When Empires Bargain:200 Years of Tariffs, Power & Markets— and What Happens at the Trump-Xi Summit on May 14

When Empires Bargain:

200 Years of Tariffs, Power & Markets

— and What Happens at the Trump-Xi Summit on May 14

From the British Corn Laws to the Great Hall of the People — the definitive chronicle of history’s great trade confrontations, the forces reshaping the global economy right now, and what the Trump-Xi summit on May 14–15 means for every market you trade.

Overview: The World on the Eve of Beijing

In four days, Air Force One will touch down in Beijing. Donald Trump — the most aggressive protectionist to occupy the White House since Herbert Hoover — will shake hands with Xi Jinping in the Great Hall of the People, and the world’s financial markets will hold their breath. This is no ordinary diplomatic summit. It is the culmination of a trade war that has reshaped global supply chains, driven the dollar to multi-year lows, sent gold past $4,700 per ounce to within striking distance of all-time highs, and forced economies from Hanoi to Hamburg to Frankfurt to recalibrate their entire economic strategies.

The summit, scheduled for May 14–15, 2026, marks the first visit by a US president to China in nearly eight years. It arrives against a geopolitical landscape of uncommon complexity: a shooting war in the Middle East that has pushed WTI crude oil above $97 per barrel, a Chinese economy that has pivoted eastward and southward with remarkable strategic agility, a US Supreme Court that struck down Trump’s landmark tariff architecture in February, and a great-power competition that has metastasized from goods and services into semiconductors, rare earths, artificial intelligence, digital currencies, and the very infrastructure of global monetary settlement.

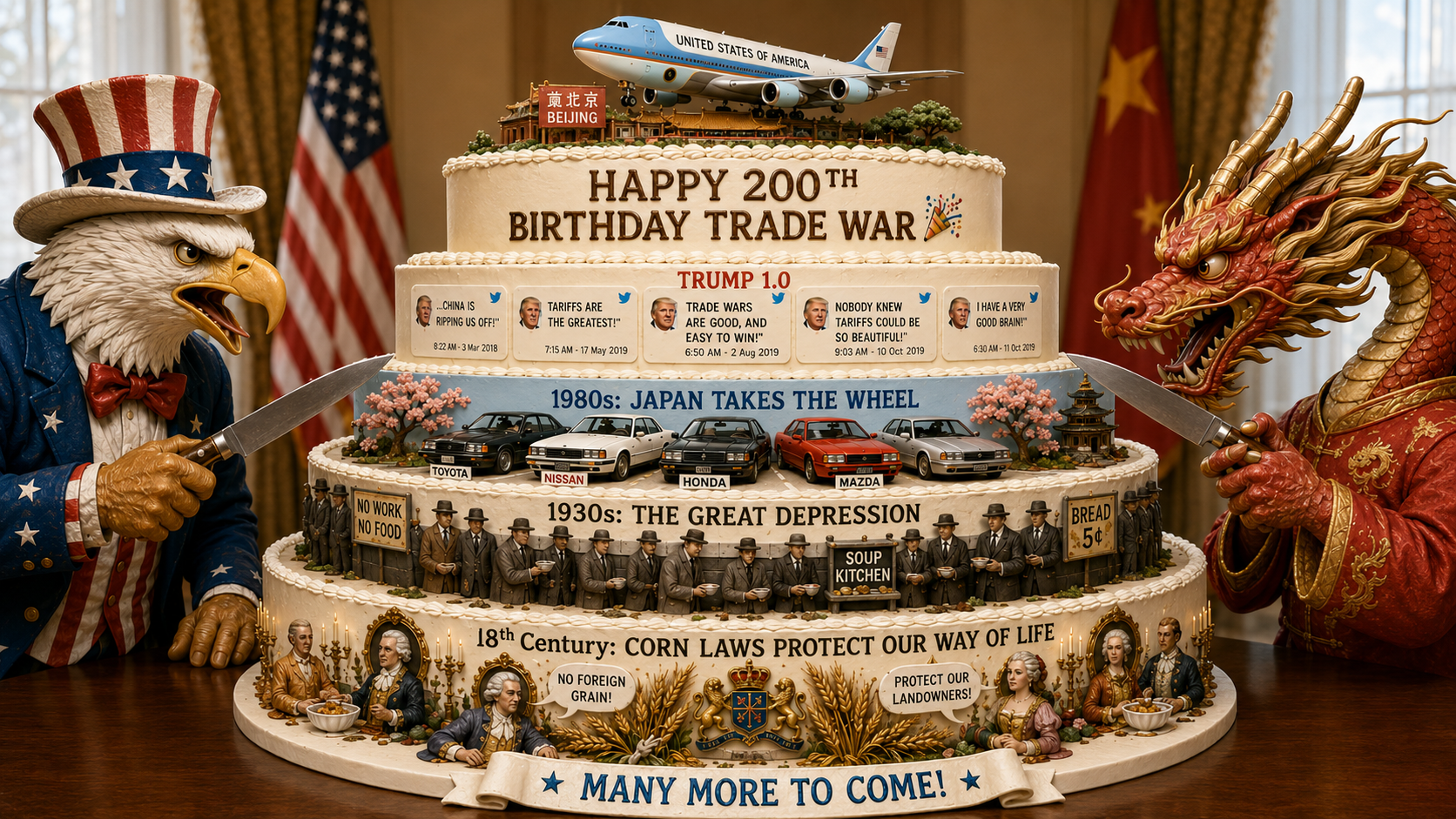

The world has been here before. Not in this precise configuration — the specific actors, technologies, and geographies are new — but the underlying dynamic is as old as the Industrial Revolution: a rising economic power challenging the established hegemon, the hegemon responding with economic coercion, and both sides discovering, slowly and painfully, that the global system is too interconnected for either to win a war of pure attrition. The British learned this after the Corn Laws. America learned it after Smoot-Hawley. Japan and Germany learned it after World War II. China has studied all of these precedents with meticulous attention. So, in a different way, has Donald Trump.

