that minted it had faded to a shadow. Sterling lasted 115 years as the world’s reserve currency, then surrendered the throne at a hotel in New Hampshire in 1944, when a dying British economist named Keynes wept as the American delegation — holding two-thirds of the world’s gold — installed the dollar in its place.

The dollar has held that throne for 82 years. It is the shortest reign of any reserve currency in the modern era. And on a single day in April 2025, for the first time in those 82 years, it did something no reserve currency had ever done in a crisis of its own making: it fell. Stocks fell. Bonds fell. The dollar fell. All at once. The rule that had held since Bretton Woods — that fear drives capital toward the dollar, always — broke. And what history teaches, with brutal consistency, is that rules broken once are never quite unbreakable again.

This is the complete account of those five thousand years. Every currency that earned the world’s trust. Every crisis that tested it. Every failure, every succession, every structural shift — from Mesopotamian silver to Swiss francs, from Byzantine gold to Liberation Day 2025. It is not a survey of exchange rates. It is the story of how civilisation has organised its fear, age by age — and what that ancient, unbroken pattern tells us about where the world’s frightened money is going next.

Safe Haven 2026

Dominated Global Trade

Worst Since 1973

Share · Down from 71%

ATH $5,589 (Jan ’26)

Reserve Currency

Safe Haven Winner

Picture a merchant in Constantinople in 527 AD, sewing gold coins into the lining of his cloak as barbarian armies approach. Picture a Jewish banker in 1938 Vienna, converting reichsmarks to Swiss francs as the Anschluss unfolds. Picture a Chinese billionaire in 2025, watching the dollar fall on Liberation Day and reaching for something — anything — that might hold its value when the world’s reserve currency cannot. The question they all asked is the same question every generation asks when fear arrives: where does money go to survive? The answer has changed twelve times in five thousand years. This is the story of each answer, why it worked, why it eventually stopped working, and what the current answer is becoming.

Every empire that ever rose faced the same terrifying question at the moment of crisis: when the armies are at the gates, when the plague ships arrive, when the treasury is empty and the king is desperate — what do you hold that will still be worth something tomorrow? The Mesopotamian merchants figured it out first: silver, because you could weigh it anywhere and it didn’t rot. The Romans improved on it: gold coins stamped with the emperor’s face, accepted from Britain to Babylon. The Byzantines perfected it: the solidus, 4.5 grams of pure gold, unchanged for seven hundred years — the longest monetary stability in human history. Then came the Italian bankers, the Spanish silver fleets, the Dutch traders, the British Empire, and finally, in a hotel in New Hampshire in 1944, the Americans. Each one inherited the throne. Each one eventually lost it. And now, for the first time since that New Hampshire hotel, the succession is in question again. What comes next?

Part I — Ancient & Medieval Eras 3000 BCE to 1400 AD: Gold, Silver, and the First Safe Havens

Long before anyone had a word for “currency,” humans understood fear. A Mesopotamian merchant in 2500 BCE knew that grain rotted, cattle died, and land could be seized — but silver? Silver you could hide. Silver you could carry. Silver a stranger would accept without knowing your name or your king. When the first coins were struck in Lydia around 700 BCE, they formalised what terrified people had known for millennia: some things hold their value when everything else falls apart. The only question was which things. For the next three thousand years, the answer would shift from silver to gold to empire-stamped coins — each transition triggered by crisis, each new safe haven built on the ashes of the last.

In 312 AD, a Roman emperor named Constantine made a decision that would echo for seven centuries. He minted a new coin: 4.5 grams of pure gold, stamped with his face, called the solidus. And then — here is the remarkable part — his successors never changed it. Not once. For 700 years, every Byzantine emperor who sat on the throne in Constantinople maintained that exact weight, that exact purity. A merchant in 5th-century Alexandria could accept a solidus from a stranger without testing it. A Norse trader in the 9th-century Baltic hoarded solidi because nothing else on earth was as reliable. Contemporaries called it “the dollar of the Middle Ages” — not as metaphor, but as fact. It was the currency in which international debts were settled, hoards were kept, and fear was parked.

And then, in the 10th century, the emperors got greedy. Wars were expensive. The treasury was empty. Surely no one would notice if the coins were a little less pure? They noticed. Within a generation, the solidus — 700 years of accumulated trust — was worthless for international trade. The lesson was brutal and it would repeat throughout history: safe haven status takes centuries to build and decades to destroy. Remember this pattern. We will see it again.

When Constantinople’s emperors debased the solidus, someone had to fill the void. Two Italian city-states answered the call — Florence and Venice — and in doing so invented modern banking. Florence struck the first florin in 1252: 3.5 grams of pure gold, the first major European gold coin in over 500 years. Within decades, 150 cities across Europe were minting their own florins to the exact same standard. This was history’s first currency network effect — the same dynamic that makes the dollar dominant today.

Venice went even further. The Venetian ducat, minted from 1284, achieved 99.47% gold purity — the highest metallurgical standard possible with medieval technology. Leonardo da Vinci was paid 400 ducats per year by the King of France (about $56,000 in today’s money). The Medici bank built the world’s first international banking network: branches in Florence, London, Bruges, Venice, and Lyon, all settling accounts in florins without physically shipping gold. They had invented the bill of exchange — history’s first derivative. And then, in the 1530s, Spanish silver flooded Europe from the New World. The florin couldn’t compete with the scale. The last one was struck in 1531. Another safe haven, eclipsed by a bigger one.

Part II — The Age of Silver and Empire The Spanish Piece of Eight: The First Truly Global Currency

In 1545, a Quechua llama herder named Diego Huallpa was chasing a stray animal up a Bolivian mountainside when he discovered something that would reshape the entire global economy. The mountain was called Cerro Rico — “Rich Mountain” — and it was, quite literally, made of silver. At its peak, Potosi alone supplied 60% of the world’s silver. The Spanish Crown had stumbled into a river of money that would fund three centuries of empire — and accidentally created the first truly global currency.

The Spanish Piece of Eight — the real de a ocho — became something no currency had ever been before: accepted everywhere. A merchant in Seville could spend it. A trader in Manila could spend it. A silk dealer in Canton would only accept it. China, the world’s largest economy, ran a structural trade surplus with everyone and demanded payment in Spanish silver — nothing else. Thousands of tonnes flowed from Bolivian mines into Chinese vaults. The Piece of Eight was legal tender in the United States until 1857. When Alexander Hamilton designed the dollar, he literally averaged a sample of worn Spanish coins to determine the weight. The dollar sign ($) almost certainly comes from the Pillars of Hercules stamped on every Piece of Eight. Every currency in the Americas, plus the yen, the yuan, and the dollar itself, are direct descendants of that Quechua herder’s mountain.