What makes 2026 different from all previous trade war episodes is the simultaneous fracturing of three systems that have underpinned global stability since 1945: the liberal trading order built around the WTO, the dollar’s monopoly on global reserve currency status, and American technological supremacy — particularly in semiconductors and artificial intelligence. In all previous trade wars, the United States held decisive structural advantages in at least two of these three domains. Today, it is contesting all three simultaneously, against a peer competitor that has spent three decades preparing for exactly this confrontation.

To understand what the Beijing summit might deliver — and what it means for your portfolio — you need to understand not just the summit itself, but the 200-year historical arc that made it inevitable, the specific structural forces that have transformed it from an economic dispute into a civilizational contest, and the precise market mechanics through which its outcome will manifest across gold, equities, forex, and commodities. That is what this analysis delivers.

- The 200-Year Pendulum: Protectionism vs. Free Trade

- The Great Trade Wars of History — Five Case Studies

- Trump 2.0: The Tariff Revolution and Its Mutations

- The Damage Report: Economic Cost and China’s Pivot

- The Beijing Summit: Stakes, Leverage and the Six Battlegrounds

- Multi-Polarity, Dedollarization and the New Monetary Order

- The Gold Story: Central Banks, Dedollarization and Structural Demand

- The Most Sensitive Markets: Where the Trade War Shows Up First

- Market Forecasts: 1 Day to 12 Months

- Three Scenarios for the Next 12 Months

- Conclusion: The Dragon and the Eagle

- FAQ

The 200-Year Pendulum: Protectionism vs. Free Trade

Every generation believes its trade war is unprecedented. It never is. Since the Napoleonic Wars ended in 1815, the world has oscillated between protectionism and free trade with the reliability of a geopolitical metronome — each wave driven by the same anxieties, each resolution reached through the same exhausting combination of economic pain, political capitulation, and creative face-saving. Understanding that rhythm is not merely a historical exercise. It is the most powerful analytical lens available for making sense of what is happening right now.

The cycle has three consistent drivers. First, rising power anxiety: whenever a new economic power challenges the established hegemon’s dominance — Britain in the 1810s, America in the 1870s, Japan in the 1970s, China today — the hegemon invariably reaches for trade barriers as a defensive tool, even as its own economists argue against it. Second, domestic political pressure: the distributional consequences of free trade (lower consumer prices but concentrated job losses in specific industries and regions) create powerful political constituencies for protection that vastly outweigh the diffuse benefits of open markets. Third, technological disruption: the Industrial Revolution, the Second Industrial Revolution, the semiconductor revolution, and now the artificial intelligence revolution have each forced a renegotiation of who produces what, with trade policy as the primary instrument of that renegotiation.

The current episode checks all three boxes with unusual clarity. China’s rise from poverty to peer economic competitor within a single generation is without historical precedent in speed. The political backlash against globalization — the deindustrialization of the American Midwest, the collapse of manufacturing communities in the UK’s North, the yellow vest movement in France — has been building since the mid-1990s and found its political expression in Trump, Brexit, and the broader populist wave. And the race for dominance in semiconductors and artificial intelligence is producing exactly the kind of geopolitical competition over strategic technologies that drove the protectionism of earlier eras.

The 200-year swing between protectionism and free trade — we are now in the early stages of the third major protectionist wave since 1815.

What makes the current episode particularly dangerous is the speed of escalation. Previous protectionist waves unfolded over decades; the current one compressed years of trade liberalization into months of reversal. The world went from a 3.5% average tariff rate in 2024 to an effective rate of 23.69% on Chinese goods in less than 18 months. No supply chain — however well-designed — can adjust to that kind of velocity without significant economic disruption. The cost is already being felt across thousands of product categories, from semiconductors to soybeans, and it is being paid primarily by consumers and small businesses, not by the political constituencies that demanded protection.

The Great Trade Wars of History — Five Case Studies

History does not offer comfort to trade war optimists. Of the five major protectionist episodes since 1815, three ended in economic catastrophe, one ended in a managed currency deal that crippled the losing side for a generation, and one ended with both sides declaring victory while the underlying imbalances remained. Understanding which of these templates most closely matches the current situation is the essential analytical task for any investor or trader active in 2026.

The Corn Laws: The Original Protectionist Blunder

Britain’s Corn Laws — a system of tariffs and restrictions designed to keep grain prices artificially high for the aristocratic landowning class — are the foundational case study in the political economy of protection. The laws did exactly what protectionist policies always do: they enriched the politically connected, impoverished consumers (contributing to the deaths of an estimated one million people during the Irish Famine of 1845–52), and retarded the development of the industrial economy by raising the wage floor that manufacturers had to pay to keep workers alive. Their repeal in 1846, after a decade-long political battle led by Richard Cobden’s Anti-Corn Law League, inaugurated the first golden age of free trade and demonstrated that protectionism, once entrenched, requires a genuine political crisis to reverse. The lesson for 2026: trade barriers, once imposed, create constituencies for their own perpetuation. Removing them requires extraordinary political will — which is why even the moderate voices in the Trump administration are reluctant to commit to a timeline for tariff reduction.

Smoot-Hawley: The Trade War That Became a Depression

The Smoot-Hawley Tariff Act of June 1930 raised US import duties to their highest peacetime level in history — averaging 45–50% on over 20,000 imported goods. The immediate consequences were catastrophic: US imports fell from $4.4 billion in 1929 to $1.3 billion by 1932, a 70% collapse. US exports fell by an almost identical proportion as trading partners — Canada, Britain, France, Germany — retaliated with their own tariffs. The Dow Jones Industrial Average fell 90% from its 1929 peak to its 1932 trough. Global trade volumes fell by 66%. The Smoot-Hawley tariff did not cause the Great Depression — that honour belongs primarily to the Federal Reserve’s monetary contraction — but it demonstrably deepened and prolonged it, converting what might have been a severe recession into a civilizational crisis. The precedent haunts every trade war discussion today: even a Supreme Court that has struck down Trump’s IEEPA tariffs cannot fully insulate the global economy from the second-order consequences of a protectionist spiral.

The Chicken Tax: The Zombie Tariff

In the early 1960s, American frozen chicken flooded European markets, devastating French and West German poultry farmers. The EEC retaliated with steep poultry tariffs. President Johnson, under pressure from American farmers, responded with a 25% tariff on European light trucks — specifically targeting Volkswagen’s Transporter van. More than 60 years later, the Chicken Tax on light trucks remains US law. It is the reason America’s pickup truck market is dominated by domestic manufacturers and the reason foreign automakers spend billions engineering workarounds — importing trucks as cargo vehicles, then converting them after arrival. The Chicken Tax is the perfect illustration of why trade barriers are so politically durable: once an industry depends on protection, removing it destroys those jobs in the short term, even if it creates more jobs in the long term. The political calculus always favors maintenance. This is exactly why the 2026 tariff landscape — once legal under Section 301 — is likely to endure well beyond any single administration.

US-Japan: The Blueprint China Deliberately Rejected

America and Japan fought a rolling, decades-long trade war across every major industry: textiles in the 1950s and 60s, steel in the 1970s, automobiles and semiconductors in the 1980s and 90s. By the mid-1980s, the US trade deficit with Japan had reached $40 billion — nearly one-third of the total US trade deficit. The US response combined tariffs, “voluntary export restraints” (quotas disguised as Japanese goodwill), and the 1985 Plaza Accord, which forced the yen to appreciate by nearly 50% against the dollar in less than two years. The resulting yen appreciation crushed Japanese export competitiveness, contributed to the asset bubble that inflated through the late 1980s, and may have played a decisive role in Japan’s subsequent “Lost Decade” of stagnation. The lesson that China drew from this was precise and operational: never accumulate enough dollar-denominated assets to be vulnerable to currency coercion; never let your economic model become as dependent on US market access as Japan’s was; and build a diplomatic network that gives you leverage the United States cannot simply buy away. China has spent thirty years implementing those lessons. This is why the current trade war is fundamentally harder to resolve than the Japan episode — China is not Japan, and Xi Jinping knows exactly why.

Trump 1.0: The Opening Shot that Crossed a Bipartisan Rubicon

Trump’s first trade war with China began with steel and aluminum tariffs in March 2018 and escalated through four major rounds to cover approximately $360 billion in Chinese goods at 25% tariffs. China retaliated on $110 billion in US goods, targeting agriculture, autos, and energy with surgical political precision — hitting soybean farmers in Iowa and corn farmers in Illinois, states Trump needed for re-election. US soybean exports to China collapsed from $12.4 billion in 2017 to $3.1 billion in 2018. American farmers received $23 billion in government bailouts — more than the federal government spent on the original Marshall Plan in inflation-adjusted terms. The S&P 500 fell 20% in Q4 2018 before recovering when the “Phase One” deal was struck in January 2020, securing Chinese commitments to purchase $200 billion in additional US goods over two years — commitments China met at approximately 58% completion. The Biden administration inherited the tariffs and, crucially, kept almost all of them, adding new layers on EVs and solar panels. Trade policy had crossed a bipartisan Rubicon: what Trump began as a negotiating tactic, Biden entrenched as strategic competition. Trump 2.0 then elevated both the scale and the ambition by an order of magnitude.

Trump 2.0: The Tariff Revolution and Its Mutations

If Trump 1.0 was a trade war, Trump 2.0 is a trade revolution — one that has proceeded in distinct phases, each more legally complex and geopolitically consequential than the last. The sheer scale, speed, and scope of the tariff offensive that began in January 2025 has no peacetime precedent in modern economic history. But understanding the current state of play requires tracking not just the tariffs themselves, but the legal architecture that sustained them, the court ruling that partially dismantled that architecture, and the administrative scramble to rebuild it on more defensible legal ground.

Phase 1: Liberation Day and the Escalation Spiral (January–May 2025)

Within weeks of returning to office, Trump imposed a 10% punitive tariff on all Chinese goods, citing fentanyl and trade imbalances. Within three months, through four escalating rounds culminating in the “Liberation Day” reciprocal tariffs announced on April 2, 2025, US tariffs on Chinese goods reached 145%. China’s retaliation topped 125% on US goods. The two largest economies in the world had effectively imposed a near-total trade embargo on each other — a situation that neither side had planned for and that created genuine economic disruption across global supply chains. The tariff revolution extended far beyond China: steel and aluminum duties reached 50% on Canadian steel; 25% tariffs were placed on all imported automobiles globally; the EU faced a 20% baseline “reciprocal” tariff and 25% on cars. Canada and Mexico found CUSMA/USMCA — the trade agreement Trump himself had negotiated in his first term — effectively suspended by executive action.

Phase 2: The Geneva Truce (May 2025)

The first inflection point came in May 2025. After weeks of behind-the-scenes negotiations — facilitated in part by Swiss intermediaries and backchannel communications through APEC — US and Chinese representatives met in Geneva and struck a 90-day tariff truce. Under the agreement, the US reduced tariffs from the 145% peak toward more manageable levels; China eased some restrictions on rare earth exports. Markets rallied sharply: gold pulled back from its highs, the yuan strengthened, and the S&P 500 rose 4% in a single week. Three weeks later, Trump declared China had violated the deal. Beijing disputed this. The escalation resumed, though at a slower pace — a pattern that would repeat itself several times over the following months.

Phase 3: The Busan Accommodation (October 2025)

The second major inflection point came on October 30, 2025, when Trump and Xi met on the sidelines of the APEC summit in Busan, South Korea. This meeting produced a substantive if carefully hedged agreement: US tariffs were trimmed from their peak effective rate of approximately 57% to around 47%; China pledged to purchase 12 million metric tons of US soybeans by end-2025 and at least 25 million metric tons annually through 2028; both sides agreed to pause their most aggressive export control measures until November 2026. Trump rated the Busan meeting “12 out of 10” in remarks to reporters. Markets, briefly, believed him.