Here is the strangest fact about the Spanish Piece of Eight: it remained the world’s dominant currency for 300 years — long after Spanish power had faded. Why? Because the coin itself never changed. Each Piece of Eight contained exactly 25.563 grams of fine silver, minted to the same standard in Spain, Mexico, Lima, and Potosi. The milled edge prevented clipping. The weight could be verified anywhere on earth with a simple scale. In a world without central banks, the coin’s safe haven property was its physical content — not a government’s promise.

This is the critical lesson for understanding the dollar today. The Piece of Eight outlasted Spanish decline because it was backed by metal, not by Madrid. When Spain weakened, the coin didn’t. But the dollar, since 1971, is backed by nothing but American institutional credibility. It has no intrinsic value. It cannot be weighed on a scale. The dollar’s safe haven status is contingent on the continued political and fiscal credibility of the US government. That contingency was invisible for 54 years. After Liberation Day, it is visible. And visibility changes everything.

Part III — The Dutch Guilder & The First Financial Revolution The Amsterdam Exchange Bank and Paper Money as Safe Haven

In 1602, a group of Dutch merchants did something that had never been done before: they created a company that anyone could own a piece of. The VOC — the Dutch East India Company — was the world’s first joint-stock corporation. You could buy shares. You could sell them. You could collect dividends. And for nearly two centuries, those dividends ran 18-25% annually, funded by a monopoly on the spice trade from the Indian Ocean. But here’s what matters for our story: the VOC issued bonds denominated in Dutch guilders. And those bonds became something new in financial history — the first paper safe haven.

The Amsterdam Exchange Bank, founded in 1609, completed the revolution. You could deposit your gold and silver coins — clipped, worn, debased by a dozen kings — and receive paper receipts backed by the Bank’s full metallic reserves. Those receipts circulated across Europe because merchants trusted the Amsterdam Exchange Bank more than they trusted any sovereign’s coins. For the first time in history, trust in an institution replaced trust in metal. The guilder dominated global finance not because the Dutch had the biggest army, but because they had the most trustworthy bank. This was the prototype for everything that came after — including the dollar. And like everything that came after, it eventually failed: the VOC went bankrupt in 1799, Napoleon occupied the Netherlands, and the institutional trust that had taken two centuries to build evaporated in a decade.

Part IV — The Age of Sterling 1870–1931: The British Pound and the Empire’s Balance Sheet

At the height of the British Empire, the pound sterling was more than a currency — it was the language of global commerce. Sixty percent of the world’s foreign exchange reserves. The settlement currency for the majority of international trade. One pound bought $4.86, and that rate was backed by something no previous paper currency had ever achieved: a credible promise. The Bank of England, operating since 1694, would convert your pounds to gold at a fixed rate, no questions asked. For over a century, that promise held. Sterling wasn’t trusted because Britain had the biggest navy (though it did). It was trusted because the Bank of England had never broken its word.

And then came the war that changed everything.

The First World War cost Britain everything — its young men, its wealth, and its status as the world’s creditor. By 1918, Britain owed America more than anyone owed Britain. The empire was bankrupt. And yet, in 1925, a politician made a decision that would haunt him for the rest of his life. Winston Churchill, then Chancellor of the Exchequer, announced that Britain would return to the gold standard at its pre-war rate of $4.86 per pound. The problem? The pound was worth about 10% less than that. Churchill had pegged sterling at the wrong price out of pride — and in doing so, created a target that every speculator in the world could see.

For six years, Britain bled gold trying to defend an indefensible rate. British exports became too expensive. Unemployment soared. And in September 1931, the wolves finally came. A speculative assault drained the Bank of England’s gold reserves in weeks. On September 19, 1931, Britain surrendered. The gold standard was abandoned. The pound fell 25% in a month. Countries holding sterling — India, Australia, Egypt, half the empire — absorbed catastrophic losses. Two hundred years of monetary credibility, destroyed in six years by one man’s pride. Churchill later called it the greatest mistake of his political life. He was right.

Part V — Bretton Woods and the Dollar’s Coronation 1944: The Secret Hotel Meeting That Redesigned the World

July 1944. The Mount Washington Hotel in Bretton Woods, New Hampshire. Seven hundred and thirty delegates from 44 nations, gathering to decide who would rule global finance for the next century. But the outcome was never really in doubt. America held 65% of the world’s gold. Every other power at the table was either bankrupt, bombed, or indebted to Washington. The British sent John Maynard Keynes — the most brilliant economist of his generation — with a proposal for a neutral supranational currency called the “bancor.” Fair. Balanced. Issued by no single nation. The Americans sent Harry Dexter White with a counter-proposal: the dollar. White won. Keynes reportedly wept on the final day.

The Bretton Woods agreement crowned the dollar king of the world. Every major currency would peg to the dollar. The dollar alone would peg to gold at $35 per ounce. This was not a market outcome — it was the most deliberate act of monetary coronation in human history. And for 27 years, it worked. Then, on August 15, 1971, Richard Nixon appeared on television and severed the dollar from gold forever. The king kept his crown, but the crown was now made of paper. What had been a currency backed by metal became a currency backed by nothing but American institutional credibility. That credibility held for 54 years. Then came Liberation Day.

For 80 years, there was one rule in global finance that never failed: in a crisis, the dollar rises. It didn’t matter what caused the crisis. 1987 crash? Dollar up. 1997 Asian contagion? Dollar up. 2008 financial collapse? Dollar up. 2020 pandemic? Dollar up. The rule was so reliable that traders treated it as a law of nature. Then came April 2, 2025 — Liberation Day — and the law broke.

On Liberation Day, the United States announced sweeping new tariffs that triggered a global market panic. US stocks fell. And here’s where it got strange: US Treasury bonds fell too (yields spiked). And the dollar — the dollar that was supposed to rise in every crisis — also fell. All three. Simultaneously. Deutsche Bank’s George Saravelos called it “a simultaneous collapse in the price of all US assets.” This had never happened before. Not in 1987. Not in 2008. Not ever. The dollar’s 80-year safe haven rule was broken because the US itself was the source of the crisis. And you cannot flee to the dollar when the dollar is what you’re fleeing from.