Phase 4: The Supreme Court Strikes (February 2026)

On February 20, 2026, the US Supreme Court delivered a ruling that fundamentally altered the legal landscape of the tariff war. The court held that Trump’s broad use of the International Emergency Economic Powers Act (IEEPA) to impose global tariffs exceeded the statutory authority of the executive branch, violating the non-delegation doctrine that requires Congress to provide an “intelligible principle” guiding executive action. The ruling was a significant legal blow, invalidating the framework that had underpinned the bulk of Trump’s tariff architecture. In the immediate aftermath, markets rallied sharply — China, which had been subject to a 34% IEEPA rate on top of existing duties, found itself temporarily facing only the 10% universal baseline tariff under Section 122.

The Trump administration responded immediately by announcing it would use Section 301 (unfair trade practices) and Section 232 (national security) tariffs to rebuild the tariff wall through legally defensible channels. Two new Section 301 investigations were opened in March 2026 — one targeting Chinese industrial overcapacity, another alleging forced labor violations in Chinese supply chains. Section 301 investigations require formal hearings, public comment periods, and economic impact assessments — a timeline of at least six to nine months before new tariffs can be legally imposed. This creates a critical window of relative tariff stability between May and November 2026, within which the Beijing summit’s outcomes will largely define market direction.

Phase 5: The Iran Complication (February–May 2026)

No analysis of the current trade landscape can ignore the Middle East war. In February 2026, the United States and Israel launched military strikes on Iranian nuclear facilities, triggering a conflict that has disrupted global energy markets, driven oil prices above $97 per barrel, and added a new and volatile variable to an already complex US-China dynamic. China is the world’s largest buyer of Iranian oil — purchasing approximately 1.5 million barrels per day — and has formalized this relationship through a 25-year strategic partnership agreement signed with Tehran in 2021. The US sanctioned five Chinese refineries in April 2026 for purchasing Iranian crude. Beijing responded by invoking its Anti-Foreign Sanctions Law in May 2026, instructing Chinese companies not to comply with US sanctions — a direct legal defiance of American economic coercion that has no precedent in the bilateral relationship. The Iran war has transformed the US-China trade conflict from a bilateral economic dispute into a node within a much larger geopolitical confrontation — one in which China’s relationships with Russia, Iran, and the Global South give it diplomatic leverage that Japan never possessed during the 1980s trade wars.

The US tariff rate on Chinese goods has oscillated between 10% and 145% across five distinct phases since January 2025. The current effective rate of ~23.69% reflects post-SCOTUS Section 301 legacy tariffs.

The Damage Report: Economic Cost and China’s Strategic Pivot

The most important structural development of the past 18 months is not the tariff rate itself — it is what China has done in response. Rather than capitulating to American pressure, as Japan did after the Plaza Accord, Beijing has executed what may be the most successful strategic trade pivot in modern economic history. China’s trade surplus hit a record trillion-dollar level at the end of 2025 despite — and in some respects because of — Trump’s tariffs. How? By accelerating the shift toward alternative markets that had been underway since Trump 1.0. Chinese exports to Southeast Asia surged 28%. Exports to Africa grew 19%. Exports to Latin America and the Middle East expanded at double-digit annual rates. Chinese manufacturers found new buyers for everything America no longer wanted to purchase from them, often at prices that undercut local producers to an even greater extent than they had undercut American ones.

The structural consequences of this pivot are profound and largely irreversible. The export markets that China has built across Southeast Asia, Africa, and Latin America over the past three years are not temporary substitutes for US demand — they are permanent new economic relationships, cemented by infrastructure investment, long-term supply contracts, and the diplomatic networks of the Belt and Road Initiative. Even if the Beijing summit produces a comprehensive trade deal that reduces US tariffs to pre-2018 levels, the global trading map has been redrawn. China is less dependent on the US market than it has been at any point since its WTO accession in 2001. This is simultaneously a source of Chinese strategic confidence heading into the summit — and a sobering reality for US negotiators who believe that economic pressure alone can force meaningful concessions.

Meanwhile, the collateral damage has been globally distributed. Canadian manufacturing output fell 2.6% in 2025 as US steel and aluminum tariffs disrupted deeply integrated North American production networks. European automakers — Volkswagen, BMW, Mercedes-Benz, Stellantis — face a 25% tariff on cars exported to the US, contributing to layoffs at German and French automotive suppliers and triggering the most serious political crisis in the Franco-German economic relationship since the 2008 financial crisis. The IMF’s April 2026 assessment placed global growth under what it termed a “war darkens outlook” framework — a reference to both the Iran conflict and the lingering trade uncertainty — and revised global GDP forecasts downward for the third consecutive quarter.

Perhaps most significantly for financial markets: the yuan has not collapsed under tariff pressure, as many Western analysts predicted. It has strengthened. USD/CNY now tests 6.84 — the yuan’s strongest level against the dollar in nearly three years — as China’s current account surplus swells, yuan-denominated commodity trade expands, and confidence in Beijing’s economic management grows across emerging markets. Gold’s ascent past $4,700 per ounce reflects, in significant part, this structural shift in confidence: away from a dollar-denominated order toward a more genuinely multi-currency world in which the universally trusted neutral asset is not the dollar, but gold.

The Beijing Summit: Stakes, Leverage and the Six Battlegrounds

On May 14–15, 2026, Donald Trump will meet Xi Jinping in the Great Hall of the People. A US military C-17 transport aircraft has already landed in Beijing carrying advance security teams. A smaller-than-expected CEO delegation will accompany the president — a signal, according to sources familiar with the preparations, that the summit is being framed primarily as a relationship-building exercise rather than a grand deal-signing ceremony. That framing is itself a negotiating tactic: by lowering expectations, both sides create room to claim success from outcomes that might otherwise be characterized as modest.