CEPR research published in January 2026 now confirms what Liberation Day demonstrated: the dollar only functions as a safe haven during crises of external origin — funding stress, foreign wars, pandemic panic. When the crisis originates in America — policy chaos, institutional breakdown, fiscal credibility erosion — the dollar is not the refuge. It is the problem. The Swiss franc and yen appreciate during crises regardless of where they start. The dollar doesn’t. That conditional behaviour disqualifies it from the classical safe haven definition. Rules broken once are never quite unbreakable again.

Part VI — The Swiss Franc 1914 to Today: 110 Years Without a Significant Failure

Now we come to the quiet champion — the currency that has outlasted every empire, survived every war, and appreciated against every rival for 112 years without a single significant failure. The Swiss franc. In 1914, one dollar bought 5.13 Swiss francs. Today, one Swiss franc buys more than one dollar. That is a 500% appreciation in real terms across more than a century. No other currency in the history of modern finance comes close.

The franc’s secret? Switzerland was never part of the catastrophe. In the 1920s, while German marks became wallpaper and Austrian savings evaporated overnight, Switzerland maintained its gold standard, balanced its budgets, and watched as frightened capital poured across its borders. The Swiss didn’t conquer anyone. They didn’t colonise anyone. They simply didn’t destroy their currency — and in a century where everyone else did, that was enough to make them the world’s safest vault. The numbered Swiss bank account, created by the Banking Act of 1934, became the mechanism through which the world’s frightened wealth found its way into francs. But the franc’s safe haven status came at a price — and that price was moral.

Here is the ugliest truth about safe havens: neutrality has no conscience. During the Second World War, the Swiss franc was the only freely convertible currency on earth besides the dollar. Both sides needed it. The Nazis needed Swiss francs to buy tungsten from Portugal, food from Argentina, ball bearings from Sweden. The Allies needed Swiss francs as the only safe haven outside American control. And so, between 1939 and 1945, the Swiss National Bank accepted approximately CHF 1.7 billion in gold from Nazi Germany — roughly $8.5 billion in today’s money. An estimated 316 million of that was looted: from the central banks of Belgium, the Netherlands, and Norway; from the dental fillings of Holocaust victims. The franc was trusted by both sides precisely because Switzerland refused to choose a side.

This is the price of perfect neutrality. Without Swiss franc convertibility, Germany’s war economy would have faced currency constraints years earlier. The franc’s safe haven status was purchased — at least in part — by refusing to exercise the moral judgment that would have compromised it. The Bergier Commission documented this in 2002. Switzerland paid $1.25 billion in restitution in 1998. But the currency lesson remains: a safe haven that takes sides is no longer a safe haven. The franc’s 112-year track record was built on this principle. Whether that principle is admirable or monstrous depends on when you needed the franc and what you were fleeing from.

The franc’s modern mechanics tell a simple story: Switzerland runs surpluses, carries almost no debt, and changes leaders so frequently that no single politician can destabilise policy. But the most revealing moment in recent Swiss monetary history came on January 15, 2015 — a day traders call “Francogeddon.”

For three years, the Swiss National Bank had been fighting its own currency. The franc was so sought-after as a safe haven that it kept appreciating, crushing Swiss exporters. The SNB drew a line: 1.20 francs per euro, no stronger. They printed hundreds of billions of francs to defend that floor. And then, without warning, they surrendered. On January 15, 2015, the SNB abandoned the floor. The franc surged 25-30% in minutes. Currency brokers went bankrupt. Swiss watch companies saw their prices spike overnight. Retail traders lost everything. But here’s what everyone misses about Francogeddon: it wasn’t evidence that the franc is dangerous. It was evidence that the franc is too good a safe haven. The SNB wasn’t fighting weakness — it was fighting strength. No other currency in the world has that problem.

The Complete Historical Record: Every Major Crisis, Every Safe Haven Response

Part VII — The Japanese Yen’s Paradox A Safe Haven Built on Debt and Disappearing Mechanics

Here is a riddle: How can the most indebted developed nation on earth, with 250% debt-to-GDP, persistent trade deficits, negative interest rates, and a shrinking population, also be one of the world’s most reliable safe haven currencies? The answer reveals something profound about how modern financial markets actually work — and why that mechanism is now breaking down.

The story begins in the mid-1990s, when the Bank of Japan cut rates to nearly zero. Suddenly, anyone in the world could borrow yen for almost nothing. And they did. Hedge funds, pension funds, speculators — everyone borrowed yen and invested it in higher-yielding assets: Australian bonds, US Treasuries, emerging market debt. Trillions of dollars of “short yen” positions built up over two decades. Then, whenever a crisis hit — 1998, 2008, 2020 — everyone panicked, sold their risky assets, and rushed to buy back yen to repay their loans. The yen surged. Not because Japan was safe, but because the world owed Japan money and suddenly needed to pay it back. The yen’s safe haven status was never about Japan. It was about debt mechanics.

But here’s the twist that changes everything: the BOJ is now raising rates. In August 2024, a single BOJ policy signal caused the Nikkei to crash 12% in one session — the worst day in decades — as $4 trillion in carry trades unwound simultaneously. The S&P 500 fell 3%, and there was no fundamental reason for it except that the yen’s old mechanics were being dismantled. With BOJ rates at 0.75% and rising, the cheap-yen-borrowing era is ending. By 2028, the yen may simply be a normal currency again, moving on fundamentals rather than debt mechanics. One of the world’s three major safe havens is being dismantled in real time. What fills the gap?

Part VIII — The Dollar’s Contested Throne Why 56.9% Is Not 71% and Why the Gap Matters

Now we arrive at the question this entire article has been building toward: Is the dollar losing its throne?

The numbers tell a story of slow-motion erosion. In 1999, the dollar accounted for 71% of global foreign exchange reserves. By Q3 2025, that number had fallen to 56.9%. That’s 14 percentage points lost in 25 years — and the decline has survived every crisis that should have stopped it. The 2008 financial crisis should have scared the world back into dollars. It didn’t. The 2020 pandemic should have reinforced American dominance. It didn’t. The decline is not cyclical. It is structural, and it is compounding.

But here’s what the dollar bears get wrong: there is no alternative. Not yet. The dollar is still on one side of 89.2% of all currency transactions on earth. The renminbi is blocked by capital controls — China won’t let capital flow freely, which means foreigners can’t trust holding it. The euro is fragmented — there’s no unified European treasury, so there’s no true eurozone safe asset. The Swiss franc is too small to absorb global flows without the SNB fighting every trade. Gold can’t be digitally settled. The dollar isn’t being replaced because nothing can replace it. Not yet. But the erosion continues anyway — into gold, into euros at the margin, into anything that isn’t a single country’s liability. And that erosion, compounding over decades, eventually tips thrones.

Gold surpassed the euro as the second-largest reserve asset globally by value in 2025 — driven by record central bank buying. This is the market’s verdict on the reliability of currency safe havens. Sources: IMF COFER, WGC, BIS

Part IX — The Current Hierarchy March 2026: Every Safe Haven Currency Assessed

The safe haven hierarchy in March 2026 is undergoing the most significant reshuffling since the Nixon Shock of 1971. Three major developments have occurred simultaneously: the franc has delivered its strongest multi-year performance in decades, confirming its structural dominance; the yen’s mechanical safe haven properties are visibly diminishing as BOJ normalises; and the dollar has broken its own 80-year safe haven rule on a globally visible occasion. The following table assesses each currency against the five classical safe haven criteria.

| Currency | Safe Haven Since | Mechanism | Current Account | Yield Level | Neutrality/Institutional Independence | 2026 Status | 2031 Outlook |

|---|---|---|---|---|---|---|---|

| CHF | 1914 (WWI) | True safe haven: neutrality + fiscal discipline + current account surplus | Strong surplus | Near zero/low | Political neutrality since 1815 · SNB independent | Strongest active SH | Durable |

| JPY | Mid-1990s | Mechanical: carry trade unwind; not true safe haven fundamentals | Deficit trending | Low but rising | BOJ independent (historically) | Transitional | Diminishing as BOJ normalises |

| USD | 1944 (Bretton Woods) | Funding stress instrument; dominant reserve but conditional safe haven | Persistent deficit | High (carry target) | Fed independence questioned 2025–26 | Contested | Contested · gradual erosion |

| EUR | Partial, crisis-dependent | Partial safe haven in dollar crises; risk asset in eurozone crises | Aggregate surplus | Moderate | ECB independent · no fiscal union | Partial beneficiary | Gradual gain if fiscal union advances |

| Gold (XAU) | Pre-history | Non-sovereign store of value; central bank reserve diversification | N/A — no issuer | Zero (cost to hold) | No political authority · neutral by definition | Structural bull ~$4,386 | Record buying continues |

| CNY | Not yet | Trade settlement growing; capital controls prevent reserve status | Persistent surplus | Moderate | Capital controls · authoritarian governance | Challenger · decade+ timeline | Still emerging |

Part X — Market Implications How Safe Haven Currency Dynamics Move Every Asset Class

Safe haven currency dynamics are not merely a foreign exchange phenomenon. They are a systematic signal that propagates through every major asset class simultaneously, because a shift in safe haven currency preference represents a fundamental reassessment of global risk architecture. The following analysis covers the cross-asset implications of the current safe haven hierarchy and its expected evolution through 2031.

CHF: EUR/CHF target 0.92–0.93 end-2027 (RBC). USD/CHF at 11-year highs. CHF is the cleanest long against energy-importing currencies (EUR, JPY, KRW, INR) in a sustained geopolitical risk environment. SNB intervention risk limits upside but does not reverse the structural trend. The Swiss franc appreciates in every crisis regardless of origin — the one criterion the dollar definitively fails.

JPY: USD/JPY at 158.64 reflects the tug-of-war between BOJ normalisation (yen-positive: reduces carry, raises yields) and energy cost pressure (yen-negative: Japan imports 95% of crude from Middle East). The Hormuz crisis has created an unusual JPY dynamic where the geopolitical risk that normally strengthens the yen through carry unwind is simultaneously worsening Japan’s terms of trade through higher energy costs. USD/JPY likely to test the 160 ceiling pending Hormuz resolution and BOJ policy clarity.

USD: The ING assessment (February 2026) characterises the 2026 dollar decline as “more cyclical than structural” — a view shared by Julius Baer and supported by the IMF COFER data showing reserve share declines are gradual, not catastrophic. The dollar remains the world’s shock absorber in true systemic crises. But Liberation Day 2025 demonstrated that when the US is the origin of uncertainty, the dollar falls rather than rises. Any US-originating policy shock — Fed independence concerns, fiscal sustainability questions, tariff escalation — is now explicitly dollar-negative, regardless of global risk conditions.

Safe haven currency flows serve as a leading indicator for equity market risk appetite with a consistent and quantifiable historical relationship. When CHF and JPY are appreciating simultaneously against G10 peers during a risk-off episode, the empirical record shows: S&P 500 typically down 2–8% within the following three weeks if the appreciation is sustained. European equity markets (Stoxx 600) typically underperform the S&P 500 by 3–6% as European energy cost exposure (particularly relevant to CHF safe haven flows) feeds into earnings estimates. Emerging market equities face the most acute pressure — EM currencies typically fall 3–8% during CHF/JPY combined appreciation episodes, tightening domestic financial conditions.

The current 2026 episode is atypical because it combines CHF safe haven appreciation (geopolitical risk signal) with USD weakness (US institutional credibility signal) simultaneously — a combination that historically has not occurred. The S&P 500 is down only 4% from peak despite Brent above $100. JPMorgan’s framework (every $10 oil rise = 2–5% EPS reduction) implies 6–15% EPS headwind if sustained — suggesting the equity market is not yet pricing the full oil-safe haven combined risk.

The bond market dimension of the current safe haven currency shift is the most consequential for portfolio construction. In classical risk-off episodes, flight-to-quality buying drives government bond prices up (yields down) simultaneously with safe haven currency appreciation. The current episode is inverted: US Treasury yields are rising (prices falling) while the CHF and gold are simultaneously hitting multi-year highs. This configuration — safe havens appreciating but bonds declining — signals the market is pricing stagflation risk rather than deflationary recession risk. In a stagflation environment, neither traditional safe haven portfolio construction (long bonds, long safe haven FX) nor traditional risk-on allocation (equities, credit) works cleanly. Gold and CHF, which appreciate in both inflation and risk-off environments, become the dominant portfolio hedges. This is precisely the dynamic currently visible in market positioning.

Part XI — Technical Analysis: Currency by Currency Key Levels, Chart Structure, and Trade Frameworks for Every Safe Haven Pair

Technical analysis of safe haven currencies requires a layered approach: the structural (multi-year chart patterns that reflect reserve currency dynamics), the tactical (monthly and weekly levels that define tradeable range boundaries), and the operational (daily and intraday support/resistance that market participants actively reference). The following section addresses each major safe haven currency and commodity across all three timeframes, integrating the fundamental context established above with the precise levels that currently define market structure.