Trump, speaking in late April, said he expects to receive a “big, fat hug” from Xi when he arrives — characteristically theatrical, but also revealing in what it prioritizes: optics of warm personal chemistry over substantive agreement. Xi, for his part, told Trump in a phone call that China was “willing to do bigger and better things” together with the United States — diplomatic language that signals flexibility without committing to specifics, the time-honored formula of a side that has more patience than its counterpart. The Economist’s assessment, published May 7, is characteristically sober: “Trump and Xi will struggle to strike a major economic deal.” Markets largely agree: the 58.5% probability priced in by prediction markets for a tariff agreement by May 31 suggests cautious optimism rather than conviction.

The Six Battlegrounds

1. The “Board of Trade” Framework. US Trade Representative Jamieson Greer has openly discussed establishing a formalized bilateral trade management mechanism — a “Board of Trade” — that would define priority goods for import and export, institutionalizing a managed-trade approach outside WTO norms. If agreed, this would represent a fundamental shift in the architecture of global trade: a move from multilateral rules toward bilateral barter between the two largest economies. For markets, the key question is whether such a framework would be binding or aspirational — the difference between a structural deal that reduces uncertainty and a press release that generates a two-day rally before being quietly ignored.

2. Boeing and Agricultural Purchases. The US is expected to push hard for a Chinese commitment to purchase up to 500 Boeing aircraft — a deal worth approximately $45–55 billion at list prices, though heavily discounted in practice. Sustained Chinese imports of US soybeans, energy, and beef are also on the table. The 25 million metric ton annual soybean commitment from Busan remains only partially fulfilled. China’s agricultural imports serve multiple US interests simultaneously: they reduce the trade deficit, provide political cover for Trump with farm-state voters ahead of the 2026 midterms, and give Boeing — struggling with production quality issues — the kind of large order that stabilizes investor confidence. The challenge is verification: China has a track record of making purchasing commitments and meeting them selectively.

3. Rare Earths and Semiconductor Controls. This is the most technically complex and geopolitically sensitive negotiation on the summit agenda. China controls 60–80% of global rare earth processing — and mining analysts estimate the strategic value of this leverage at $1.2 trillion, based on the cost to the US of developing alternative supply chains to a comparable scale. China controls gallium (95% of global production), germanium (60%), antimony (80%), and the processing of neodymium, dysprosium, and terbium — without which there are no advanced electric motors, no F-35 fighter jets, and no wind turbines. In October 2025, Beijing agreed to suspend some rare earth export controls until November 2026. The US wants to extend or make permanent this suspension; China wants semiconductor concessions in return — particularly the ability to access advanced AI chips and extreme ultraviolet lithography equipment, which remain subject to the strictest US export controls. This is the hardest knot to untie: both sides’ national security imperatives are in direct conflict.

4. Taiwan. Xi told Trump in February that Taiwan is “the most important issue in China-US relations” — a statement of extraordinary directness that signals Beijing’s non-negotiable bottom line. While Taiwan is unlikely to dominate the summit’s public agenda, any implicit or explicit understanding about the pace or scale of US arms sales to Taiwan could be a hidden variable in the broader trade equation — and a highly sensitive one for Asian markets, particularly Taiwan Semiconductor Manufacturing Company (TSMC) and the broader technology supply chain. TSMC’s Arizona fabs, which Trump has championed as evidence of his manufacturing renaissance, are meaningfully dependent on Taiwanese engineers and supply chains that a Taiwan Strait crisis would instantly sever.

5. Iran. The Middle East war has created a new and urgent pressure point. The US wants China to stop purchasing Iranian oil — approximately 1.5 million barrels per day, representing roughly 90% of Iran’s oil export revenues — and to use its influence in Tehran to facilitate a ceasefire. China has instead invoked its Anti-Foreign Sanctions Law to protect its oil-buying companies from US penalties, and has publicly stated that China “does not recognize” the unilateral US sanctions. This issue is likely to generate the most friction at the summit. Beijing has no economic incentive to cut Iranian oil imports — they arrive at significant discounts to market prices — and doing so would undermine the strategic partnership with Iran that gives China leverage over Middle Eastern energy flows.

6. Chinese EV Market Access. In January 2026, Trump signaled openness to allowing Chinese carmakers — including BYD, which became the world’s largest EV manufacturer by volume earlier this year — to sell in the US market, potentially in exchange for Chinese purchase commitments for Boeing aircraft and agricultural goods. US lawmakers from both parties wrote to Trump urging him to resist any such concession. The political arithmetic is treacherous: allowing BYD into the US market would create jobs in any state where BYD chose to manufacture, but would be portrayed as devastating to UAW members in Michigan and Ohio. The auto industry trade-off — US aircraft sales to China in exchange for Chinese EV access to America — is the kind of deal that looks elegant in a trade theorist’s spreadsheet and politically catastrophic in a swing-state newspaper.

The Balance of Power: Who Has More Leverage?

| Domain | US Position | China Position | Edge |

|---|---|---|---|

| Consumer Market | $18T GDP — world’s #1 consumer market | $19T GDP — surpassed US; domestic demand growing | Roughly Equal |

| Technology Controls | Advanced chips, AI software, EUV equipment | Huawei Kirin chips; SMIC advancing; Llama-equivalents | USA (narrowing) |

| Rare Earths | Building alternatives (Australia, Canada, Africa) | 60–80% of processing; $1.2T leverage; Ga, Ge, Sb | China — decisive |

| Manufacturing | Reshoring accelerating; still 2–3 yrs from scale | World’s factory; record $1T+ trade surplus | China — decisive |

| Financial System | Dollar reserve currency; SWIFT; deepest capital markets | Yuan internationalizing; $800B+ US Treasuries | USA (eroding) |

| Diplomatic Alliances | NATO, Five Eyes, Quad, G7, EU | BRICS+, SCO, BRI (140 countries), Russia, Iran, Gulf | Roughly Equal (different blocs) |

| Domestic Pressure | Legal setbacks, tariff inflation, midterm politics 2026 | Economic slowdown, youth unemployment, property crisis | Both sides need visible progress |

Multi-Polarity and the New Monetary Order

Perhaps the most consequential shift of the past decade — and the one that will outlast any individual trade deal or summit communiqué — is the fracturing of the unipolar trading order that defined the post-Cold War era. During the Pax Americana of 1945–2017, the United States provided what economists call a “public good”: an open trading system underwritten by the dollar, enforced by naval supremacy, and formalized through the WTO. This system was not purely altruistic — it served American interests by making the world economically dependent on the dollar, and by ensuring that the most dynamic companies in emerging markets needed access to the US financial system to thrive. But it was also genuinely beneficial for global growth: world trade grew from roughly $60 billion in 1950 to $25 trillion by 2017, a 40,000% expansion that lifted hundreds of millions of people out of poverty.