Technical 1 — USD/CHF Correcting a Multi-Year Downtrend: Where Bears Re-Enter and Bulls Stall

USD/CHF has been in a structural downtrend from the 2022 high at 1.0146, declining to a cycle low of 0.7603 in early 2026 as CHF safe haven flows intensified under the Hormuz crisis and continued dollar institutional credibility erosion. The pair is currently staging a corrective rebound from that low — technically a bounce within a larger downtrend rather than a structural reversal.

Current price: ~0.7951 (corrective rebound from 0.7603 cycle low)

Structural context: Trading inside a descending channel from 1.0146 (2022 peak). The current rally is assessed as a corrective bounce targeting 38.2% Fibonacci retracement of the full 1.0146–0.7603 decline at 0.8213. The 55-week EMA at approximately 0.8091 is the critical dividing line: a sustained close above this level would suggest the decline from 0.9200 is being corrected at a larger degree. Rejection at the 55W EMA would resume the structural downtrend toward 0.7382 (100% projection of the decline from 1.0146 to 0.8332, measured from 0.9200).

Key resistance levels: 0.7926/27 — confluence of 2026 yearly open and 61.8% Fib retracement of the November decline (primary near-term resistance). 0.7958/0.7975 — 200-day MA zone (next resistance if 0.7927 breaks). 0.8033 — yearly high-day close. 0.8091 — 55-week EMA (structural decision point). 0.8101 — November high-day close. 0.8213 — 38.2% retracement of 1.0146–0.7603 (corrective rally target).

Key support levels: 0.7842 — 38.2% retracement of the January advance (initial corrective support). 0.7823/29 — 2025 swing low / 50% retracement zone (median line support on ascending pitchfork; a close below signals deeper correction). 0.7746 — key support; break invalidates the corrective bounce thesis. 0.7603 — cycle low (structural floor).

Momentum: RSI (14-day) at ~38 — suggests the pair is in oversold-to-neutral territory on the daily timeframe, consistent with a corrective bounce attempting to extend. MACD turning positive on daily suggests short-term momentum is with the upside correction. Weekly signal: still bearish, consistent with the larger downtrend.

Trading framework: Bears look to re-enter on rejection at 0.7926/27 or the 200-day MA zone with stops above 0.8033. Bulls with a correction thesis target 0.8091–0.8213 but face significant structural resistance. Any failure to break 0.7927 confirms the descending channel remains intact and the structural downtrend toward sub-0.75 is the dominant path.

Correlation note: USD/CHF has a -0.96 correlation with EUR/USD and a -0.82 inverse correlation with gold (XAU/USD). A sustained gold rally above $4,800 historically pressures USD/CHF below current support zones. Monitor the EUR/USD breakout at 1.08/1.09 for synchronised directional signal.

Technical 2 — USD/JPY The 140–160 Range That Has Defined Three Years: BOJ Hikes vs Dollar Strength

USD/JPY has been trading within a wide 140–160 lateral range since January 2024, with neither bulls nor bears able to establish sustained breakout above 160 or below 140. The pair is currently at approximately 158–159, testing the upper boundary of this range as energy cost pressures offset BOJ normalisation benefits, with recent price action challenging the 200-day SMA resistance zone.

Current price: ~158.64 (recovering from 140 area lows toward the 200-day SMA resistance)

Structural context: The dominant feature is the 140–160 lateral range that has contained price since 2024. Above 160 triggers Ministry of Finance intervention risk (the 160 level has been an explicit line-in-the-sand for Japanese authorities, evidenced by coordinated intervention in 2024). Below 140 triggers carry unwind dynamics. The pair’s direction within this range is determined by the differential between Fed rate expectations and BOJ hike trajectory. Currently: BOJ at 0.75%, signalling further hikes; Fed paused. The rate differential is compressing, which is structurally yen-positive over the medium term.

Key resistance levels: 149.27 — 50-period simple moving average on weekly chart (immediate overhead resistance). 150.00 — psychological and round-number resistance (also near current 100-day SMA). 152.43 — upper end of 2026 consensus forecast range. 155.00 — next major level where selling pressure typically re-emerges. 158.00 — interim resistance before the critical 160 zone. 160.00/160.60 — intervention zone; upper boundary of the multi-year lateral range.

Key support levels: 147.50–148.00 — near-term support (converging moving averages on daily). 145.00 — mid-range support within the 140–160 band. 142.00–143.00 — significant support zone (2025 lows region). 140.00 — structural floor; the level that has prevented deeper losses since 2024. 138.00 — post-140 break target (BOJ hike scenario).

BOJ scenarios: If BOJ hikes to 1.00% by H2 2026 (base case per market pricing), USD/JPY faces structural pressure toward 142–145. If BOJ hikes to 1.5%+ by 2027, the 140 floor is at serious risk of breaking, with the August 2024 episode (Nikkei −12% in one session) as a roadmap for the violence of yen appreciation when carry unwinds. The 200-day SMA (currently rising toward 156) provides medium-term resistance context: the pair needs to close above this convincingly to re-establish bullish momentum.

Momentum: Daily RSI at ~64 (Investing.com data) — approaching overbought on the recent bounce, suggesting momentum may stall at current resistance levels. Monthly signal: Strong Buy on moving average alignment, reflecting the dominant multi-year USD strength trend. But MACD on weekly timeframe showing declining histogram, consistent with bearish divergence at the medium-term level.

Trading framework: Range traders sell 155–158 and buy 141–143. Trend-following longs above 160 become structurally sound only with sustained break of the range ceiling (rare given intervention history). Carry trade expressions (long USD/JPY) become progressively less risk-adjusted as BOJ rate path compresses the differential. The next 18 months will likely see this range test both boundaries at least once.

Technical 3 — EUR/USD Breaking the Dollar Narrative: EUR Gaining as USD Safe Haven Premium Erodes

EUR/USD has staged one of the most significant reversals of recent years, recovering from the January 2025 near-parity levels (EUR/USD ~1.02–1.03 range) to trade above 1.15 in March 2026. The recovery reflects both structural dollar weakness (post-Liberation Day safe haven credibility erosion) and eurozone resilience (German fiscal stimulus, ECB credibility maintained). The technical picture is constructive medium-term as the pair tests the 1.15–1.16 resistance zone.

Current price: ~1.1562 (testing the 1.15–1.16 resistance zone amid dollar weakness and Iran ceasefire developments)

Key resistance levels: 1.0900 — round number psychological resistance / prior consolidation ceiling. 1.1000 — major psychological level; also near the 200-week SMA. 1.1200 — medium-term target in the dollar bear scenario (ING base case for EUR/USD by end-2026). 1.1400–1.1550 — longer-term recovery target if US fiscal concerns escalate. 1.1600 — 2022 high-close area; structural ceiling for any multi-year euro recovery.