That system is not collapsing — but it is fracturing into three distinct blocs, each with its own rules, preferences, and increasingly, its own currencies. Bloc 1 is the US-aligned sphere: NATO, the G7, the Five Eyes intelligence alliance, the Quad (US, Japan, India, Australia), and the network of bilateral trade agreements that Washington is currently negotiating from a position of tariff pressure. Bloc 2 is the China-centered sphere: BRICS+ (now including Saudi Arabia, UAE, Iran, Egypt, and Ethiopia), the Shanghai Cooperation Organisation, the Belt and Road Initiative spanning 140 countries, and the bilateral energy and infrastructure agreements China has built across Africa, Southeast Asia, and Latin America. Bloc 3 — the most interesting from a market perspective — is the genuinely non-aligned world: India, ASEAN members, Brazil, the Gulf states, Turkey, and most of Africa. These countries are trading actively with both blocs, strategically refusing to choose sides, and extracting maximum advantage from the great-power competition.

The world has fractured into three distinct trading blocs. The non-aligned world — trading actively with both — is arguably the biggest strategic winner of the current trade war.

Gold at $4,715: Central Banks, Dedollarization, and the Structural Bull Market

Gold’s performance in 2025 and 2026 is not a simple safe-haven trade. It is the most important monetary signal of the post-war era — a collective judgment by central banks, institutional investors, sovereign wealth funds, and retail savers across the world that the dollar-denominated order is fracturing, and that the only neutral, politically unfreezable store of value is the one asset that no government can print.

The scale of central bank buying since 2022 is without modern precedent. Global central banks purchased more than 1,000 tonnes of gold annually in each of 2022, 2023, and 2024 — more than double their average annual purchases in 2015–19. In 2025, despite gold prices rising 42% to make each tonne more expensive, purchases remained above 860 tonnes — still historically extraordinary. The People’s Bank of China has made 15 consecutive monthly gold reserve additions, bringing official holdings to 2,308 tonnes — 9.6% of total reserve assets, up from 3.3% in 2019. Poland, Turkey, India, and Singapore have all made substantial additions. Even Saudi Arabia — historically dollar-aligned — has begun quietly diversifying toward gold and yuan-denominated assets.

The catalyst that transformed central bank gold buying from a trend into a stampede was Russia’s experience in February 2022. When the United States and EU froze approximately $300 billion in Russian foreign exchange reserves as a sanction for the invasion of Ukraine, every central bank in the world with any reason to fear future US sanctions — a category that extends far beyond Russia’s direct allies — drew the same conclusion: assets held in US dollars, in US financial institutions, or cleared through SWIFT are not truly sovereign. They are hostages to US foreign policy. Gold, held in physical form in domestic vaults, is the only major reserve asset that cannot be frozen, seized, or devalued by an adversary’s policy decision. The rush to acquire it is a rational response to a genuinely new geopolitical reality.

Gold peaked near $5,595 in late 2025, has since consolidated around $4,500–4,750. J.P. Morgan targets $5,000 in Q4 2026; Goldman Sachs projects $4,900 year-end. Central banks purchasing 585 tonnes/quarter in 2026 provide a structural price floor.

J.P. Morgan Global Research, the most bullish major institutional forecaster, projects gold reaching $5,000 per ounce by Q4 2026, driven by continued central bank and ETF demand averaging 585 tonnes per quarter. Goldman Sachs maintains a $4,900 year-end target. Deutsche Bank, in a more radical but increasingly mainstream analysis, projects gold reaching $8,000 on the back of sustained dedollarization momentum over the next three to five years. The structural case rests on three pillars: central bank demand running at historically elevated levels with no sign of reversal; ETF inflows running approximately 40% above year-prior levels as institutional and retail investors reallocate toward hard assets; and a sovereign price floor mechanism — central banks buy on dips as policy, not as trades, which eliminates the panic-selling dynamic that limited gold’s upside in previous cycles.

The dedollarization story is not — despite what some analysts claim — simply rhetorical. It is measurable: the dollar’s share of global foreign exchange reserves has fallen from 72% in 2000 to approximately 58% today, its lowest level since the early 1990s. In 2025, for the first time in modern history, the majority of China’s cross-border trade was settled in yuan rather than dollars. Saudi Arabia completed its first yuan-settled oil trade in 2023, and has since expanded yuan-settlement to several other transactions. BRICS+ nations now hold 17.4% of global gold reserves, up from 11.2% in 2019 — a pace of accumulation that, sustained over a decade, would fundamentally alter the composition of global monetary reserves. For traders, the practical implication is clear: gold is not a tactical trade around the Beijing summit. It is a structural allocation that benefits from the long-term erosion of dollar hegemony, and that asset allocation decision should be sized and timed accordingly.

The Most Sensitive Markets: Where the Trade War Shows Up First

The US Dollar: The Unexpected Casualty

The dollar’s behavior in this trade war has defied the conventional playbook in ways that carry profound long-term significance. In a standard trade war episode, the currency of the tariff-imposing country tends to appreciate, because tariffs reduce imports and thus the demand for foreign currency, while domestic demand for the tariff-imposing country’s goods increases. Trump’s tariff war has not followed this script. EUR/USD reached 1.1774 on May 8 — its strongest level in nearly three years. USD/CNY is testing 6.84, with the yuan near its strongest against the dollar in three years. The DXY index has fallen over 9.5% since Trump took office.