Key support levels: 1.0700–1.0740 — near-term support (50-day SMA area). 1.0600 — medium-term support (convergence of prior highs from 2025). 1.0400–1.0450 — significant support zone (2025 multi-month lows). 1.0200 — near-parity support (structural floor established January 2025).

Fundamental-technical integration: EUR/USD has a -0.96 correlation with USD/CHF. The pair’s direction in 2026 will be primarily determined by (1) US fiscal and institutional developments, (2) ECB rate path vs Fed, and (3) eurozone fiscal union progress (German stimulus program €500B). ING’s base case is EUR/USD rising toward 1.12–1.15 in H2 2026 as US growth slows, the Fed cuts rates, and eurozone fundamentals outperform. A breach of 1.1000 with sustained closes would shift institutional positioning toward that target meaningfully. A break back below 1.0600 would signal the dollar recovery thesis is gaining traction and reassert the near-parity narrative.

Momentum: Bullish above 1.0700 on all intermediate timeframes. RSI at moderate levels (not overbought), suggesting room for continuation. The pair’s clean bullish construction from the 2025 lows argues for treating dips toward 1.0700–1.0750 as technically constructive entry points in the USD-bear thesis.

Technical 4 — Gold (XAU/USD) All-Time Highs, Corrective Phase, and The Path to $6,000+

Gold reached its all-time high of $5,595.42 on January 29, 2026, driven by safe haven demand into the early Iran war period and continued central bank buying. The subsequent correction — gold has pulled back to approximately $4,386 as of March 26, 2026 — represents a technically significant 22% correction from the peak. The 40-year VT Markets/NYMEX volume profile perspective is essential here: gold’s Long Term Point of Control sits much lower ($1,200–$1,400 range on a full 40-year profile), but the near-to-medium-term structure must be read from the post-2020 structure breakout. The series of higher highs and higher lows from the 2018 base remains structurally intact despite the current correction.

Current price: ~$4,386 (correction from $5,595 all-time high)

Structural context: Gold broke decisively above the long-term resistance zone of $2,100 in early 2024 and has since established $4,000 as a new psychological support floor. The current correction from the ATH to ~$4,386 is technically a 22% drawdown — within the normal range of corrections in secular bull markets. The 50-day moving average is at approximately $4,470; gold is currently below this level, suggesting near-term momentum is bearish within the larger uptrend. The 200-day MA provides structural medium-term support.

Key resistance levels: $4,500–$4,505 — near-term resistance / 50-day MA zone (traders actively sell here). $4,600–$4,650 — prior consolidation area / supply zone. $4,720–$4,725 — major resistance (October 2025 ATH close). $4,954 — Fibonacci extension resistance. $5,200–$5,300 — prior ATH trading range (breakout zone now acting as resistance). $5,261–$5,372 — major Fibonacci resistance cluster. $5,596 — all-time high (January 29, 2026). New resistance if approached: $5,854, $6,104, $6,324.

Key support levels: $4,300 — sell-side liquidity level (current near-term support). $4,200–$4,208 — key Fibonacci support / demand zone (high-conviction buyers here). $4,081 — pivot support identified by LiteFinance. $3,900–$3,925 — medium-term Fibonacci support (38.2% retracement of the post-2022 advance; World Gold Council identifies first major institutional support here). $3,800 — structural support (trend line extending from 2022 base). $3,506 — deeper support if structural breakdown occurs. $3,100 — long-term support base.

Momentum: Daily RSI ~30-35 (approaching oversold on daily timeframe) — approaching levels that have historically produced rebounds in the secular bull. Weekly: neutral/negative. Monthly: Strong Buy (Investing.com) — the longest timeframe is the most relevant for fundamental safe haven investors. MACD on the 50-day MA suggests the correction may be near exhaustion. Stochastic Oscillator — %K and %D lines converging in oversold territory on the weekly, consistent with approaching support.

Fibonacci pivot point: $4,519 (Investing.com, daily). The bullish scenario requires reclaiming this level and then $4,600 to signal correction completion. Below $4,208, the next major target is $3,900.

Key trading insight: Gold is currently the only major asset in which the fundamental thesis (safe haven demand, central bank buying, de-dollarisation, geopolitical risk) is uniformly bullish across all timeframes, while the technical picture shows a near-term correction from overbought conditions. This divergence historically resolves in the direction of the fundamental trend. The CME Gold Futures curve prices gold at approximately $4,759 for 2026 average and climbs steadily to $5,560 by 2031 — the market is structurally long gold through the end of the decade.

Technical 5 — EUR/CHF The Pure Safe Haven Expression: Where Geopolitical Fear Meets European Vulnerability

EUR/CHF is the cleanest expression of pure safe haven demand in the G10 forex market. Unlike USD/CHF, which is contaminated by US institutional risk (dollar falls when US is the source of uncertainty, complicating the safe haven signal), EUR/CHF reflects relatively clear safe haven dynamics: the franc appreciates as a refuge from European geopolitical and energy risk; the euro weakens as Europe faces energy cost pressure. In the current environment — Hormuz closure raising European energy costs, Bab el-Mandeb threat potentially compounding it, and European equities underperforming — EUR/CHF is under structural downward pressure.

Current price: ~0.9315 (FX Leaders data; RSI 44.15 — neutral-to-bearish)

Key resistance levels: 0.9325 — immediate resistance (near-term ceiling). 0.9331 — secondary resistance. 0.9340 — upper resistance band. 0.9580 — current EUR/CHF mid-rate (different source; the pair has significant intraday volatility). The EUR/CHF downtrend from 1.0500 (2021 SNB floor abandonment levels) to current levels defines the structural context: each attempted recovery has been sold.

Key support levels: 0.9302 — first support. 0.9298 — second support. 0.9285 — key support / potential floor. 0.9200 — critical long-term support (former SNB floor-era reference). Below 0.9200: RBC projects EUR/CHF at 0.93 end-2026, 0.92 end-2027. A break below 0.92 would represent a move to levels not seen since before the 2015 Francogeddon event.

Indicators: ADX at 34 (strong trend). 50-day SMA at 0.9319 (just above current price — pair trading at SMA, defining current battleground). 200-day EMA at 0.9316. Parabolic SAR: upward (short-term bullish signal within a broader bearish context). RSI neutral at 44 suggests neither extreme is dominant near-term.