The explanation lies in confidence — or rather the loss of it. The legal chaos around IEEPA, the Supreme Court’s ruling, the administration’s erratic escalation-and-truce cycle, and the Federal Reserve’s constrained ability to respond to tariff-induced inflation have collectively damaged global confidence in US economic governance. Foreign investors have reduced US Treasury holdings. The safe-haven premium of the dollar — which historically strengthens during US-generated crises because investors trust the depth of the US financial system — has been partially eroded. This is historically unusual and potentially structurally significant: when the world’s reserve currency weakens during a crisis generated by the reserve currency country, it is a signal that the reserve currency status itself is at risk.

Equities: S&P 500 at 7,399 — Pricing Managed Détente

The S&P 500 closed at 7,399 on May 8, 2026 — up 0.84% on the day and comfortably above the year’s opening levels. This performance reflects the paradox of modern equity markets: the index is pricing a base-case scenario of managed détente rather than either a comprehensive deal or a genuine escalation. Technology earnings — driven by AI infrastructure investment that benefits from tariff-exempt cloud computing — have offset the drag from tariff-exposed manufacturers. The market is essentially saying: the trade war is bad for some sectors, but not bad enough to derail the AI-driven productivity revolution. If the summit surprises to the upside, the rally could extend by 4–6% within the week. A negative surprise could test the 7,000–7,100 support zone.

Emerging Market Currencies: AUD as China Growth Proxy

The Australian dollar — currently around 0.6450 — is the most liquid proxy for Chinese growth expectations and commodity demand. A comprehensive US-China deal would likely push AUD above 0.66. A new escalation cycle would test lower levels. The South Korean won, Malaysian ringgit, and Thai baht are similarly exposed. Conversely, the Japanese yen remains a haven within the EM complex — caught between its safe-haven status and the BoJ’s reluctance to raise rates aggressively, USD/JPY trades near 157.80 with intervention risk on any sustained move above 160.

Commodities: Copper, Rare Earths, and Oil

Copper — trading near multi-year highs — sits at the intersection of the trade war, the global energy transition, and Chinese industrial demand. As the primary conductor in electric vehicles, grid infrastructure, and renewable energy systems, copper demand is structurally supported regardless of short-term trade war noise. Rare earths — gallium, germanium, neodymium, dysprosium — are the most geopolitically consequential commodities on earth in 2026. China’s control of their processing chain gives Beijing leverage that no tariff can replicate. Oil at $97.62/barrel (WTI) reflects the Iran war premium rather than demand destruction from the trade war — a distinction that matters because any ceasefire or de-escalation in the Middle East, potentially facilitated by Chinese diplomacy acknowledged at the summit, would be a significant oil-bearish catalyst and a positive for risk sentiment globally.

Market Forecasts: 1 Day to 12 Months

The following forecasts represent our base-case scenario — the most probable outcome given current positioning — as of May 10, 2026. They incorporate the approaching Beijing summit, the legal uncertainty around US tariffs, the Iran war premium in oil, yuan trajectory, central bank gold demand, and the historical precedent of previous trade war resolution cycles. Bull and bear scenario adjustments are detailed in the following section.

| Timeframe | Key Driver | S&P 500 | Gold (XAU) | USD/CNY | EUR/USD | WTI Oil |

|---|---|---|---|---|---|---|

| 1–2 Days Pre-summit |

Pre-summit positioning; CPI data (May 12) | 7,350–7,480 | $4,650–4,780 | 6.82–6.86 | 1.175–1.185 | $95–100 |

| 1 Week Post summit |

Summit outcome — base: truce extension, Boeing signal | +1.5–3.5% | $4,500–4,650 pullback | 6.74–6.80 | 1.182–1.200 | $88–95 |

| 1 Month To mid-June |

Deal implementation; Fed decision (June 17); ECB (June 11) | 7,500–7,800 | $4,500–4,900 | 6.70–6.82 | 1.185–1.215 | $85–100 |

| 3 Months To Aug 2026 |

301 investigation timelines; IEEPA appeal; Fed rate path | 7,200–7,900 | $4,600–5,100 | 6.65–6.90 | 1.170–1.230 | $85–105 |

| 6 Months To Nov 2026 |

New Section 301 tariffs (H2); export control suspension expiry | 7,000–7,900 | $4,700–5,300 | 6.60–7.00 | 1.190–1.250 | $80–110 |

| 12 Months May 2027 |

“Board of Trade” framework; dedollarization; US midterms | 7,600–8,400 | $4,900–5,600 | 6.50–6.78 | 1.210–1.270 | $75–100 |

The most critical near-term catalyst is the summit itself. A significantly better-than-expected outcome — a comprehensive “Board of Trade” framework, immediate tariff path reduction, rare earth access secured, and a Boeing deal signed — would be a genuine positive surprise and could drive S&P 500 gains of 4–6% within the week, gold pullback toward $4,400, yuan strengthening through 6.75/$, and WTI oil falling below $90 if China explicitly distances itself from the Iran conflict. A significantly worse-than-expected outcome — a breakdown in talks, new tariff threats, or a hostile joint statement on Iran — would likely trigger a 3–5% equity sell-off, gold above $5,000, and a sharp strengthening of safe-haven currencies (yen, Swiss franc).

The Critical H2 Variable: Section 301 Timelines

The six-month and one-year forecasts hinge on whether the Trump administration is able to rebuild its tariff wall through Section 301 after the IEEPA ruling. Section 301 investigation timelines require formal hearings and public comment periods — meaning new tariffs targeting China’s industrial overcapacity or forced labor practices are unlikely before Q4 2026 at the earliest. This creates a window of relative tariff stability between May and November 2026, within which the Beijing summit outcomes will largely define market direction. After November 2026 — when the rare earth export control suspension from Busan expires and new Section 301 tariffs may be ready for imposition — the risk of renewed escalation rises significantly. Position management across that horizon requires monitoring both the Section 301 investigation progress and the rare earth negotiation outcome from the May 14–15 summit.

Three Scenarios for the Next 12 Months

The Grand Bargain. Trump and Xi strike a comprehensive “Board of Trade” agreement at the May 14–15 summit — a Boeing deal worth $45B+, soybean commitments renewed and expanded, rare earth access secured to November 2027, and a roadmap for phased tariff reduction under the new Section 301 framework. The Supreme Court upholds a modified IEEPA framework on appeal. The Iran war de-escalates via Chinese mediation, oil falls toward $75. The Fed resumes rate cuts in Q3. S&P 500 breaks 8,200 by year-end. Gold consolidates at $4,500–4,900. Dollar weakens further vs euro and yuan. AUD/USD tests 0.70. Risk appetite surges across EM.

Managed Détente. The summit produces a face-saving joint statement — Busan truce extended to mid-2027, some purchase commitments renewed (Boeing letter of intent, soybean targets reiterated), a “Board of Trade” concept endorsed in principle without binding framework. Section 301 investigations proceed on schedule. Tariffs remain stable at ~24% effective rate on China through year-end. S&P 500 trades 7,400–7,900, gold drifts toward $4,900–5,300 by December. Dollar gradually weakens. Rare earth suspension extended. The world adjusts to permanent managed trade — not free trade, not war. Blocs harden but conflict stays below the boiling point.

Renewed Escalation. The Beijing summit fails to produce meaningful progress — a hostile communiqué, new Iranian oil sanctions on Chinese refiners announced within days, and Trump returning to threaten new 301 tariffs on a fast-track timeline. The Supreme Court defeats the IEEPA appeal. China reimports rare earth export controls when the November 2026 suspension expires. The Iran war widens, oil spikes above $120. Global recession risk rises materially. S&P 500 tests 6,200–6,500. Gold surges toward $5,500–5,800. Dollar initially strengthens on safe-haven flows before cracking on US recession fears. EM currencies sell off sharply.

The 5-Year Structural View: Dedollarization as a Megatrend

Beyond the 12-month forecast horizon lies a structural shift that will matter more than any individual tariff rate or summit outcome: the slow, measured, and now unmistakably deliberate erosion of the dollar’s monopoly on global trade settlement. The BRICS+ group now represents approximately 36% of global GDP at purchasing power parity. In 2025, for the first time in modern history, the majority of China’s cross-border trade was settled in yuan rather than dollars. Saudi Arabia has completed yuan-settled oil trades. India buys Russian oil in rupees. Brazil and China have a bilateral yuan-settlement mechanism. The IMF’s own projections suggest the dollar’s reserve share will fall below 50% by 2030 under a scenario of continued US fiscal expansion and geopolitical fragmentation.

Gold, in this context, is not a tactical hedge. It is the primary beneficiary of a monetary system in transition — the asset that central banks, sovereign wealth funds, and sophisticated investors are accumulating as the only neutral reserve that cannot be weaponized by any single power. The current price of $4,715 per ounce already reflects significant remonetization. The targets of $4,900 (Goldman Sachs), $5,000 (J.P. Morgan), and $8,000 (Deutsche Bank, multi-year) reflect progressively deeper assumptions about how far that remonetization goes. For traders at Capital Street FX, accessing this structural trend through gold, yuan, and commodity exposure is not speculative — it is the core macro trade of the decade.

Conclusion: The Dragon and the Eagle in the Great Hall

On May 14, Donald Trump will walk into the Great Hall of the People in Beijing carrying 200 years of trade war history on his shoulders — whether he knows it or not. He carries the ghost of Smoot-Hawley, the lesson of the Japan trade wars, the unfinished business of his own first term, the burden of a Supreme Court that has partially dismantled his most ambitious protectionist ambitions, and the shadow of an Iran war that has made China simultaneously a critical diplomatic partner and a defiant economic rival. Xi Jinping will meet him with a trillion-dollar trade surplus, a rare earth arsenal estimated at $1.2 trillion in strategic value, a diplomatic network spanning 140 countries, and the patient confidence of a civilization that measures geopolitical time in centuries, not election cycles.

Neither man will win this summit outright. That is the nature of trade wars between genuine great powers — they do not end with surrender; they end with exhaustion and accommodation. The most likely outcome is a managed de-escalation: enough of a deal to allow both leaders to claim progress, stabilize markets, buy time for the Section 301 legal architecture to be built, and allow the Iran war to find its own trajectory. Markets, pricing in a 58.5% chance of an agreement by May 31, are cautiously optimistic. That caution is warranted — but so is the optimism.

What is clear, looking across the full sweep of 200 years of trade war history, is that we are not at the end of this cycle — we are somewhere in the middle of it. The structural forces driving the current protectionist wave are not going to be resolved by a two-day summit in Beijing. Great-power competition, supply chain insecurity, political backlash against globalization, and technological rivalry will define the contours of the global economy for the next decade, perhaps longer. The investors, traders, and institutions that understand those forces — that can read the history, track the geopolitics, and position across the asset classes most sensitive to their resolution — will find extraordinary opportunities in the volatility ahead.

Gold knows it — at $4,715 per ounce, up more than 40% year-on-year, consolidating after a 52-week high of $5,595, with central banks buying at historically extraordinary rates. The yuan knows it — strengthening despite all predictions of collapse, as China’s trade surplus swells and its monetary influence expands. The dollar, slowly and reluctantly, is beginning to acknowledge it. The question is whether the men sitting across from each other in the Great Hall of the People next week will find enough common ground to manage this transition — from a unipolar dollar order to a multi-polar monetary world — without repeating history’s most catastrophic mistakes.

All market data is current as of May 9–10, 2026. Forecasts are analytical estimates and do not constitute investment advice. Trading involves significant risk of loss. Please manage position sizes appropriately.