Trading framework: EUR/CHF is a sell-on-rallies pair in the current geopolitical environment. Resistance at 0.9325–0.9340 provides entry levels for CHF-long expressions. The RBC end-2027 target of 0.92 is the medium-term objective. Stop above the 200-day EMA (0.9316 area) for risk management.

Part XII — Five-Year Price Projections: 2026 to 2031 Every Safe Haven Asset, Every Year, Every Key Scenario Quantified

The following five-year projections integrate three analytical frameworks: the fundamental structural case for each currency (reserve share trajectory, monetary policy path, institutional credibility), the technical structure (trend direction, key levels, momentum), and the consensus of institutional forecasts (Goldman Sachs, JPMorgan, UBS, RBC, ING, Julius Baer, Morgan Stanley). These are not predictions — they are calibrated analytical scenarios based on the balance of evidence.

| Asset / Pair | Current (Mar 26) | 2026 Year-End | 2027 Target | 2028 Projection | 2029–2030 | 2031 | Key Scenario Driver |

|---|---|---|---|---|---|---|---|

| USD/CHF | ~0.7951 | 0.74–0.80 | 0.72–0.78 | 0.70–0.76 | 0.68–0.74 | 0.65–0.72 | USD structural erosion vs CHF safe haven; 55W EMA (~0.8091) is the bull/bear dividing line |

| EUR/CHF | ~0.9315 | 0.92–0.95 | 0.91–0.93 (RBC) | 0.88–0.92 | 0.86–0.92 | 0.85–0.92 | Euro fiscal union progress vs CHF safe haven demand; SNB intervention risk limits extreme CHF strength |

| USD/JPY | ~158.64 | 145–155 | 138–150 | 132–145 | 125–140 | 120–135 | BOJ normalisation compresses carry differential; 140 floor breaks if BOJ reaches 1.5%+ by 2027–28 |

| EUR/USD | ~1.1562 | 1.10–1.15 (ING base) | 1.12–1.18 | 1.10–1.20 | 1.08–1.18 | 1.05–1.18 | US fiscal and institutional credibility vs eurozone fiscal union progress; ECB vs Fed rate differential |

| DXY Index | ~99.4 | 98–104 | 94–102 | 90–100 | 88–98 | 85–96 | Structural decline as reserve share falls; cyclical recoveries possible; no longer gains in all crises |

| Gold XAU/USD | ~$4,386 | $4,700–$5,200 | $5,000–$6,206 (GS/JPM) | $5,500–$7,596 | $6,000–$8,285 | $6,500–$9,000+ | Central bank buying structural; de-dollarisation; CME futures price $5,560 by 2031; BofA extreme bull: $8,000 |

| GBP/USD | ~1.2950 | 1.28–1.36 | 1.28–1.38 | 1.25–1.38 | 1.22–1.38 | 1.20–1.40 | GBP is a risk asset, not a safe haven; tracks US growth and UK fiscal health; RBC end-2026: 0.86 EUR/GBP |

| USD/NOK | ~10.50 | 9.80–10.80 | 9.50–10.50 | 9.00–10.50 | 9.00–10.80 | 8.50–10.50 | NOK strongest oil-price beneficiary in G10; Brent above $100 = NOK appreciation; oil bull supports |

Key technical support ladder: $4,208 (Fib support) → $3,900 (55-day MA / medium-term) → $3,800 (trend line) → $3,506 (deep support). Key resistance ladder: $4,954 (Fib extension) → $5,261 (major Fib) → $5,596 (ATH) → $6,104 → $6,554. The secular bull remains intact above $3,800.

2026 (Year 1): The Hormuz crisis resolution timeline is the dominant variable for all safe haven pairs. If resolved by Q3 2026: dollar stabilises, CHF holds gains but rally decelerates, yen continues transitional behaviour, gold corrects toward $4,200–$4,700. If Hormuz stays closed into Q4 2026: gold pushes toward $5,500+, CHF breaks structurally lower vs EUR and USD hits new lows, yen faces the tug-of-war between carry unwind (positive) and energy cost (negative) with neither dominating clearly. EUR/USD likely in 1.10–1.15 range by year-end in either scenario as US institutions remain under pressure.

2027 (Year 2): BOJ normalisation trajectory becomes the dominant JPY driver. If BOJ reaches 1.0%+ by mid-2027, USD/JPY structural downtrend resumes toward 138–142. Gold’s structural bull case receives Goldman Sachs’ $5,000 target validation by year-end with central bank buying sustained. EUR/CHF likely in 0.91–0.93 zone as ECB-SNB policy differential stabilises. Dollar reserve share falls toward 54–55% on IMF COFER data — the first time below 55% since the pre-Bretton Woods era.

2028–2029 (Years 3–4): The Japanese yen’s mechanical carry safe haven status is largely dismantled if BOJ reaches 1.5%+. The yen becomes a rate-driven currency, moving on growth and rate differentials rather than carry dynamics. This is the period when CHF becomes truly unchallenged as the single dominant pure safe haven in G10 FX. Gold enters the $5,500–$7,000 zone per CME futures curve and LiteFinance/BofA projections as de-dollarisation continues and central bank buying compounds. USD/JPY likely approaching 130–135 in this scenario.

2030–2031 (Years 5): By 2031, the current evidence points toward: Dollar reserve share at 52–54% (continued gradual erosion). Gold at $5,560 per CME futures (conservative) to $8,000+ (BofA bull case). CHF still the world’s dominant individual portfolio safe haven with no credible challenger on the five classical criteria. JPY a conventional rate-driven currency. EUR potentially a partial safe haven if fiscal union advances (German €500B stimulus is the first step in that direction). The multipolar reserve system is established but not completed — no single currency has replaced the dollar, but the dollar’s supremacy is unambiguously more conditional than it was in 2015.

The Safe Haven Currency Bull and Bear Cases — 2026 to 2031

Analytical framework based on structural data · Not forecasts · IMF, CEPR, RBA, Cleveland Fed, Julius Baer, ING, Goldman Sachs research

- Dollar continues slow reserve share decline: 56.9% → ~52–54% by 2031. Not a collapse, but a structural erosion that accelerates if US fiscal trajectory continues. CBO projects debt rising through 2035 with no inflection point.

- CHF cements dominant individual portfolio safe haven status. SNB will intervene periodically but cannot prevent structural franc appreciation driven by global institutional demand. EUR/CHF target 0.92 by end-2027 (RBC).

- Gold reaches $6,000–$8,000 by 2030 as central bank buying continues and no single currency commands unambiguous safe haven consensus. Gold becomes the primary sovereign reserve diversification instrument.

- JPY gradually loses carry-trade safe haven properties as BOJ reaches 1.5–2.0% by 2028. Yen becomes a more conventional currency, moving on rate differentials and trade flows rather than carry dynamics. August 2024-style crisis events become less frequent as the aggregate short position diminishes.

- EUR gains modestly if European fiscal integration advances. The German infrastructure stimulus program (€500B announced 2025) and Maastricht 2.0 framework discussions indicate genuine movement toward fiscal union — the structural prerequisite for the euro to function as a true safe haven.

- CNY remains a decade-plus timeline project. Capital controls are not politically removable in the current Chinese governance model. The RMB’s SWIFT trade finance share has quadrupled to 8.3% over four years, but this is trade settlement, not safe haven status.

- No viable alternative exists at systemic scale. The dollar’s 89.2% share of global FX transactions (BIS 2025) is a network effect that cannot be unwound on a five-year timeline regardless of US policy choices.

- US 2026 midterm elections prompt policy moderation. Tariff war de-escalation, Fed independence reaffirmed, fiscal concerns addressed. Dollar recovers Liberation Day losses and re-establishes its traditional safe haven correlation with risk-off events.

- AI investment flows into US technology assets continue generating structural dollar demand that offsets reserve diversification. Private investor inflows to US assets rose from $1.0 trillion/year (2022–2024) to $1.5 trillion in 2025 (ING data) — predominantly into equities and Treasuries.

- The ING analysis characterises 2026 dollar decline as “more cyclical than structural”: the dollar is still historically very strong by any long-run standard despite recent decline. The 2025 Liberation Day episode may prove a one-time policy-shock event rather than a structural regime change.

- Dollar financial market depth is irreplaceable. The US Treasury market remains the largest, most liquid government bond market in the world by margins that cannot be replicated by any other currency area within a decade.

- Mean reversion: the dollar has recovered from every prior 10%+ drawdown — 2008, 2011, 2020 — within 18 months. Historical base rate argues for eventual recovery, not structural decline.

The 5,000-year record of safe haven currencies yields a single consistent lesson: safe haven status is earned over decades or centuries, maintained by institutional discipline and political stability, and lost through exactly the combination of fiscal overextension, policy unpredictability, and institutional credibility erosion that is currently visible in the United States. The Byzantine solidus was debased by a government funding wars it could not afford. Sterling was compromised by a chancellor who returned to gold at the wrong rate out of pride. The dollar’s safe haven rule was broken on Liberation Day 2025 when US tariff policy created a crisis of American origin that the dollar could not survive as a safe haven.

The franc has outlasted every other modern safe haven currency not by being the largest, the most liquid, or the most economically powerful, but by being the most consistently boring in the best possible way: neutral, fiscally disciplined, with a central bank that does not take political instructions and a government that does not start wars. These properties cannot be acquired quickly. They compound over centuries. The franc’s 110-year track record against the dollar is not a coincidence — it is the accumulated compound interest of 110 years of exactly those properties, applied consistently through every crisis the world has thrown at it.

Gold reaching $5,589 per ounce in January 2026 — before the current correction to $4,386 — is the market’s verdict on the current state of the safe haven currency system. It is not speculation. It is the allocation decision of the world’s most sophisticated reserve managers — the same institutions that built and maintained the dollar-centric system — acting on the conclusion that no single currency can currently claim unambiguous safe haven status. When central banks buy gold at record pace for three consecutive years, they are not making a forecast. They are making a statement about the system they are diversifying away from.

The dollar will not be replaced quickly or suddenly. The Spanish Piece of Eight remained in circulation for decades after Spanish imperial power declined. Sterling remained a reserve currency for twenty years after its safe haven status effectively ended in 1931. Reserve currency transitions are measured in decades, not years. But the direction of travel is no longer ambiguous. The world is, for the first time since 1944, genuinely questioning whether the dollar deserves its safe haven designation — and that questioning, once started, does not stop on its own.

Key Questions on Safe Haven Currencies — Analytically Answered

Research-backed answers to the questions market participants ask most frequently

Conclusion: The 5,000-Year Pattern and What It Tells Us About 2026

We began this story with a Mesopotamian merchant sewing silver into his cloak, a Byzantine trader trusting a solidus from a stranger, and a Chinese billionaire watching the dollar fall on Liberation Day. They all asked the same question: where does money go to survive? The answer changed twelve times in five thousand years. But the pattern never changed at all.

Every safe haven currency in history followed the same arc: trust is built over decades or centuries through institutional discipline and political neutrality. It is lost through fiscal overextension and credibility erosion. The Byzantine solidus held its gold content for 700 years — until an emperor got greedy. Sterling ruled for a century — until Churchill pegged it at the wrong rate out of pride. Safe haven status is earned through boring consistency. It is lost through moments of weakness that compound.

The Swiss franc has been building its credentials for 112 years. Two world wars. A Great Depression. The end of gold. Bretton Woods and its collapse. Pandemic. Geopolitical chaos. Through all of it, the franc appreciated 500% against the dollar. Not one significant safe haven failure. Not one.

The dollar has held reserve currency status for 82 years — shorter than the franc’s safe haven run. And on Liberation Day 2025, something happened that had never happened before: the dollar fell during a crisis of American origin. US stocks fell. US bonds fell. The dollar fell. All at once. The 80-year rule was broken. Rules broken once are never quite unbreakable again.

The most important signal of 2025–2026 is not any single currency move. It is the behaviour of the world’s most sophisticated reserve managers — central banks — who have been buying gold at record pace for three consecutive years, pushing it to $5,589 in January before the current correction. These are the same institutions that built the dollar-centric system. When they diversify away from it, they are not speculating. They are making a statement about the system they no longer trust absolutely.

The solidus lasted 700 years. The florin lasted 280. The Piece of Eight lasted 300. The pound lasted 115. The dollar has lasted 82. The question is not whether it will eventually be replaced — every reserve currency eventually is. The question is whether the institutions that should prevent premature erosion are still functioning as designed. In 2026, for the first time since that New Hampshire hotel in 1944, that question is no longer rhetorical. And the answer will be written not in speeches or policy papers, but in where the world’s frightened money actually goes.

Published March 26, 2026 by The Capital Dispatch at Capital Street FX (capitalstreetfx.com). For informational and educational purposes only. Not financial advice. Not investment guidance. Sources: CEPR, IMF COFER, Cleveland Fed, RBA, BIS, Goldman Sachs, Julius Baer, ING, RBC, Bergier Commission, Swiss National Bank, Federal Reserve.